Downloaded 347 times

This document discusses key concepts in cost accounting, including the meaning and objectives of cost accounting, the relationship between cost accounting and other types of accounting, elements of cost like direct and indirect costs, and cost classification. It defines important cost accounting terms and concepts, explains the general principles and advantages/limitations of cost accounting, and describes how a cost sheet is used to analyze costs.

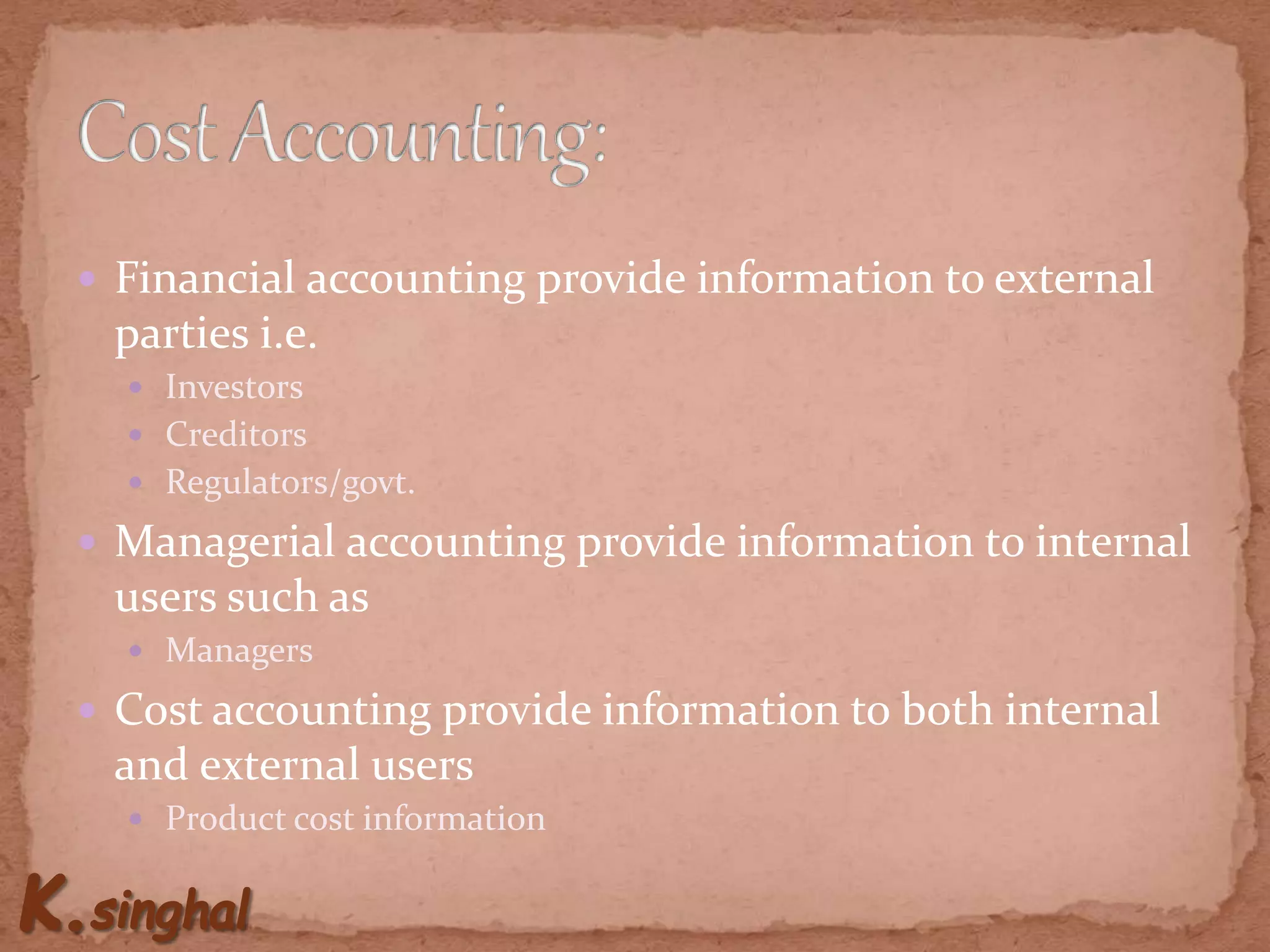

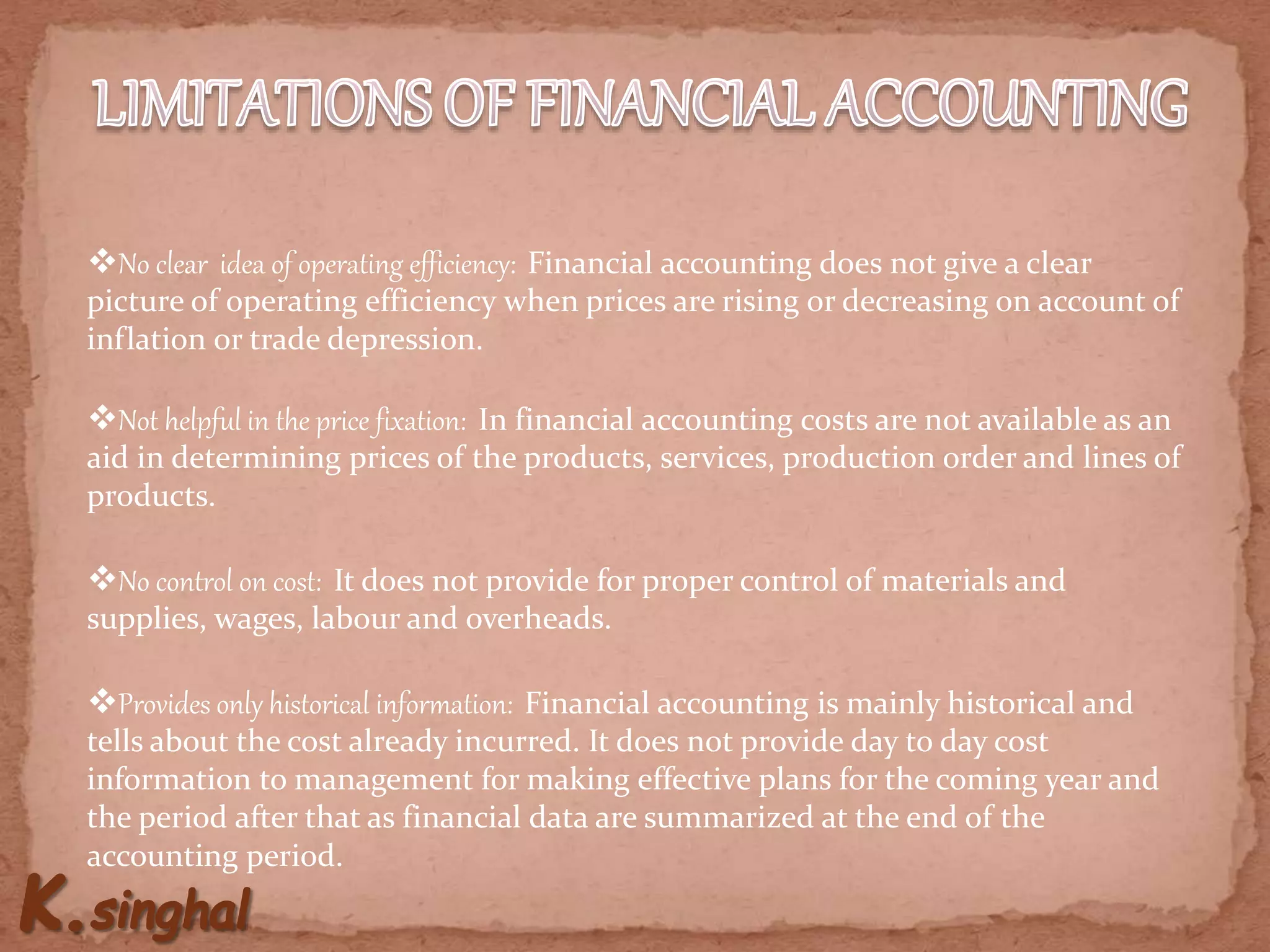

Introduction to cost accounting's meaning, scope, limitations, and relationship with management and financial accounting.

