Wipro

•

0 likes•74 views

Wipro reported financial results for the first quarter of fiscal year 2011, with revenues growing 3.1% over the previous quarter and 12.6% over the same quarter last year. Operating profit margins expanded due to effective currency hedges, and net income grew 9% over the previous quarter and 30.5% over the first quarter of fiscal year 2010. The company's performance was driven by strong volume growth in IT services revenues, with new client additions and large deal wins during the quarter. The analyst maintained an "Accumulate" rating on Wipro stock, with a target price representing 13% upside.

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (17)

Similar to Wipro

Similar to Wipro (19)

More from Angel Broking

More from Angel Broking (20)

Recently uploaded

Recently uploaded (20)

Wipro

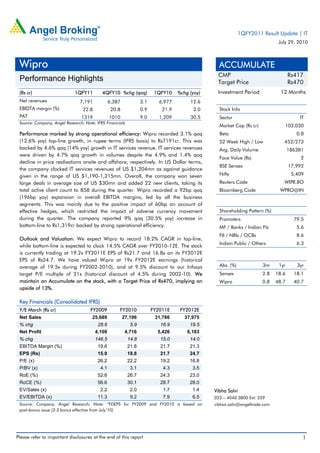

- 1. 1QFY2011 Result Update | IT July 29, 2010 Wipro ACCUMULATE CMP Rs417 Performance Highlights Target Price Rs470 (Rs cr) 1QFY11 4QFY10 %chg (qoq) 1QFY10 %chg (yoy) Investment Period 12 Months Net revenues 7,191 6,387 3.1 6,977 12.6 EBIDTA margin (%) 22.8 20.8 0.9 21.9 2.0 Stock Info PAT 1319 1010 9.0 1,209 30.5 Sector IT Source: Company, Angel Research; Note: IFRS Financials Market Cap (Rs cr) 102,030 Performance marked by strong operational efficiency: Wipro recorded 3.1% qoq Beta 0.8 (12.6% yoy) top-line growth, in rupee terms (IFRS basis) to Rs7191cr. This was 52 Week High / Low 452/273 backed by 4.6% qoq (14% yoy) growth in IT services revenue. IT services revenues Avg. Daily Volume 186381 were driven by 4.7% qoq growth in volumes despite the 4.9% and 1.4% qoq Face Value (Rs) 2 decline in price realisations onsite and offshore, respectively. In US Dollar terms, BSE Sensex 17,992 the company clocked IT services revenues of US $1,204mn as against guidance given in the range of US $1,190-1,215mn. Overall, the company won seven Nifty 5,409 large deals in average size of US $30mn and added 22 new clients, taking its Reuters Code WIPR.BO total active client count to 858 during the quarter. Wipro recorded a 92bp qoq Bloomberg Code WPRO@IN (196bp yoy) expansion in overall EBITDA margins, led by all the business segments. This was mainly due to the positive impact of 60bp on account of effective hedges, which restricted the impact of adverse currency movement Shareholding Pattern (%) during the quarter. The company reported 9% qoq (30.5% yoy) increase in Promoters 79.5 bottom-line to Rs1,319cr backed by strong operational efficiency. MF / Banks / Indian Fls 5.6 FII / NRIs / OCBs 8.6 Outlook and Valuation: We expect Wipro to record 18.2% CAGR in top-line, Indian Public / Others 6.3 while bottom-line is expected to clock 14.5% CAGR over FY2010-12E. The stock is currently trading at 19.2x FY2011E EPS of Rs21.7 and 16.8x on its FY2012E EPS of Rs24.7. We have valued Wipro at 19x FY2012E earnings (historical average of 19.5x during FY2002-2010), and at 9.5% discount to our Infosys Abs. (%) 3m 1yr 3yr target P/E multiple of 21x (historical discount of 4.5% during 2002-10). We Sensex 2.8 18.6 18.1 maintain an Accumulate on the stock, with a Target Price of Rs470, implying an Wipro 0.8 48.7 40.7 upside of 13%. Key Financials (Consolidated IFRS) Y/E March (Rs cr) FY2009 FY2010 FY2011E FY2012E Net Sales 25,689 27,196 31,786 37,975 % chg 28.6 5.9 16.9 19.5 Net Profit 4,109 4,716 5,426 6,183 % chg 146.5 14.8 15.0 14.0 EBITDA Margin (%) 19.6 21.8 21.7 21.3 EPS (Rs) 15.9 18.8 21.7 24.7 P/E (x) 26.2 22.2 19.2 16.8 P/BV (x) 4.1 3.1 4.3 3.5 RoE (%) 52.6 26.7 24.3 23.0 RoCE (%) 56.6 30.1 28.7 28.0 EV/Sales (x) 2.2 2.0 1.7 1.4 Vibha Salvi EV/EBITDA (x) 11.3 9.2 7.9 6.5 022 – 4040 3800 Ext: 329 Source: Company, Angel Research; Note: *FDEPS for FY2009 and FY2010 is based on vibhas.salvi@angeltrade.com post-bonus issue (2:3 bonus effective from July’10) Please refer to important disclosures at the end of this report 1

