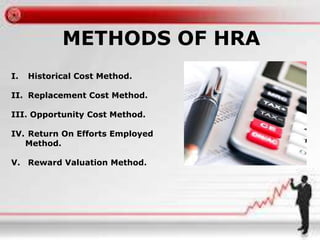

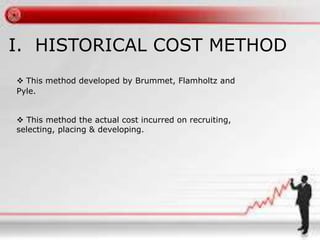

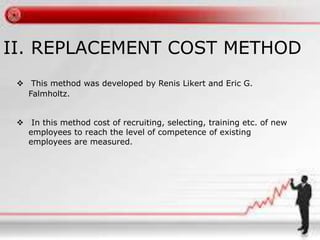

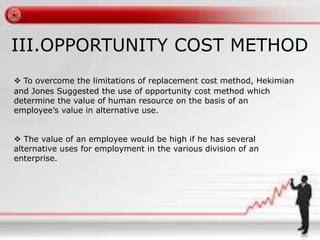

This document discusses human resource accounting (HRA), which involves identifying and measuring data about a company's human resources and communicating this information. It defines HRA and lists its objectives such as improving management and considering people as assets. The document also outlines advantages like helping with staffing decisions and identifying underutilized resources. Disadvantages include assumptions in valuing human assets and potential employee discouragement. Several methods of HRA are described, including historical cost and replacement cost approaches. Finally, it examines the costs associated with human resources like acquisition, training, welfare, and health and safety.

![Business environment {UNCTAD]](https://cdn.slidesharecdn.com/ss_thumbnails/bussppt-170305102804-thumbnail.jpg?width=640&height=640&fit=bounds)

![Hacking-Uncovered-How-People-Get-Hacked-and-How-to-Stay-Safe[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/hacking-uncovered-how-people-get-hacked-and-how-to-stay-safe1-260130170011-4883a9c7-thumbnail.jpg?width=640&height=640&fit=bounds)

![제 23회 보아즈(BOAZ) 빅데이터 컨퍼런스 - [MBOAX] : ABSA를 활용한 소비자 반응 분석 기반 운영 효율화 대시보드 설계](https://cdn.slidesharecdn.com/ss_thumbnails/3-1boaz23rdconferencemboax-260203102709-9d519923-thumbnail.jpg?width=640&height=640&fit=bounds)

![7.__Developing_a_Research_Proposal[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/7-260131073037-df92dd7d-thumbnail.jpg?width=640&height=640&fit=bounds)