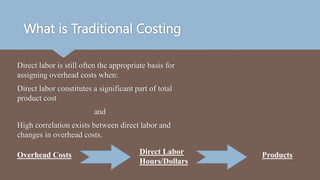

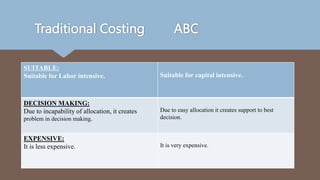

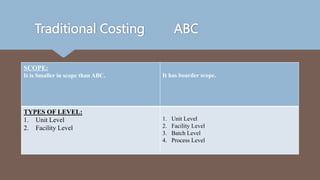

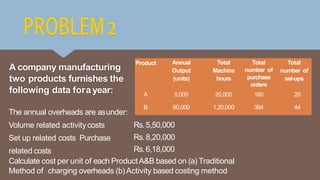

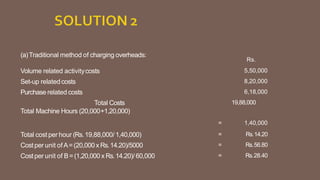

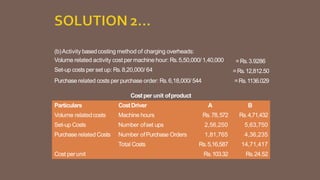

The document presents information on traditional costing vs activity-based costing. It discusses how traditional costing allocates overhead using a single predetermined rate based on direct labor or machine hours. Activity-based costing allocates overhead to multiple cost pools and uses cost drivers to trace costs to products. The key differences between the two methods are discussed, such as traditional costing being more suitable for labor-intensive operations while ABC is more accurate for capital-intensive operations. Examples are provided to demonstrate calculating product costs using both traditional and activity-based costing methods.