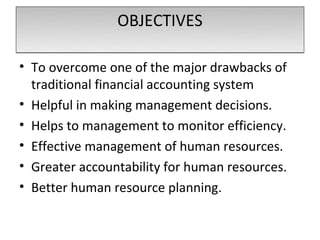

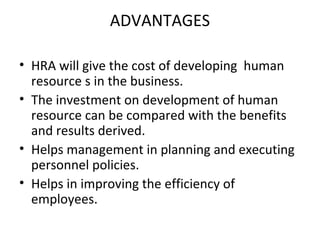

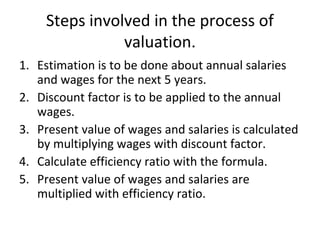

Human resource accounting aims to identify and measure data about human resources and communicate this information to interested parties. It helps address drawbacks in traditional financial accounting and assists management with decision making, monitoring efficiency, and human resource planning. Various models have been proposed to account for human resources, including historical cost, replacement cost, and opportunity cost models which value human resources differently. More recent models aim to determine the present value of future earnings and services provided by human resources to value this important organizational asset. However, human resource accounting continues to face challenges in implementation due to difficulties in measurement and lack of standardization.