Downloaded 4,471 times

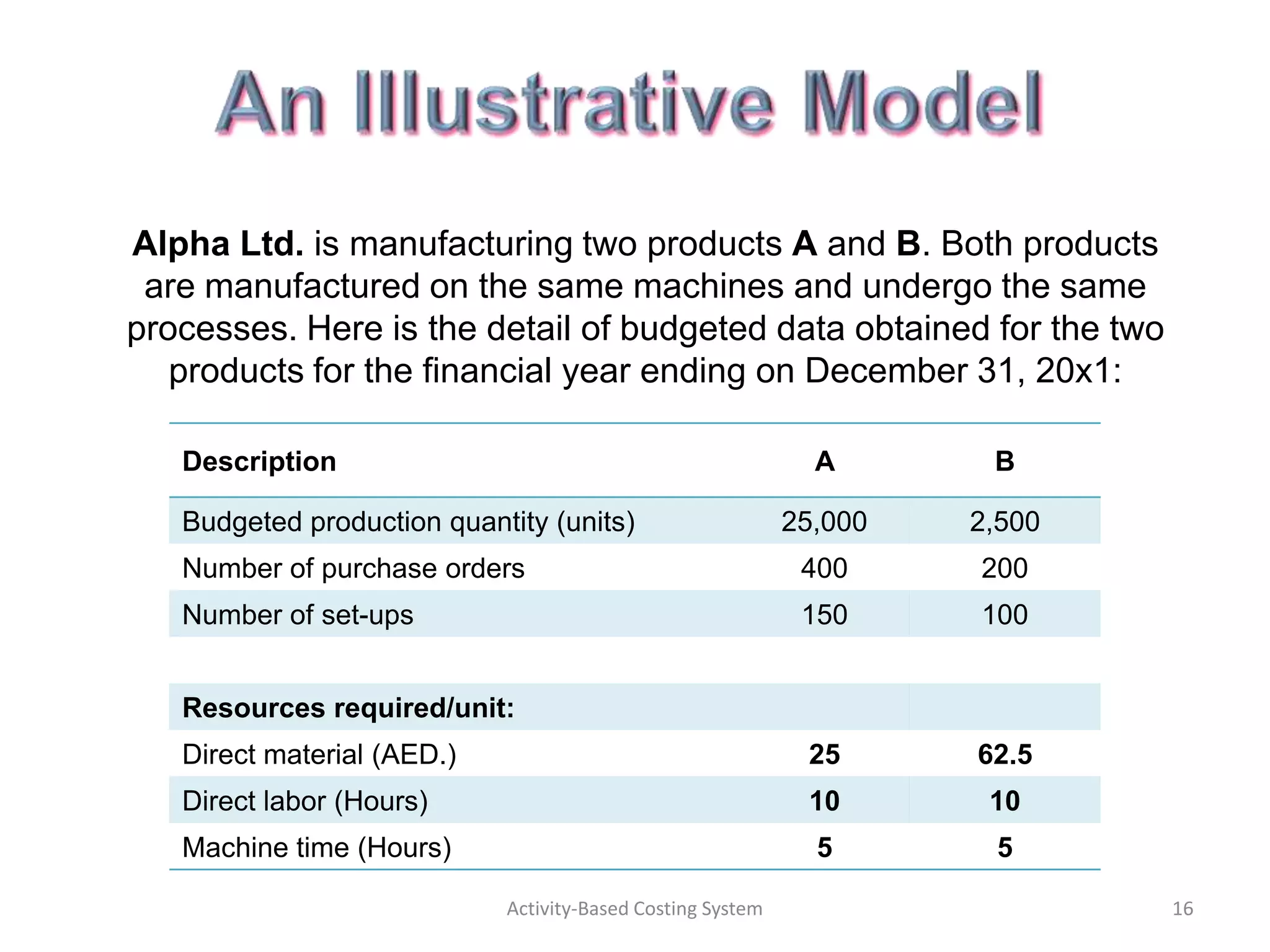

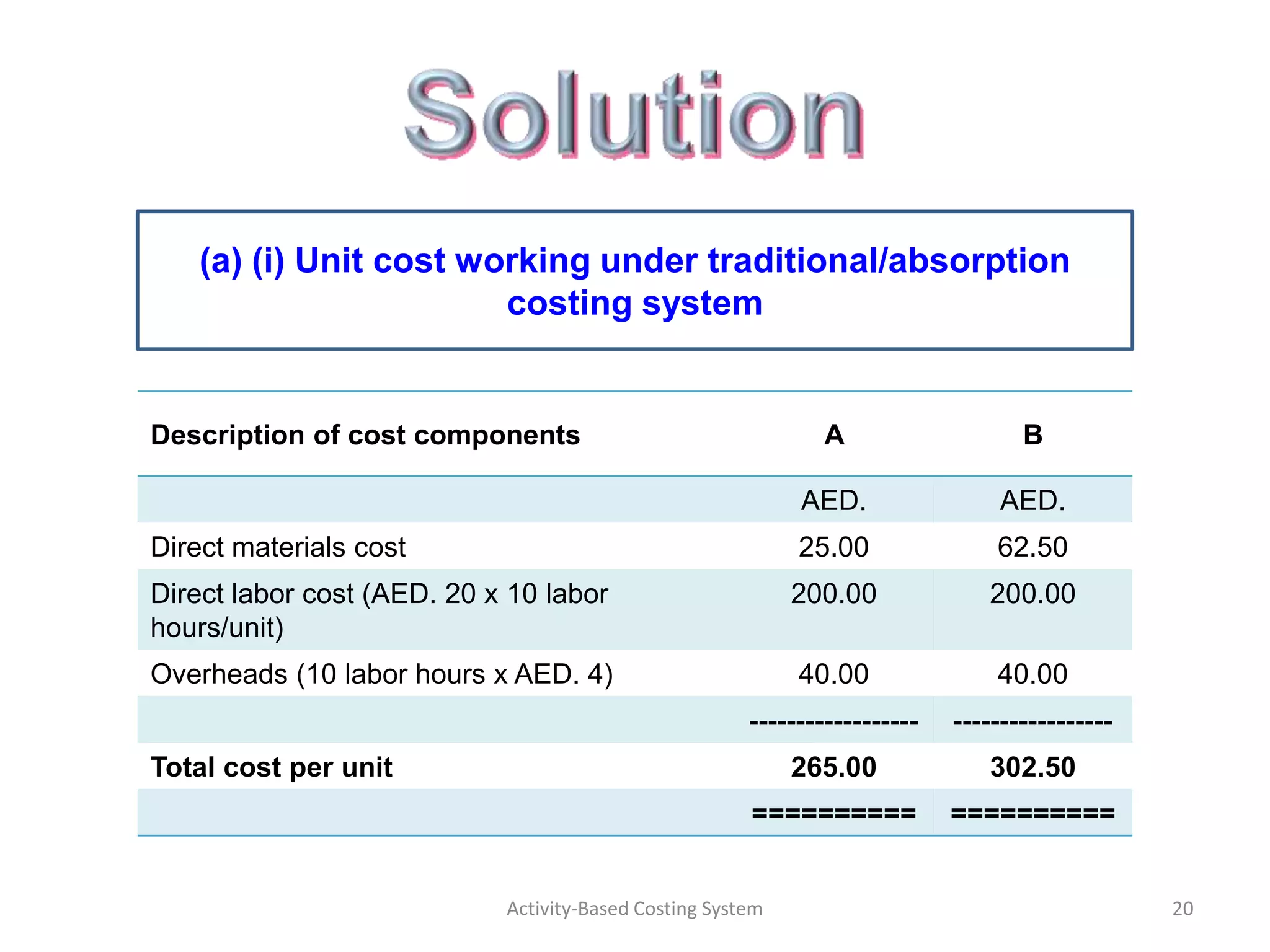

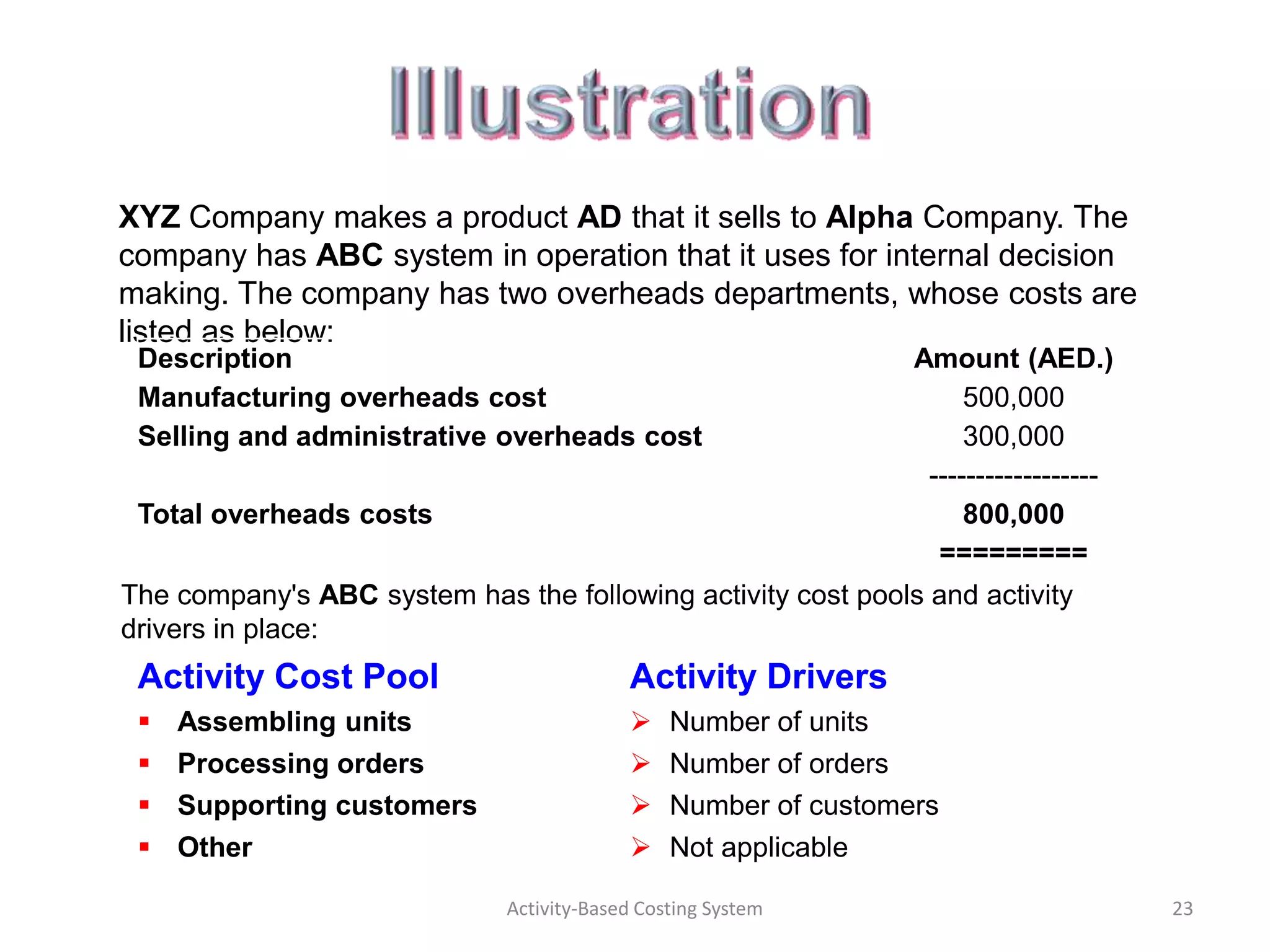

![(a) (ii) Unit cost working under Activity-Based Costing system

Description of cost components A B

AED. AED.

Direct materials cost 25.00 62.50

Direct labor cost 200.00 200.00

Volume related overheads cost (AED. 2 x 5 machine 10.00 10.00

hours/unit)

Purchases related overheads cost:

Product A: [(AED. 500 x 400 Orders)/ 25,000 8

Units] 40

Product B: [(AED. 500 x 200 Orders)/2,500 Units]

Set-up related overheads cost:

Product A: [(AED. 2,100 x 150 Set-ups)/25,000 12.60

Units] 84.00

Product B: [(AED. 2,100 x 100 Set-ups)/25,00 Units]

------- --------

Total cost per unit Activity-Based Costing System 255.60 396.50 21](https://image.slidesharecdn.com/activity-basedcostingsystem-121201022457-phpapp01/75/Activity-Based-Costing-System-21-2048.jpg)

