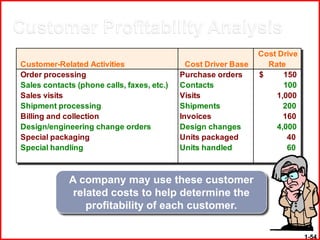

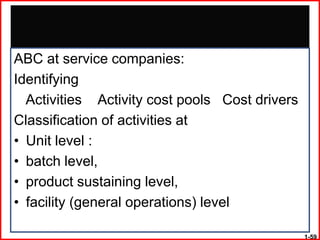

Downloaded 922 times

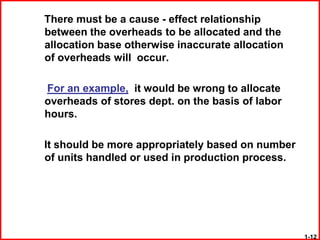

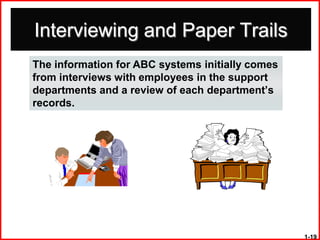

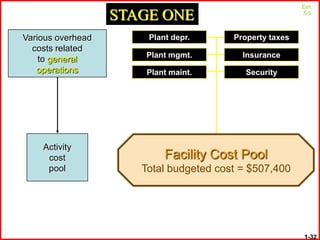

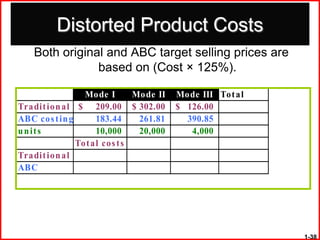

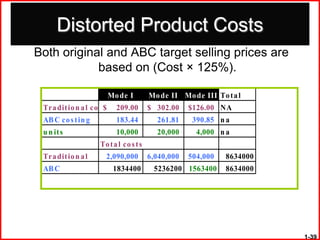

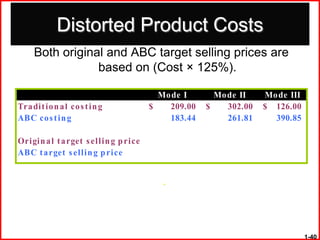

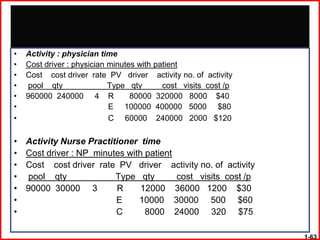

![Distorted Product Costs

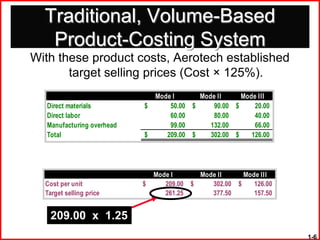

Both original and ABC target selling prices are

based on (Cost × 125%).

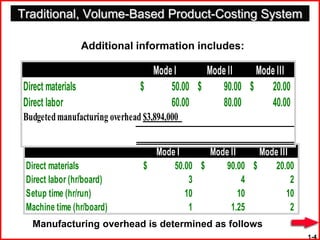

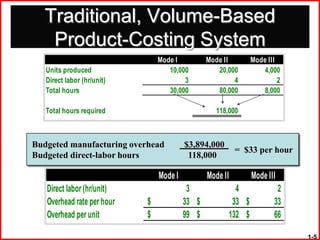

Mode I Mode II Mode III

Tradition al cos tin g $ 209.00 $ 302.00 $ 126.00

ABC cos tin g 183.44 261.81 390.85

Origin al targe t s e llin g price 261.25 377.50 157.50

ABC targe t s e llin g price 229.30 327.26 488.56

The selling price of Mode I and II are reduced

and the selling price for Mode III is increased.

[$209.00 × 1.25] [$183.44 × 1.25]

1-41](https://image.slidesharecdn.com/activity-based-costing-120805032129-phpapp01/85/Activity-based-costing-41-320.jpg)

