Downloaded 626 times

![The concepts of ABC were developed in the manufacturing sector of the United States during the 1970s and 1980s. During this time, the Consortium for Advanced Manufacturing-International , now known simply as CAM-I, provided a formative role for studying and formalizing the principles that have become more formally known as Activity-Based Costing. [1]](https://image.slidesharecdn.com/activity-based-costing-1219652252142850-8/85/Activity-Based-Costing-5-320.jpg)

![History [2] They initially focused on manufacturing industry where increasing technology and productivity improvements have reduced the relative proportion of the direct costs of labor and materials, but have increased relative proportion of indirect costs. For example, increased automation has reduced labor, which is a direct cost, but has increased depreciation, which is an indirect cost.](https://image.slidesharecdn.com/activity-based-costing-1219652252142850-8/85/Activity-Based-Costing-9-320.jpg)

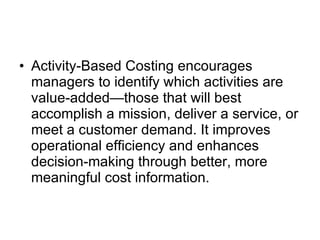

The document discusses activity-based costing (ABC), a method that assigns costs to products and services based on the activities consumed by each. It provides a 4-step process for ABC implementation: 1) identify activities, 2) assign resource costs to activities, 3) identify outputs, and 4) assign activity costs to outputs using cost drivers. ABC aims to more accurately determine costs by tracing them to specific causes like production activities rather than allocating overhead broadly.