Introduction to cost accounting's meaning, scope, limitations, and relationship with management and financial accounting.

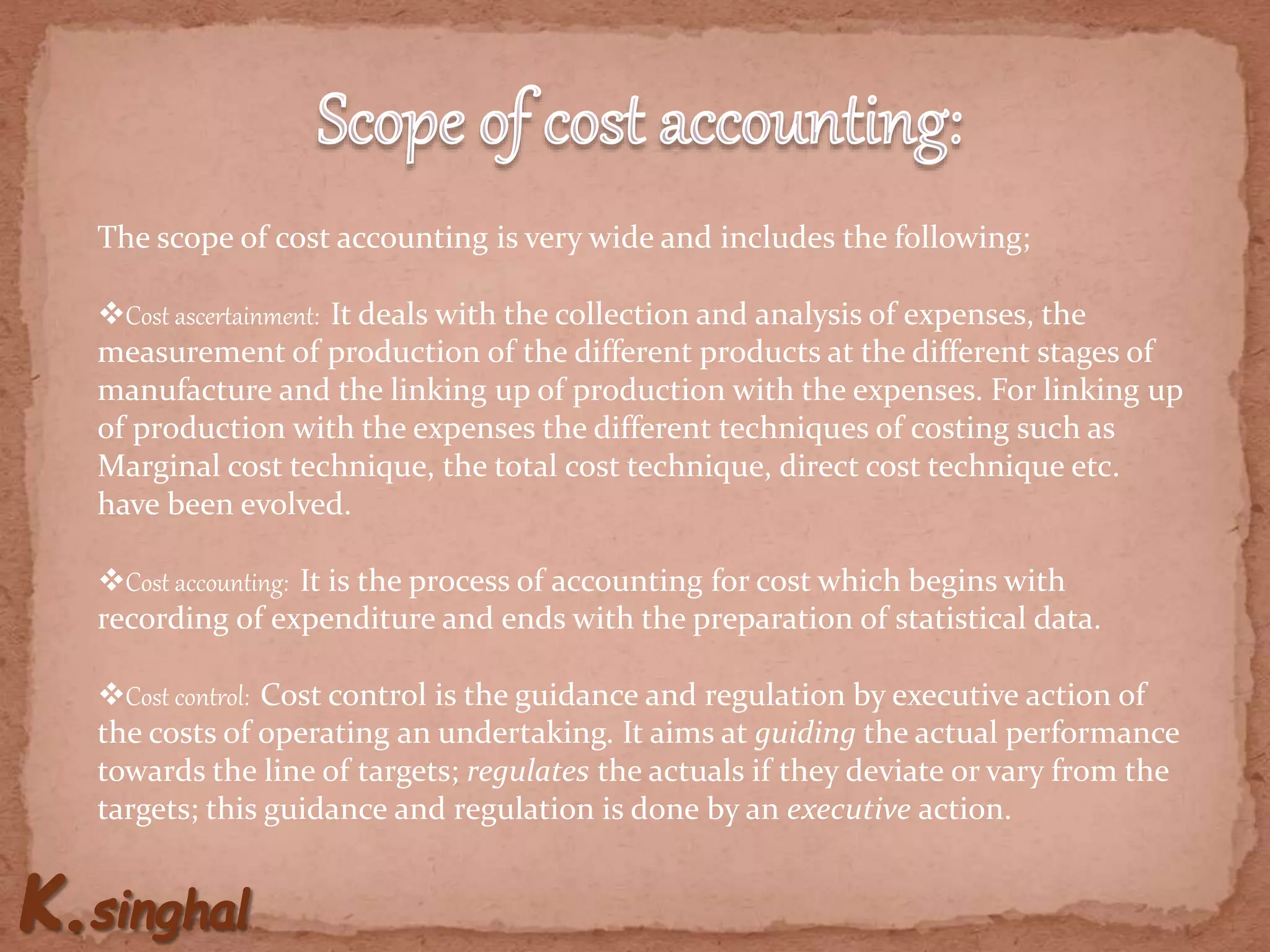

Goals of cost accounting include cost ascertainment, control, and providing data for management decisions.