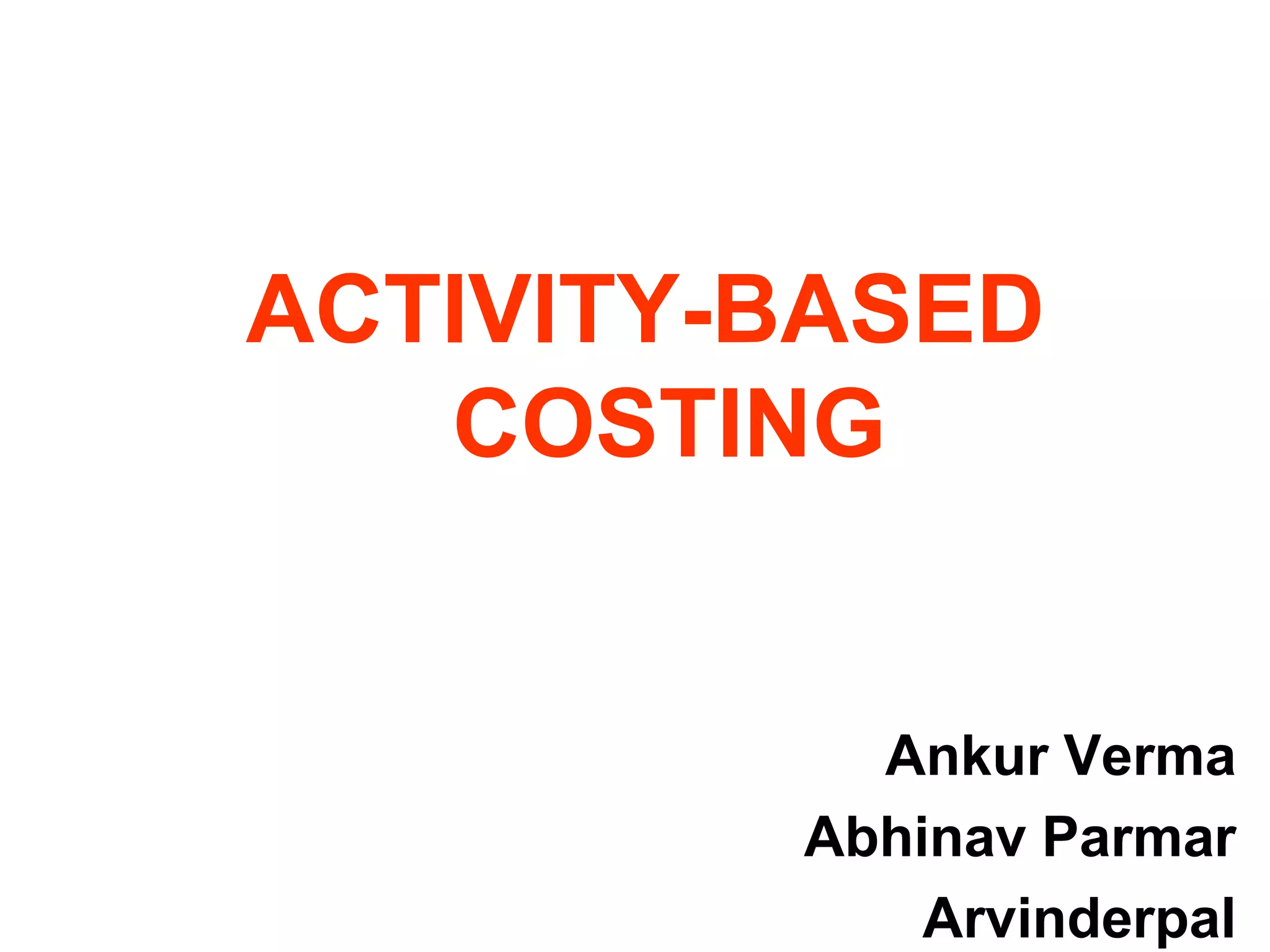

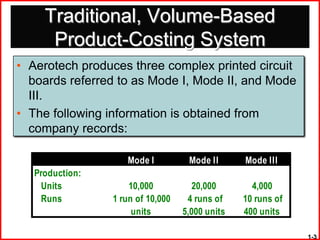

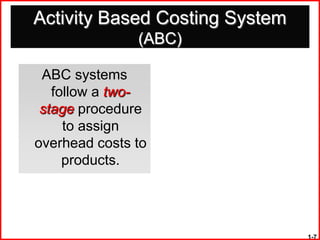

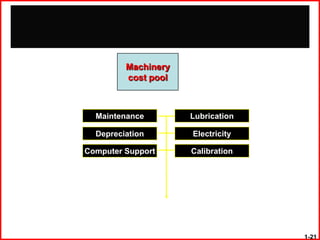

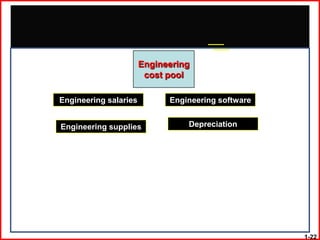

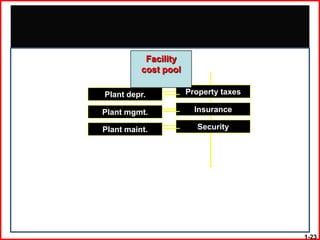

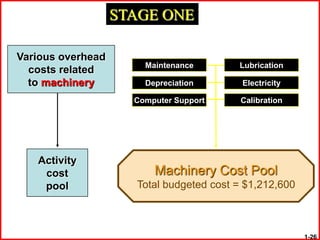

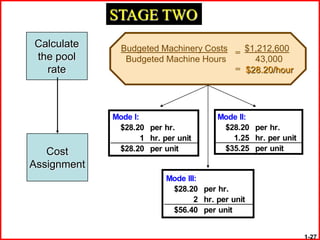

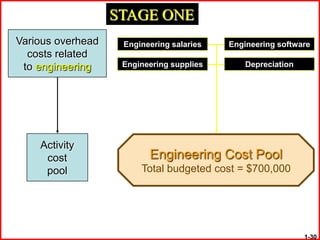

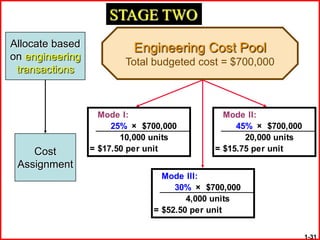

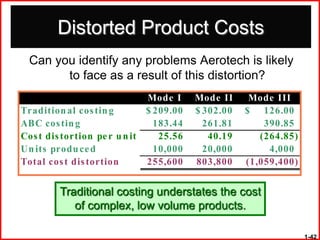

1) ABC identifies activities associated with overhead costs and assigns costs to each activity. 2) Costs are then allocated to products based on cost drivers for each activity that influence the costs. 3) For Aerotech, activities included machinery, setup, engineering, and facilities. Costs for each activity were assigned to products based on relevant cost drivers like machine hours or engineering transactions. This provided a more accurate allocation of overhead costs than traditional volume-based methods.