- 2. Wipro | 1Q FY2011Result Update Exhibit 1: 1QFY2011 performance (consolidated, IFRS) Y/E March (Rs cr) 1QFY11 4QFY10 % chg 1QFY10 % chg FY2010 FY2009 % chg (qoq) (yoy) Net Revenues 7,191 6,977 3.1 6,387 12.6 27,196 25,689 5.9 Cost of Revenue 4,676 4,588 1.9 4,138 13.0 17,938 17,386 3.2 Gross Profit 2,514 2,390 5.2 2,249 11.8 9,258 8,303 11.5 SG&A Expenses 923 870 6.0 779 18.4 3,252 3,123 4.1 Forex Gains/Losses (net) (46) (6) 141 72 155 Operating Profit (EBITDA) 1,638 1,525 7.4 1,329 23.2 5,934 5,025 18.1 Other Income 135 185 (26.9) 100 35.8 460 357 29.0 Interest 40 24 70.0 64 (37.0) 123.2 233 (47.2) Depreciation 188 189 (0.2) 187 0.9 783.10 694.70 12.7 Share of profits of Equity 16 18 (10.8) 11 37.7 53 36 46.4 accounted associates Income before Income Taxes 1,560 1,515 2.9 1,189 31.1 5,541 4,490 23.4 Income Taxes 235 302 (22.2) 174 34.8 929 604 54.0 Minority Interest 7 5 45.7 5 36.7 18.500 10 86.9 Net Income 1,319 1,209 9.0 1,010 30.5 4,593 3,876 18.5 Diluted EPS (Rs) 5.4 5.0 9.0 4.1 31.0 31.2 26.5 17.9 Gross Profit Margin (%) 35.0 34.2 35.2 34.0 32.3 EBITDA Margin (%) 22.8 21.9 20.8 21.8 19.6 Net Profit Margin (%) 18.3 17.3 15.8 16.9 15.1 Source: Company, Angel Research Exhibit 2: 1QFY2011 – Actual v/s Angel estimates (Rs cr) Estimates Actual Variation (%) Net revenue 7,134 7,191 0.8 EBIDTA margin (%) 21.2 22.8 0.0 PAT 1,213 1,319 8.7 Source: Company, Angel Research Top-line growth led by strong volumes in IT services Wipro recorded 3.1% qoq (12.6% yoy) top-line growth, in rupee terms (IFRS basis), backed by 4.6% qoq (14% yoy) growth in IT services revenues, which were driven by 4.7% qoq growth in volumes despite the 4.9% and 1.4% qoq decline in price realisations onsite and offshore, respectively. Higher volumes were on account of new project start ups during the quarter mainly onsite, which impacted the price realisation severely there compared to offshore. In US Dollar terms, the company clocked IT services revenues of US $1,204mn as against guidance given in the range of US $1,190-1,215mn. The growth in IT Services was broad-based, and mainly driven by 18.5%, 9.7%, 3.7% and 2.6% qoq growth in product engineering services (PES), package implementation (PI), ADM and R&D services, respectively. In terms of verticals, growth was strongly driven by communication & media services providers (CMSP), financial services, manufacturing and retail-transportation verticals, which grew by 6.4%, 6.4%, 5.5% and 5.1% qoq, respectively. In addition to IT services segments, the consumer care and lightning, and other businesses also grew by 5.4% and July 29, 2010 2