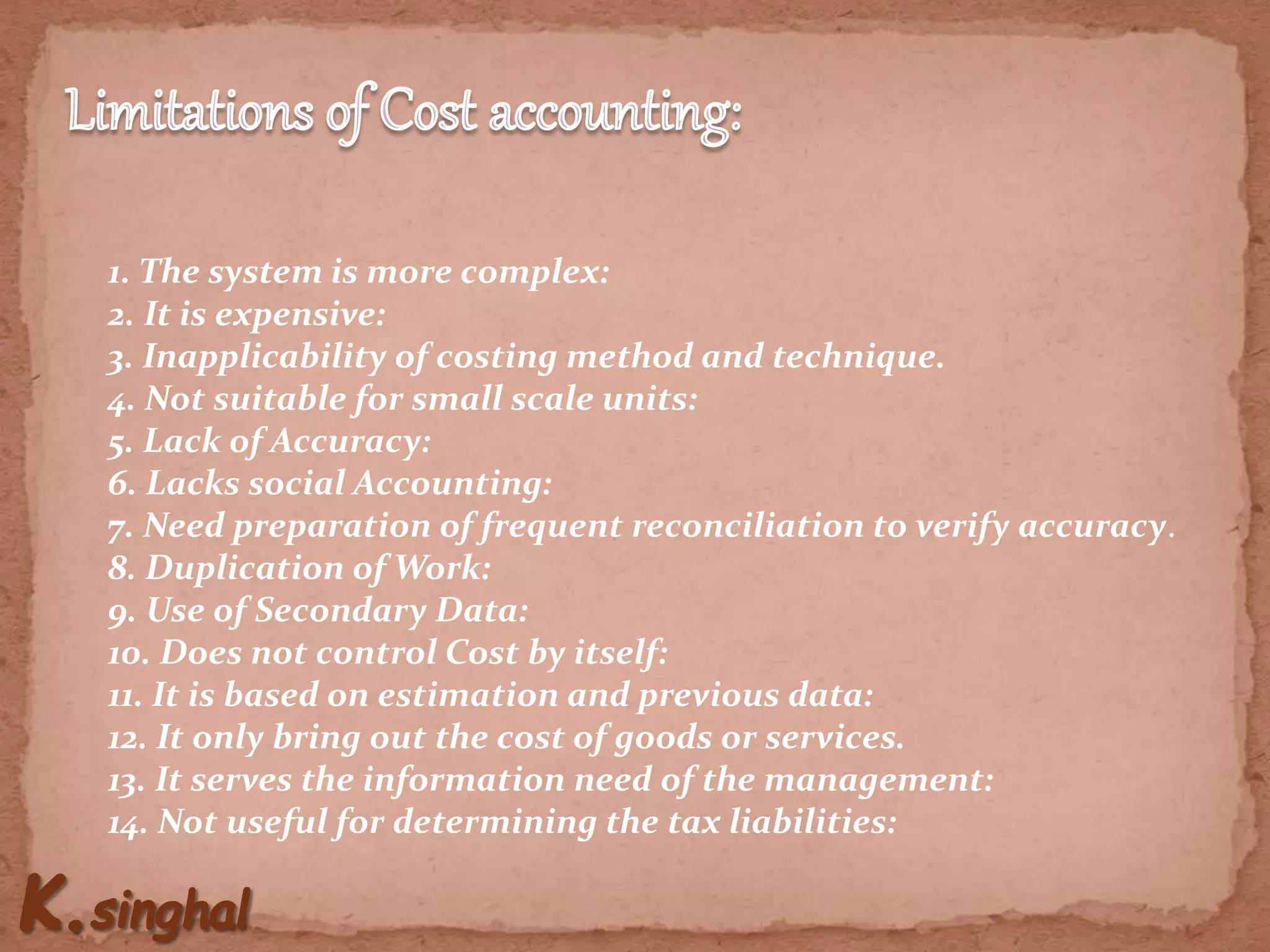

Highlights benefits like identifying profitability and challenges such as complexity and costliness.

