Downloaded 374 times

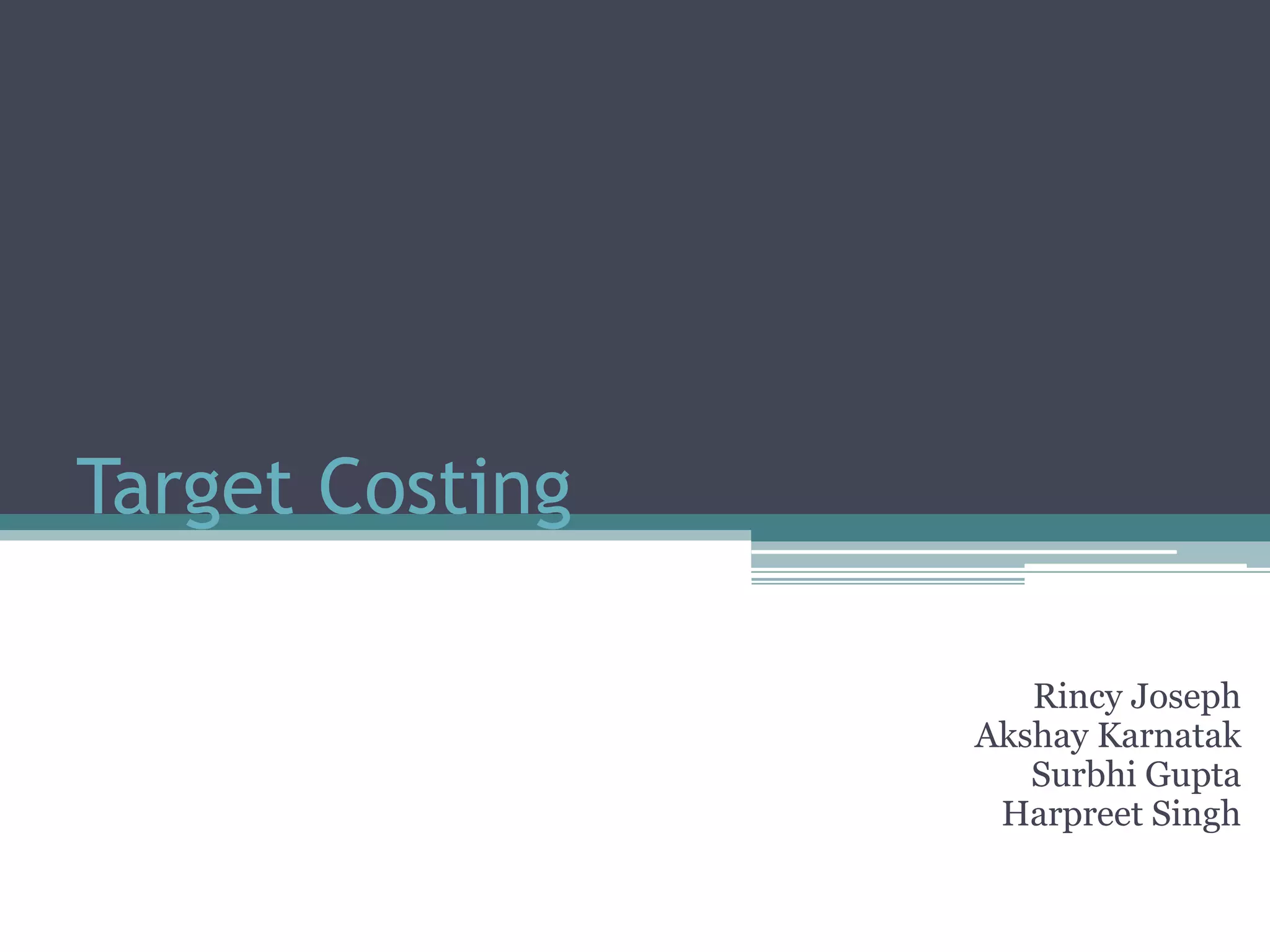

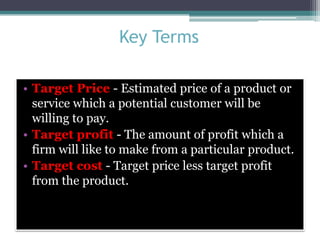

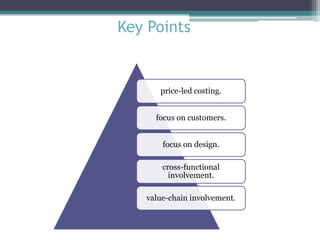

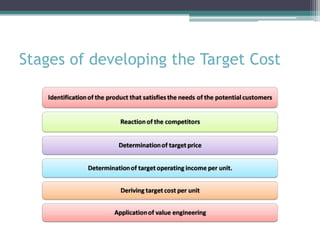

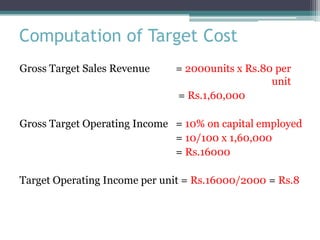

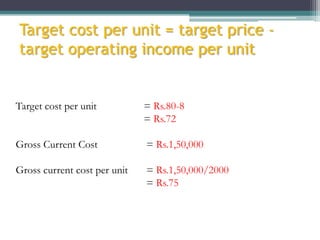

This document discusses target costing, which is a process that develops costs for a product or service based on market considerations like the target price customers will pay. It involves estimating the target price, target profit, and target cost. Target cost is calculated as the target price minus the target profit. The key steps are computing the target cost, setting gross target sales and operating income, then determining the target cost per unit. The benefits are a focus on customers, cross-functional involvement, and commitment to innovation. Potential downsides include delays from overloaded features, and conflicts from pressure to excessively cut costs.