- 3. Wipro | 1Q FY2011Result Update 1.6% qoq, respectively. The IT product business de-grew by 6.5% qoq, but was up by 13.4% yoy. In terms of geographies, America, India and the Middle East and APAC, and other emerging markets witnessed growth of 4.3%, 5.4% and 5.6% qoq, respectively. Despite the ongoing crisis in Europe, the company witnessed slight de-growth of 0.2% qoq, while it grew by 16.2% yoy. In fact, Wipro won a large deal from one of its European client, viz. Citibank to take over the ownership and management of its data center in Meerbusch, Germany. As per the agreement Citibank will lease back-office and data center space from Wipro for at least 30 months and Wipro will provide Citibank with facilities management and IMS services during the period. The Meerbusch Germany data center will be Wipro’s first facility in Europe and will enable it to offer full portfolio of infrastructure management solutions (IMS) to its European and global clients. Overall, the company won seven large deals in average size of US $30mn and added 22 new clients, taking its total active client count to 858 during the quarter. Exhibit 3: Segment-wise revenue breakup Rs cr 1QFY11 4QFY10 1QFY10 chg chg qoq % yoy % IT services 5,500 5,260 4,827 4.6 14.0 Pure IT Services 4,945 4,686 4,339 5.5 14.0 BPO Services 556 573 487 (3.1) 14.0 IT Products 832 890 734 (6.5) 13.4 Consumer Care & Lightning 641 608 520 5.4 23.4 Others 232 229 149 1.6 56.3 Eliminations (15) (9) 158 62.4 (109.5) Total 7,191 6,977 6,387 3.1 12.6 Source: Company, Angel Research Effective hedges contained adverse currency impact on margins During 1QFY2011, Wipro recorded a 92bp qoq (196bp yoy) expansion in overall EBITDA margins, led by all the business segments. Despite the higher employee costs (with infused freshers hiring) and decline in pricing, the company witnessed 37bp qoq (238bp yoy) expansion in EBIT margins of IT services segment. This was mainly due to the positive impact of 60bp on account of effective hedges, which contained the adverse currency impact on EBIDTA margins during the quarter. The EBIT margins in IT products and consumer care and lighting businesses also expanded by 111bp and 44bp qoq, respectively. The company continued to witness strong sequential ramp up in its fixed-priced projects mix, which was up by 30bp qoq to 44.6% in 1QFY2011. July 29, 2010 3

- 4. Wipro | 1Q FY2011Result Update Exhibit 4: EBITDA margin trend 25 24 23 22 (%) 21 20 19 1QFY08 2QFY08 3QFY08 4QFY08 1QFY09 2QFY09 3QFY09 4QFY09 1QFY10 2QFY10 3QFY10 4QFY10 1QFY11 Wipro (Total) Wipro (IT Services) Source: Company, Angel Research Strong operational efficiency boosts bottom-line Other income declined by 26.9% qoq mainly due to gains from exchange fluctuation in 4QFY2010, absent in 1QFY2011. However, on a yoy basis, other income was up 35.8% due to higher interest income. The interest cost increased by 70% qoq with increase in debt levels during the quarter. Further, the effective tax rate was down from 20% in 4QFY2010 to 15% in 1QFY2011. Thus, at the net level, the company reported 9% qoq (30.5% yoy) increase in bottom-line backed by strong operational efficiency. Strong manpower additions aided growth Wipro made net addition of 4,854 employees during the quarter taking total headcount to 1,12,925. The quarterly annualised attrition rate in Global IT services was up at 23% (17.1% in 4QFY2010); however, on TTM basis, it stood lower at 15.8%, yet higher from 12.1% in 4QFY2010. In BPO services, the quarterly attrition stood at 16% (17% in 4QFY2010). The company has strong hiring plans both for laterals and freshers going forward, with the improvement in demand environment. 2QFY2011E revenue guidance at US $1,253-1,277mn Despite challenging macro-economic indicators Wipro has given strong revenue guidance for the IT services segment for 2QFY2011 in the range of US $1,253-1,277mn, a sequential growth of 4.1 - 6.1%. To address the attrition issue, the company gave 20,000 promotions with effect from July 1, 2010 and will also award restricted stock units (RSUs) to its middle management staff. Thus, adverse currency movement and higher employee costs (with strong hiring and variable spends) would remain key headwinds impacting the margins and bottom-line in 2QFY2011. July 29, 2010 4