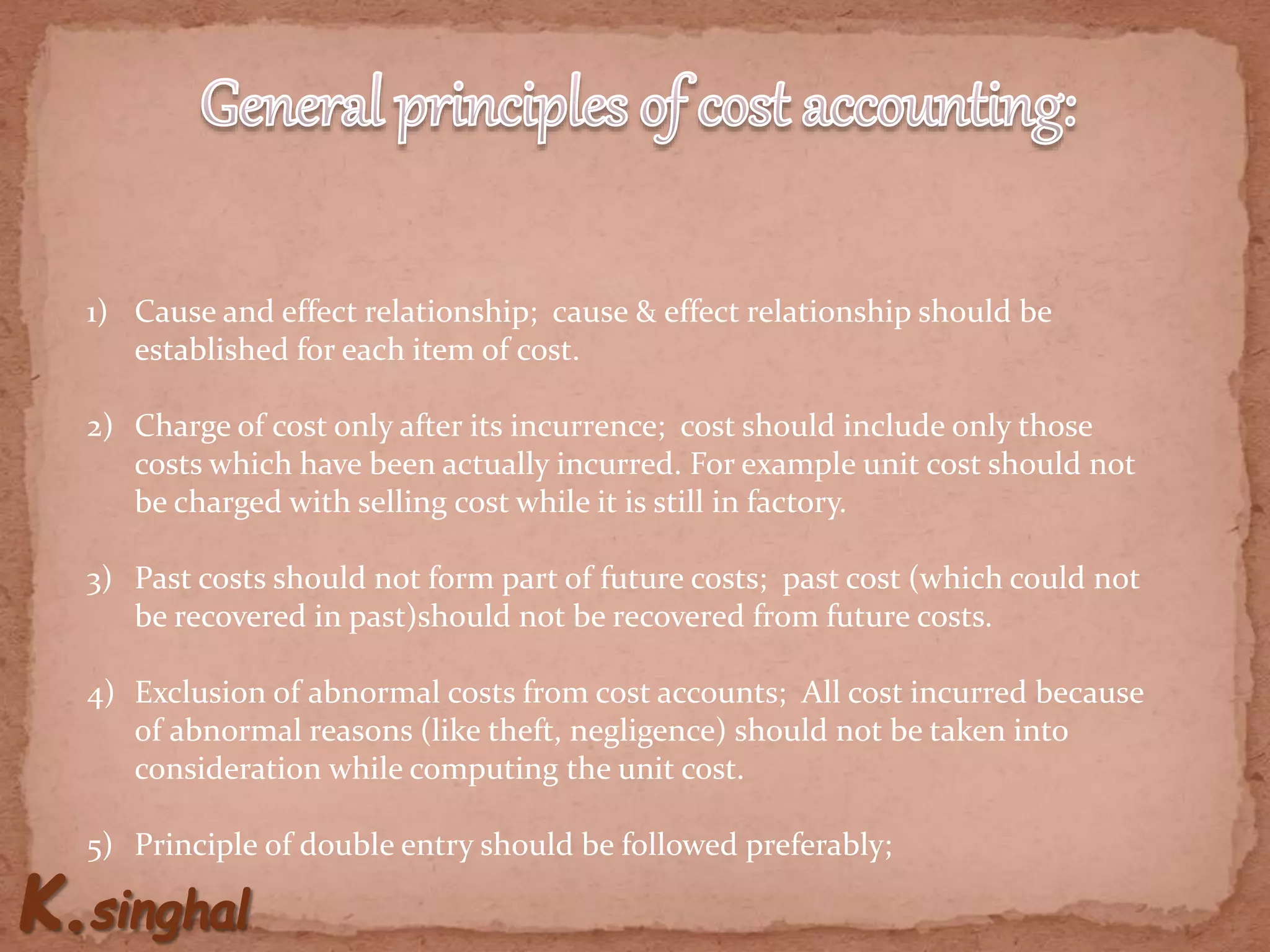

Fundamental principles guiding cost accounting practices to ensure accuracy and relevance of cost data.

