Downloaded 25 times

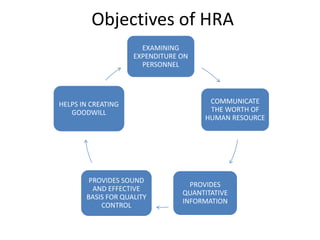

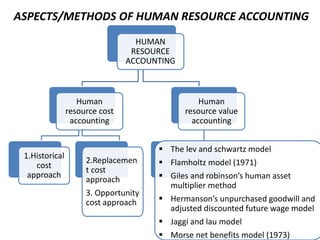

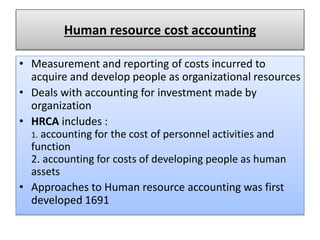

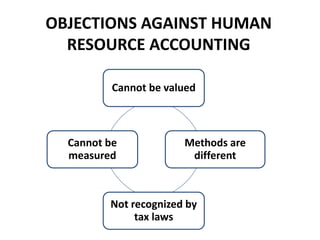

Human resource accounting involves measuring the cost and value of people to an organization. It includes measuring recruitment, training, and development costs incurred by the organization and assessing the economic value employees provide. There are two main aspects of human resource accounting: human resource cost accounting, which accounts for investment in developing human resources, and human resource value accounting, which assigns monetary values to human assets. Various approaches to valuing human resources include historical cost, replacement cost, and opportunity cost approaches. While human resource accounting provides useful information for decision making, there are also limitations such as uncertainty around employee tenure and lack of standardized valuation methods.