- 5. Wipro | 1Q FY2011Result Update Investment Arguments Broad-based volume led growth with uptick in discretionary spends and stable pricing environment The strong growth witnessed in Wipro’s package implementation service revenues during 1QFY2011 reflects the pick-up in discretionary spends of clients. Significant spend is currently happening in social customer relationship management (CRM), which if it grows further as expected would certainly assure strong top-line and better profitability for the company going forward. Further, the consumer package goods (CPG), retail & transportation, energy & utilities and the healthcare verticals are witnessing strong demand pipeline and are expected to grow strongly. The financial services vertical is also witnessing steady demand pick. The company is witnessing a stable pricing environment from most of its clients with some expected to give an upward revision going forward. Non-linear initiatives to drive growth Wipro’s non-linear initiatives include implementation of shared services model thereby executing more projects without any major employee deployment, which would result in costs savings. Other such initiatives include its platform oriented integrated IT and BPO offerings and intellectual property related revenues. Such offerings help to drive better profitability in projects without incurring of additional fixed costs. The company expects these initiatives to contribute ~14% of its revenues in FY2011. Outlook and Valuation We expect Wipro to record 18.2% CAGR in top-line, while bottom-line is expected to clock 14.5% CAGR over FY2010-12E. The stock is currently trading at 19.2x FY2011E EPS of Rs21.7 and 16.8x on its FY2012E EPS of Rs24.7. We have valued Wipro at 19x FY2012E earnings (historical average of 19.5x during FY2002- 2010), and at 9.5% discount to our Infosys target P/E multiple of 21x (historical discount of 4.5% during 2002-10). We maintain an Accumulate on the stock, with a Target Price of Rs470, implying an upside of 13%. Exhibit 5: Key assumptions FY2011E FY2012E Volume growth 20.0 18.6 Pricing growth (2.6) 2.7 Revenue growth (in US $ terms) 16.2 18.1 USD-INR rate (realised) 46.5 47.0 Revenue Growth (in Re terms) 17.0 19.5 EBIDTA Margin (%) 21.7 21.3 Tax Rate (%) 18.0 20.0 EPS Growth (%) 15.4 14.1 Source: Company, Angel Research July 29, 2010 5

- 6. Wipro | 1Q FY2011Result Update Exhibit 6: Change in estimates FY2011E FY2012E Parameter Earlier Revised Var. Earlier Revised Var. (Rs cr) estimates estimates (%) estimates estimates (%) Net revenue 31,034 31,786 2.4 37,317 37,975 1.8 EBIDTA 6,620 6,901 4.2 7,741 8,094 4.6 PBT 6,028 6,590 9.3 7,194 7,696 7.0 Tax 1,085 1,164 7.3 1,439 1,513 5.1 PAT 4,988 5,426 8.8 5,805 6,183 6.5 Source: Company, Angel Research We have upgraded our FY2011E and FY2012E top-line estimates, in line with strong cues from management and the expected higher infusion of gross manpower. Since the company has a strong hedge position (currently stands at US $1.6bn), unfavourable cross-currency movement would have lesser impact on EBIDTA margins as expected earlier. We estimate PAT to be higher in FY2011E and FY2012E, compared to the earlier estimates, on the back of better margins. Exhibit 7: Angel EPS forecast v/s consensus Bloomberg Variation Year (%) Angel forecast consensus (%) FY2011E 21.7 22.2 (2.3) FY2012E 24.7 25.2 (2.0) Source: Company, Angel Research Exhibit 8: One-year forward P/E band 800 30x 700 600 25x Share Price (Rs) 500 20x 400 15x 300 200 100 Dec-05 Apr-04 Jul-05 Aug-07 Apr-09 Jul-10 Mar-07 Oct-06 Sep-04 Feb-05 Sep-09 Feb-10 Nov-08 May-06 Jun-08 Jan-08 Source: Company, Angel Research July 29, 2010 6