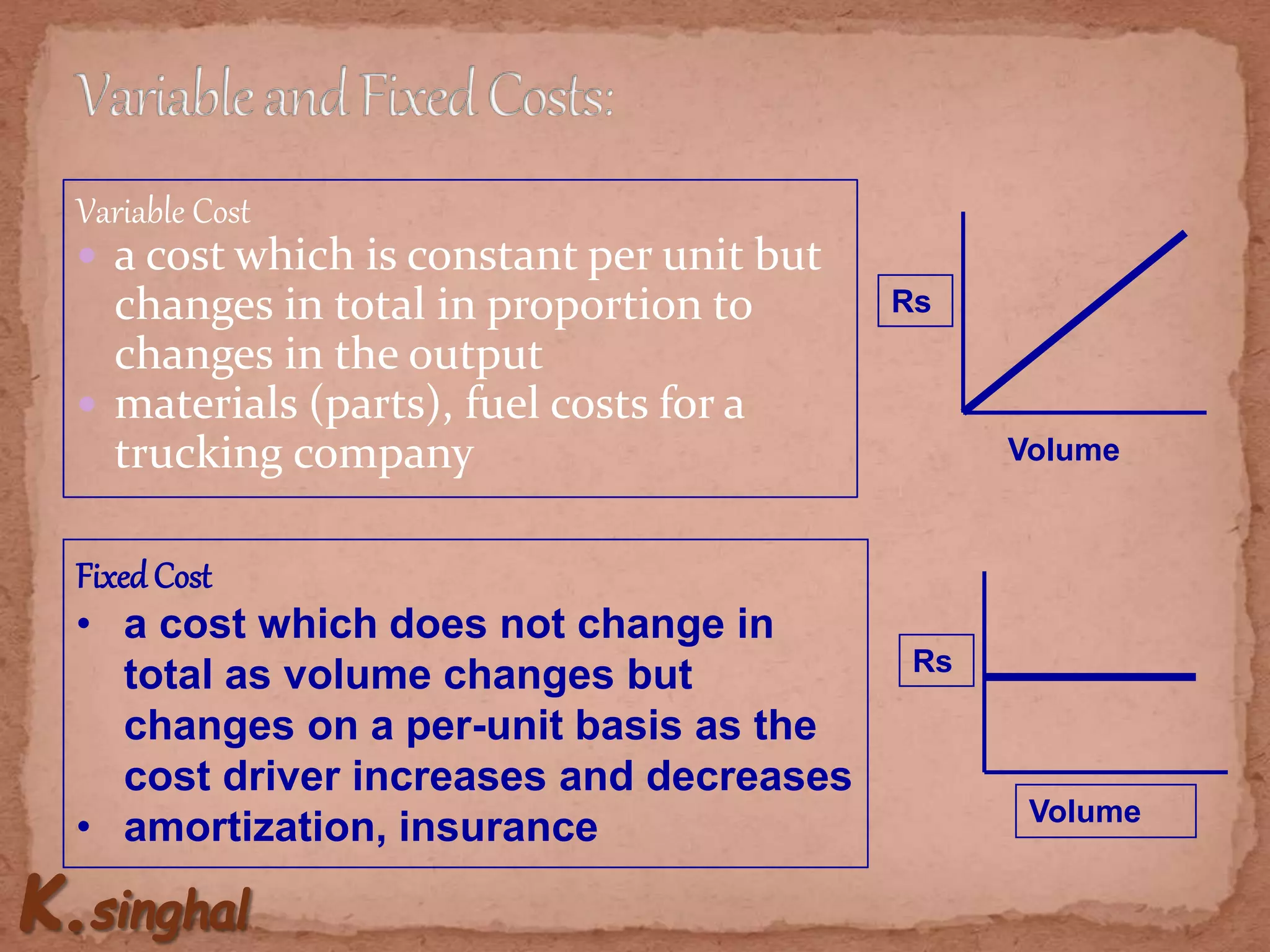

