Downloaded 28 times

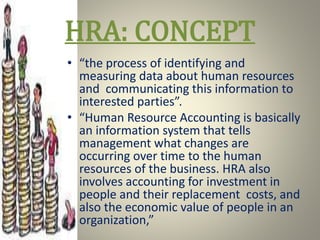

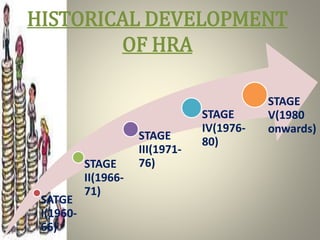

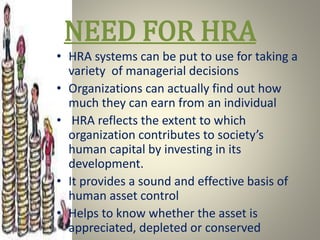

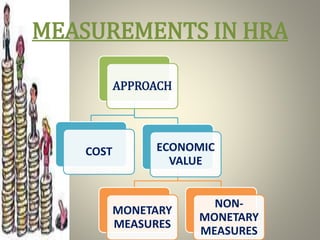

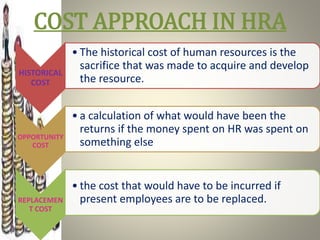

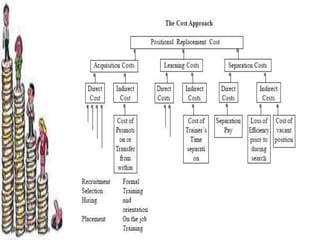

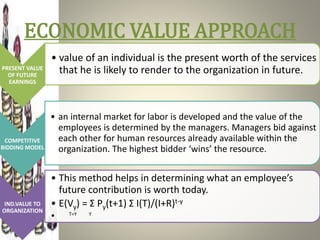

This document discusses human resource accounting (HRA). It defines HRA as identifying and measuring data about human resources and communicating it to management. HRA involves accounting for investments in employee development and their replacement costs, as well as the economic value employees provide. The document outlines the historical development of HRA, need for HRA, common measurement approaches including cost and economic value, specific valuation methods under each approach, and deterrents to implementing HRA.