- 7. Wipro | 1Q FY2011Result Update Exhibit 9: Premium/discount in Wipro P/E versus Infosys P/E 130.0 110.0 90.0 70.0 50.0 30.0 10.0 (10.0) (30.0) (50.0) Dec-03 Dec-08 Apr-02 Jul-03 Aug-05 Apr-07 Jul-08 Mar-05 Mar-10 Oct-04 Oct-09 Sep-02 Feb-03 Sep-07 Feb-08 Nov-06 May-04 May-09 Jun-06 Jan-06 Premium/Discount to Sensex Avg. Historical Discount Source: Company, Angel Research Exhibit 10: Recommendation summary Company Reco. CMP Tgt. price Upside FY2012E FY2012E FY2010-12E FY2012E FY2012E (Rs) (Rs) (%) P/BV (x) P/E (x) EPS CAGR (%) RoCE (%) RoE (%) 3iInfotech Buy 63 95 50.8 0.6 3.6 218.4 15.0 16.5 Educomp Buy 618 734 18.8 2.8 13.5 26.9 21.0 22.3 HCL Tech Accumulate 379 420 11.0 3.1 14.1 17.9 40.9 24.1 Infosys Accumulate 2,834 2,900 2.3 4.6 20.5 12.6 33.1 25.0 Infotech Enterprises Buy 167 192 15.0 1.4 8.6 12.1 18.1 17.0 Mphasis Buy 600 872 45.5 2.4 9.3 14.9 41.6 29.2 NIIT Buy 66 83 25.2 1.7 11.5 16.6 12.1 15.8 TCS Buy 850 920 8.2 5.3 19.4 11.7 53.2 30.4 Tech Mahindra Buy 704 950 35.0 2.0 10.5 11.8 73.4 22.0 Wipro Buy 417 470 12.8 3.5 16.8 14.7 28.0 23.0 Source: Company, Angel Research July 29, 2010 7

- 8. Wipro | 1Q FY2011Result Update Profit & Loss Statement (Consolidated IFRS) Y/E March (Rs cr) FY2009 FY2010 FY2011E FY2012E Gross sales 25,689 27,196 31,786 37,975 Less: Excise duty - - - - Net Sales 25,689 27,196 31,786 37,975 Other operating income - - - - Total operating income 25,689 27,196 31,786 37,975 % chg 28.6 5.9 16.9 19.5 Total Expenditure 20,664 21,262 24,885 29,880 Cost of Equipment 3,463 3,497 3,878 4,557 SGA 1,905 1,947 2,177 2,525 Cost of IT 15,142 15,746 18,751 22,712 Other 155 72 79 86 EBITDA 5,025 5,934 6,901 8,094 (% of Net Sales) 19.6 21.8 21.7 21.3 Depreciation& Amortisation 695 783 880 993 EBIT 4,330 5,151 6,022 7,102 (% of Net Sales) 16.9 18.9 18.9 18.7 Interest & other Charges 233 123 124 132 Other Income 393 513 568 594 (% of PBT) 8.7 9.3 8.8 7.9 Recurring PBT 4,490 5,541 6,466 7,564 % chg 22.0 23.4 16.7 17.0 Extraordinary Expense/(Inc.) - - - - PBT (reported) 4,490 5,541 6,466 7,564 Tax 604 929 1,164 1,513 (% of PBT) 13.4 16.8 18.0 20.0 PAT (reported) 3,886 4,612 5,302 6,051 Add: Share of earnings of - - - - associate Less: Minority interest (MI) (9.9) (18.5) - - Prior period items - - - - PAT after MI (reported) 3,876 4,593 5,302 6,051 ADJ. PAT 3,876 4,593 5,302 6,051 % chg 18.8 18.5 15.4 14.1 (% of Net Sales) 15.1 16.9 16.7 15.9 Basic EPS (Rs) 26.7 31.5 21.7 24.7 Fully Diluted EPS (Rs) 26.5 31.2 21.7 24.7 % chg 18.8 18.5 15.4 14.1 July 29, 2010 8

- 9. Wipro | 1Q FY2011Result Update Balance Sheet (Consolidated IFRS) Y/E March (Rs cr) FY2009 FY2010 FY2011E FY2012E SOURCES OF FUNDS Equity Share Capital 293 294 489 489 Reserves& Surplus 14,071 19,047 23,446 28,305 Shareholders Funds 14,364 19,341 23,935 28,794 Minority Interest 375 314 - - Total Loans 3,323 2,563 2,713 2,913 Total Liabilities 18,061 22,218 26,648 31,707 APPLICATION OF FUNDS Gross Block 7,421 8,561 9,561 10,561 Less: Acc. Depreciation 3,465 4,049 4,929 5,922 Net Block 3,956 4,511 4,632 4,639 Capital Work-in-Progress 1,373 1,236 1,236 1,236 Goodwill 5,614 5,380 5,530 5,530 Investments 1,365 1,276 1,626 1,676 Current Assets 16,078 20,551 24,736 30,388 Cash 4,912 6,488 6,477 8,785 Loans & Advances - - - - Other 11,166 14,064 18,259 21,603 Current liabilities 10,324 10,737 11,112 11,762 Net Current Assets 5,753 9,814 13,624 18,626 Mis. Exp. not written off - - - - Total Assets 18,061 22,218 26,648 31,707 Cash Flow Statement (Consolidated IFRS) Y/E March (Rs cr) FY2009 FY2010 FY2011E FY2012E Profit before tax 4,490 5,541 6,466 7,564 Depreciation 695 783 880 993 Change in Working Capital (1,075) 731 (4,661) (2,708) Less: Other income (287) 1,164 568 594 Direct taxes paid 786 791 1,164 1,513 Cash Flow from Operations 3,610 5,100 952 3,741 (Inc)./ Dec in Fixed Assets (1,742) (2,770) (609) (985) (Inc)./ Dec. in Investments (375) (580) (50) (50) (Inc)./ Dec. in loans and adv. (668) (405) - Other income 366 374 568 594 Cash Flow from Investing (2,418) (3,382) (91) (441) Issue of Equity 8 9 - - Inc./(Dec.) in loans 349 614 150 200 Dividend Paid (Incl. Tax) 683 682 1,022 1,192 Others (fx effect) 155 (82) - - Cash Flow from Financing (171) (142) (872) (992) Inc./(Dec.) in Cash 1,020 1,576 (11) 2,308 Opening Cash balances 3,891 4,912 6,488 6,477 Closing Cash balances 4,912 6,488 6,477 8,785 July 29, 2010 9

