Downloaded 247 times

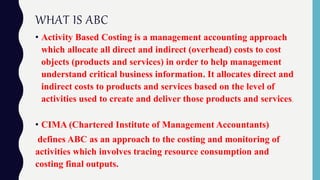

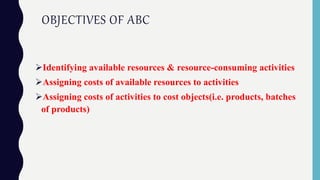

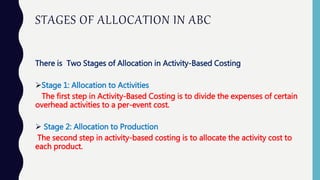

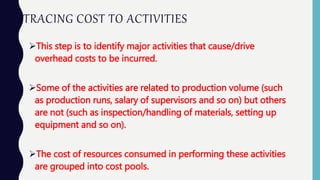

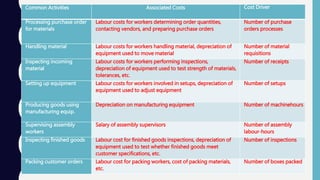

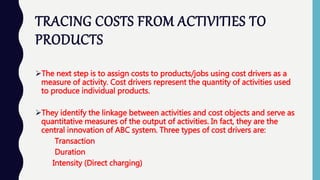

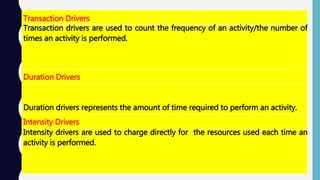

Activity-based costing (ABC) is a management accounting approach that allocates overhead costs to products and services based on the activities consumed and resources used to produce them. It identifies major activities in a company and traces the costs of each activity back to the products. There are two stages - costs are first allocated to activities, then activities are allocated to products using cost drivers that represent consumption of activities. ABC provides more accurate product costs than traditional volume-based allocation and helps identify unprofitable products. It is useful when overhead costs are significant or product complexity varies widely.