1. Market Outlook

India Research

July 19, 2011

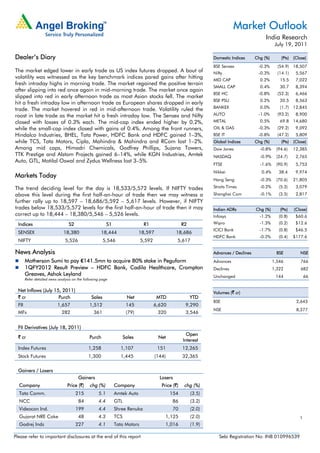

Dealer’s Diary Domestic Indices Chg (%) (Pts) (Close)

BSE Sensex -0.3% (54.9) 18,507

The market edged lower in early trade as US index futures dropped. A bout of Nifty -0.3% (14.1) 5,567

volatility was witnessed as the key benchmark indices pared gains after hitting MID CAP 0.2% 15.5 7,022

fresh intraday highs in morning trade. The market regained the positive terrain

SMALL CAP 0.4% 30.7 8,394

after slipping into red once again in mid-morning trade. The market once again

BSE HC -0.8% (52.3) 6,466

slipped into red in early afternoon trade as most Asian stocks fell. The market

BSE PSU 0.2% 20.5 8,563

hit a fresh intraday low in afternoon trade as European shares dropped in early

BANKEX 0.0% (1.7) 12,845

trade. The market hovered in red in mid-afternoon trade. Volatility ruled the

roost in late trade as the market hit a fresh intraday low. The Sensex and Nifty AUTO -1.0% (93.2) 8,900

closed with losses of 0.3% each. The mid-cap index ended higher by 0.2%, METAL 0.5% 69.8 14,680

while the small-cap index closed with gains of 0.4%. Among the front runners, OIL & GAS -0.3% (29.2) 9,092

Hindalco Industries, BHEL, Tata Power, HDFC Bank and HDFC gained 1–3%, BSE IT -0.8% (47.2) 5,809

while TCS, Tata Motors, Cipla, Mahindra & Mahindra and RCom lost 1–2%. Global Indices Chg (%) (Pts) (Close)

Among mid caps, Himadri Chemicals, Godfrey Phillips, Sujana Towers, Dow Jones -0.8% (94.6) 12,385

TTK Prestige and Alstom Projects gained 6–14%, while KGN Industries, Amtek NASDAQ -0.9% (24.7) 2,765

Auto, GTL, Motilal Oswal and Zydus Wellness lost 3–5%.

FTSE -1.6% (90.9) 5,753

Nikkei 0.4% 38.4 9,974

Markets Today

Hang Seng -0.3% (70.6) 21,805

The trend deciding level for the day is 18,533/5,572 levels. If NIFTY trades Straits Times -0.2% (5.3) 3,079

above this level during the first half-an-hour of trade then we may witness a Shanghai Com -0.1% (3.5) 2,817

further rally up to 18,597 – 18,686/5,592 – 5,617 levels. However, if NIFTY

trades below 18,533/5,572 levels for the first half-an-hour of trade then it may Indian ADRs Chg (%) (Pts) (Close)

correct up to 18,444 – 18,380/5,546 – 5,526 levels. Infosys -1.2% (0.8) $60.6

Indices S2 S1 R1 R2 Wipro -1.3% (0.2) $12.6

ICICI Bank -1.7% (0.8) $46.5

SENSEX 18,380 18,444 18,597 18,686

HDFC Bank -0.2% (0.4) $177.6

NIFTY 5,526 5,546 5,592 5,617

News Analysis Advances / Declines BSE NSE

Motherson Sumi to pay €141.5mn to acquire 80% stake in Peguform Advances 1,546 766

1QFY2012 Result Preview – HDFC Bank, Cadila Healthcare, Crompton Declines 1,322 682

Greaves, Ashok Leyland Unchanged 144 66

Refer detailed news analysis on the following page

Net Inflows (July 15, 2011) Volumes (` cr)

` cr Purch Sales Net MTD YTD

BSE 2,643

FII 1,657 1,512 145 6,620 9,290

NSE 8,277

MFs 282 361 (79) 320 3,546

FII Derivatives (July 18, 2011)

Open

` cr Purch Sales Net

Interest

Index Futures 1,258 1,107 151 12,265

Stock Futures 1,300 1,445 (144) 32,365

Gainers / Losers

Gainers Losers

Company Price (`) chg (%) Company Price (`) chg (%)

Tata Comm. 215 5.1 Amtek Auto 154 (3.5)

NCC 84 4.4 GTL 86 (3.2)

Videocon Ind. 199 4.4 Shree Renuka 70 (2.0)

Gujarat NRE Coke 48 4.3 TCS 1,125 (2.0) 1

Godrej Inds 227 4.1 Tata Motors 1,016 (1.9)

Please refer to important disclosures at the end of this report Sebi Registration No: INB 010996539

2. Market Outlook | India Research

Motherson Sumi to pay €141.5mn to acquire 80% stake in Peguform

Motherson Sumi Systems (MSSL) along with group firm Samvardhana Motherson Finance

Ltd. (SMFL) has agreed to acquire 80% stake in Peguform GmbH and Peguform Iberica, SL

together with 50% stake in Wethje Entwicklungs GmbH and Wethje Carbon Composite

GmbH. The acquisition would be made through a joint venture company in which MSSL

would hold 51% stake and SMFL would hold 49% stake. The total share consideration for

the transaction is €141.5mn, of which MSSL would pay €72.2mn and the remaining would

be paid by SMFL. MSSL intends to fund its share of acquisition through overseas loan.