- 10. Wipro | 1Q FY2011Result Update Key Ratios Y/E March FY2009 FY2010 FY2011E FY2012E Valuation Ratio (x) P/E (on FDEPS) 7.8 10.4 19.2 16.8 P/CEPS 13.3 11.4 16.5 14.5 P/BV 4.1 3.1 4.3 3.5 Dividend yield (%) 1.0 1.4 0.9 1.0 EV/Sales 2.2 2.0 1.7 1.4 EV/EBITDA 11.3 9.2 7.9 6.5 EV / Total Assets 2.0 1.7 1.4 1.2 Per Share Data (Rs) EPS (Basic) 26.7 31.5 21.7 24.7 EPS (fully diluted) 26.5 31.2 21.7 24.7 Cash EPS 31.3 36.6 25.3 28.8 DPS 4.0 6.0 3.6 4.2 Book Value 100.8 133.7 97.8 117.7 DuPont Analysis EBIT margin 16.9 18.9 18.9 18.7 Tax retention ratio 86.6 83.2 82.0 80.0 Asset turnover (x) 1.2 1.1 1.1 1.2 ROIC (Post-tax) 47.9 25.6 24.6 24.3 Cost of Debt (Post Tax) 12.2 3.5 3.9 3.8 Leverage (x) 0.3 0.2 0.1 0.1 Operating ROE 20.9 19.5 18.9 18.2 Returns (%) ROCE (Pre-tax) 56.6 30.1 28.7 28.0 Angel ROIC (Pre-tax) 78.1 38.7 34.4 32.3 ROE 52.6 26.7 24.3 23.0 Turnover ratios (x) Asset Turnover (Gross Block) 3.6 3.3 3.5 3.7 Inventory / Sales (days) 6 12 12 12 Receivables (days) 89 91 93 92 Payables (days) 54 106 90 78 Working capital cycle (ex-cash) (days) 7 45 82 95 Solvency ratios (x) Net debt to equity 0.1 - - - Net debt to EBITDA 0.4 - - - Interest Coverage (EBIT / Interest) 18.6 41.8 48.6 53.7 Note: *FDEPS for FY2009 and FY2010 is based on pre-bonus issue (2:3bonus effective from July’10) July 29, 2010 10

- 11. Wipro | 1Q FY2011Result Update Research Team Tel: 022 - 4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com Disclaimer This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and risks of such an investment. Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this document are those of the analyst, and the company may or may not subscribe to all the views expressed within. Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's fundamentals. The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report. Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory, compliance, or other reasons that prevent us from doing so. This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced, redistributed or passed on, directly or indirectly. Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in the past. Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in connection with the use of this information. Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and its affiliates may have investment positions in the stocks recommended in this report. Disclosure of Interest Statement Wipro 1. Analyst ownership of the stock No 2. Angel and its Group companies ownership of the stock No 3. Angel and its Group companies' Directors ownership of the stock No 4. Broking relationship with company covered No Note: We have not considered any Exposure below Rs 1 lakh for Angel, its Group companies and Directors. Ratings (Returns) : Buy (> 15%) Accumulate (5% to 15%) Neutral (-5 to 5%) Reduce (-5% to 15%) Sell (< -15%) July 29, 2010 11