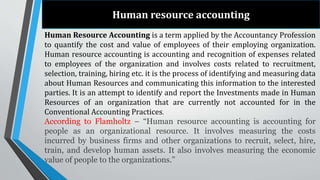

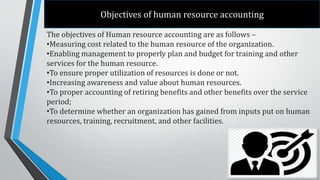

Download to read offline

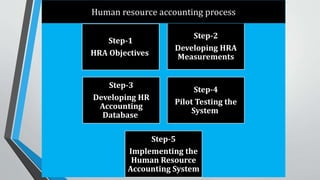

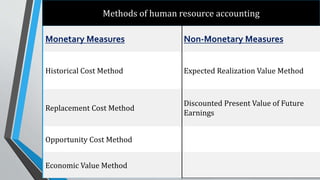

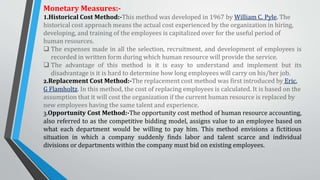

Human resource accounting is a method used to quantify the value of employees to an organization. It involves measuring costs related to recruiting, training, and developing employees. The objectives of human resource accounting are to properly measure and account for costs associated with human resources, ensure resources are being utilized effectively, and determine if investments in employee training and development are providing a return to the organization. Some common methods used in human resource accounting are the historical cost method, replacement cost method, and economic value method, which assign monetary values to employees based on past costs or future earnings potential. Non-monetary methods include the expected realization value method and discounted present value of future earnings method.