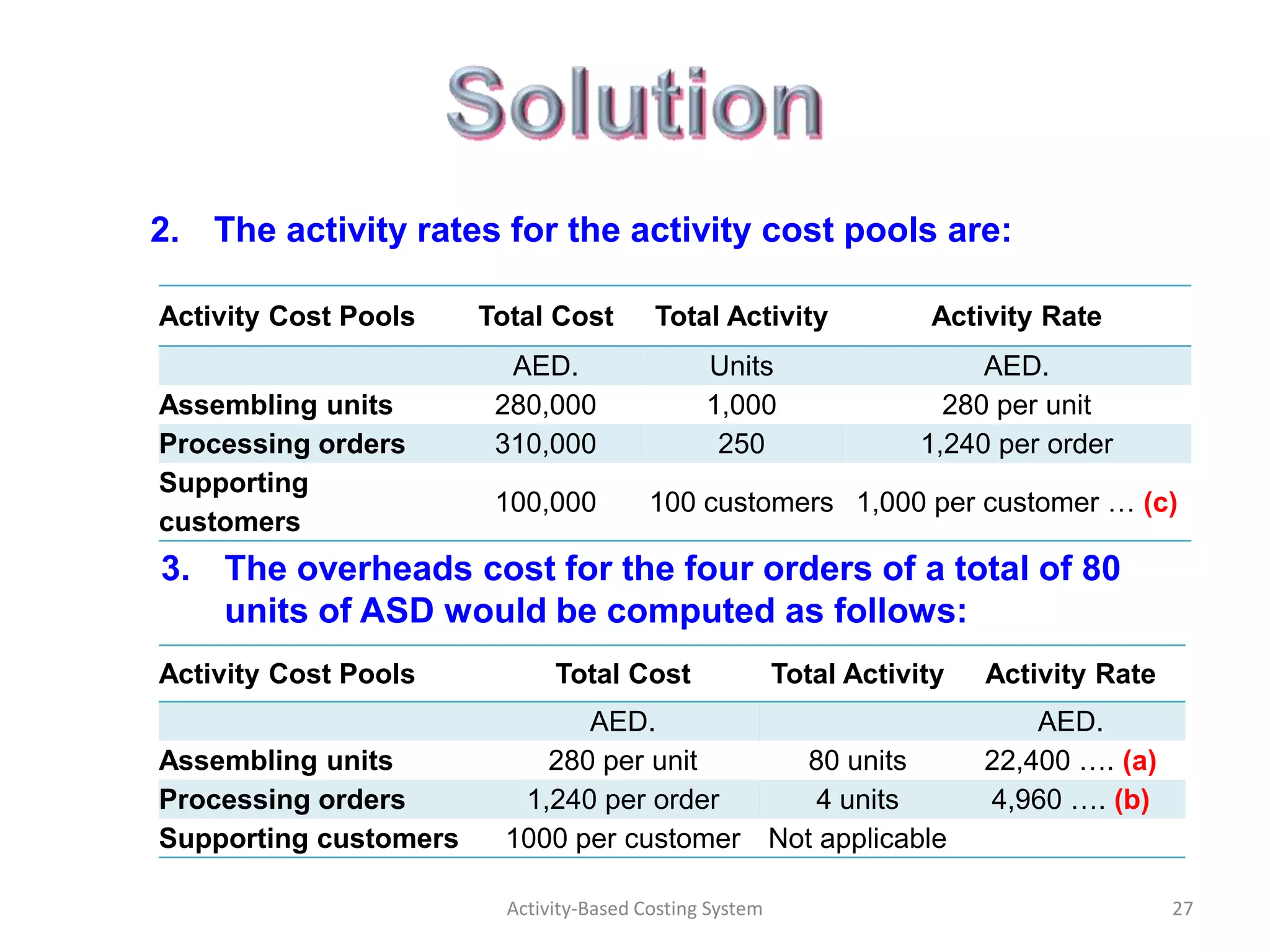

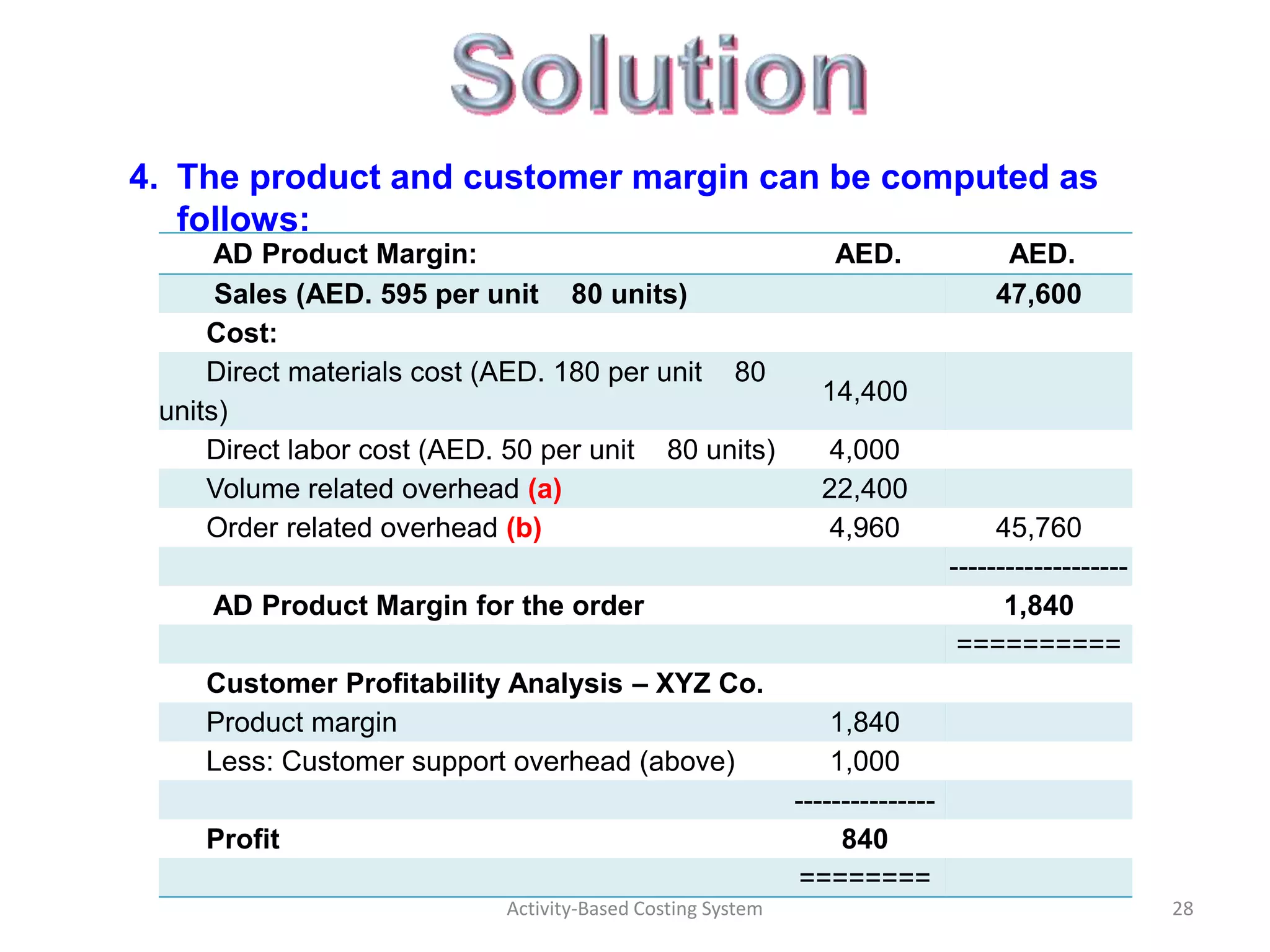

Here are the steps to solve this problem: 2. The activity rates are computed as: Assembling units: AED. 280,000/1,000 units = AED. 280 per unit Processing orders: AED. 310,000/250 orders = AED. 1,240 per order Supporting customers: AED. 100,000/100 customers = AED. 1,000 per customer Activity-Based Costing System 26 3. The table showing overhead costs for VB's 80 units and 4 orders is: Description Amount (AED.) Direct materials cost (80 units x AED. 180) 14,400 Direct labor cost