We believe the deal is attractively valued at ~5.1x and ~0.25x EV/EBITDA and EV/Sales,

respectively, on CY2010 basis. We expect the deal to be positive for the company in the

long run; however, low operating margins of Peguform Group (4.9% in CY2010 as

against 6.5% for SMR and 11% for consolidated operations) remain a near-term concern.

Currently, we are not incorporating Peguform’s acquisition into our financials as we await

more information on management’s strategy and turnaround plan. At `239, MSSL is

trading at rich valuations of 21x and 17.7x FY2012E and FY2013E earnings, respectively.

We recommend Neutral on the stock.

1QFY2012 Result Preview

HDFC Bank

HDFC Bank is scheduled to announce its 1QFY2012 results. We expect the bank to report

healthy NII growth of 25.9% yoy to `3,023cr, in spite of the expected NIM moderation.

Non-interest income is expected to register growth of 23.1% yoy, leading to operating

income growth of 25.1% yoy. Due to relatively faster rise in operating expenses, pre-

provision profit is expected to grow by relatively lower 22.1% yoy. However, provisions are

expected to decline marginally by 1.8% yoy, leading to healthy net profit growth of 32.2%

yoy to `1,073cr. At the CMP, we believe the stock is trading at fair valuations of 3.4x

FY2013E P/ABV. We maintain our Neutral recommendation on the stock.

Cadila Healthcare

For 1QFY2012, Cadila Healthcare (Cadila) is expected to post sales and adjusted net

profit of `1,281cr and `179cr, registering yoy growth of 21.4% and 35.6%, respectively.

Top-line growth would be mainly driven by domestic sales and exports. On the operating

front, margins would come at 20.5%, almost similar to the 20.7% level in 1QFY2011. At

the CMP, the stock trades at 25.1x FY2012E and 18.4xFY2013E earnings, respectively. We

recommend Accumulate with a target price of `1,053.

Crompton Greaves

Crompton Greaves is scheduled to announce its 1QFY2012 results. The company’s

revenue is expected to increase by 8% yoy to `2,486cr. On the operating front, we expect

the margin to compress by 42bp yoy to 12.5%. Net profit is expected to decline by 4.3%

yoy to `183cr. The stock is currently trading at 15.9x FY2012E and 13x FY2013E earnings.

We will revisit our estimates post the conference call. Currently, we maintain our Buy rating

on the stock with a target price of `300.

Ashok Leyland

Ashok Leyland (ALL) is slated to announce its 1QFY2012 results. We expect the company’s

top line to grow modestly by 7% yoy, driven by growth in average net realisation as

volumes during the quarter witnessed a 10% decline. On the operating front, EBITDA

margin is expected to post a decline of 53bp yoy to 9.5%, owing to higher raw-material

cost and lower operating leverage. As a result, the bottom line is expected to decline by

17% yoy to `102cr. The stock rating is under review.

July 19, 2011 2

3. Market Outlook | India Research

Economic and Political News

IIP base revision to up FY11 GDP estimates to 8.9%: Crisil

Indian consumer confidence declines in 2QCY2011: AC Nielsen survey

MSME business confidence declines for July–September quarter: CII

Corporate News

PFC to raise `22,000cr from tax-free infrastructure bonds

L&T Finance's `1,750cr IPO to open on July 26

iGate Patni bags `133cr IT deal from US firm

Glenmark Pharmaceuticals gets USFDA nod for anti-ulcer capsules

Steel Strip Wheels bags US$33mn order from BMW

Source: Economic Times, Business Standard, Business Line, Financial Express, Mint

Events for the day

Ashok Leyland Results

Cadila Healthcare Results

Chambal Fertilizers Results

Crompton Greaves Results

Greenply Industries Results

HDFC Bank Results

NIIT Technologies Results

SKF India Results

July 19, 2011 3

4. Market Outlook | India Research

Research Team Tel: 022-3935 7800 E-mail: research@angelbroking.com Website: www.angelbroking.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make investment

decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this document are

those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources

believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this document is for

general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way responsible for any loss or

damage that may arise to any person from any inadvertent error in the information contained in this report. Angel Broking Limited has

not independently verified all the information contained within this document. Accordingly, we cannot testify, nor make any representation

or warranty, express or implied, to the accuracy, contents or data contained within this document. While Angel Broking Limited

endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory, compliance, or other

reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or other

advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and its affiliates may have

investment positions in the stocks recommended in this report.

Ratings (Returns): Buy (> 15%) Accumulate (5% to 15%) Neutral (-5 to 5%)

Reduce (-5% to 15%) Sell (< -15%)

Address: 6th Floor, Ackruti Star, Central Road, MIDC, Andheri (E), Mumbai - 400 093.

Tel: (022) 3935 7800

Angel Broking Ltd: BSE Sebi Regn No : INB 010996539 / CDSL Regn No: IN - DP - CDSL - 234 - 2004 / PMS Regn Code: PM/INP000001546

Angel Capital & Debt Market Ltd: INB 231279838 / NSE FNO: INF 231279838 / NSE Member code -12798 Angel Commodities Broking (P) Ltd: MCX Member ID: 12685 / FMC Regn No: MCX / TCM /

CORP / 0037 NCDEX : Member ID 00220 / FMC Regn No: NCDEX / TCM / CORP / 0302

July 19, 2011 4