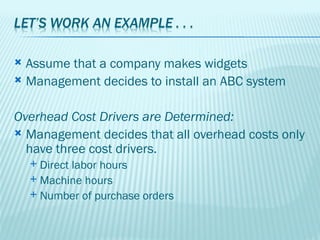

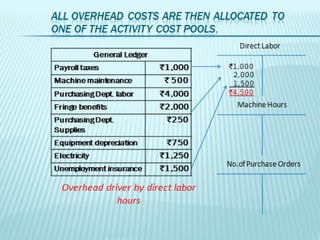

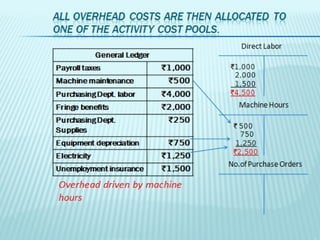

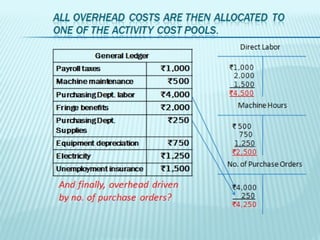

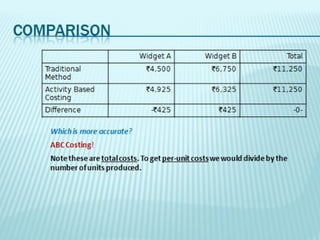

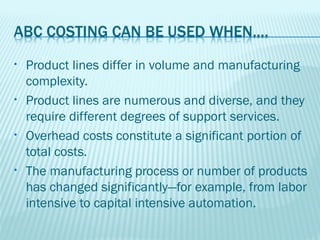

The document discusses activity based costing (ABC) and how it addresses limitations of traditional costing methods. It explains that ABC allocates overhead costs to products based on multiple cost drivers like direct labor hours, machine hours, and number of purchase orders rather than a single driver. This provides a more accurate reflection of how overhead resources are consumed. The document provides an example to illustrate how ABC can allocate overhead costs differently than traditional methods based on a single driver.