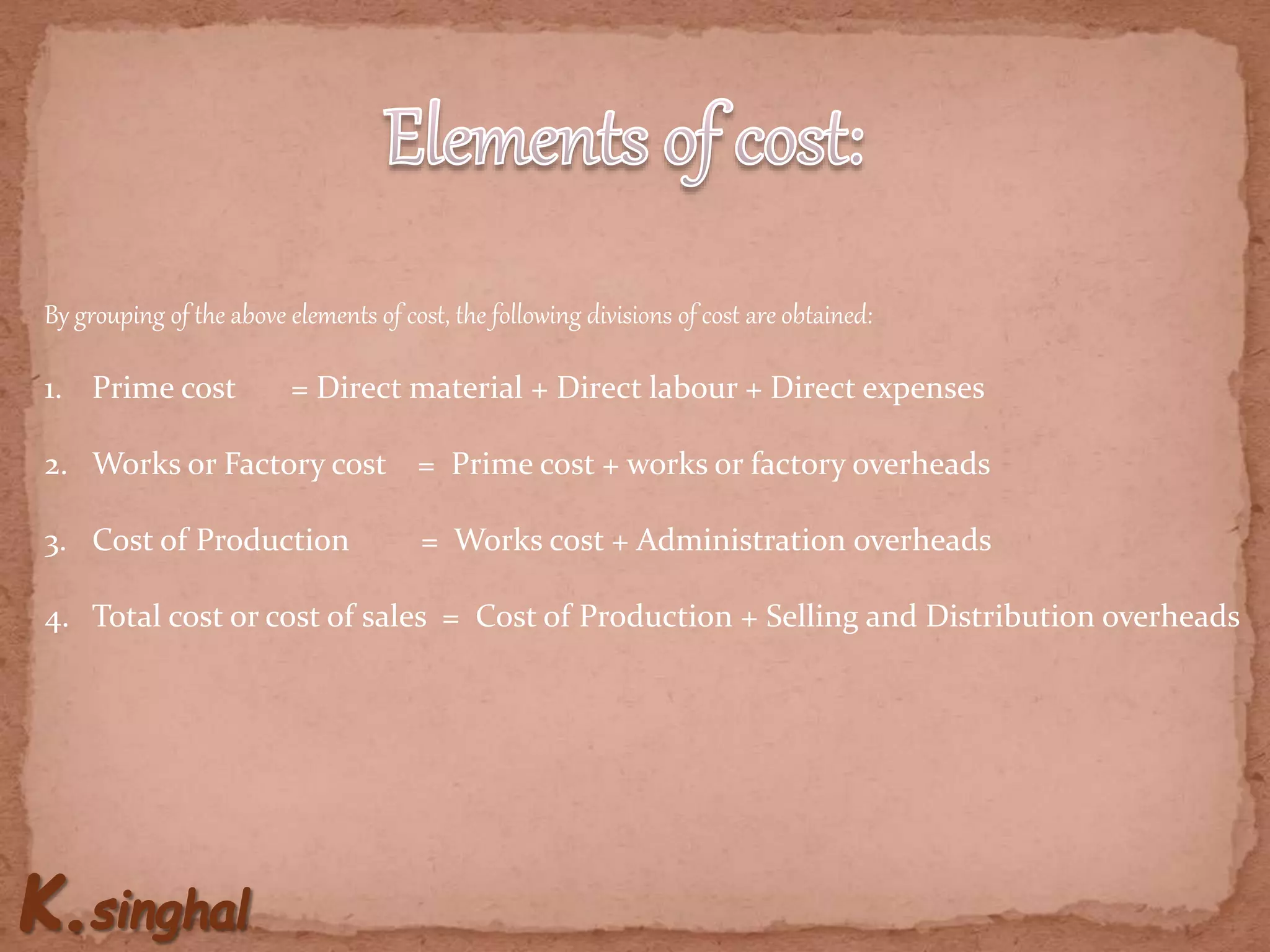

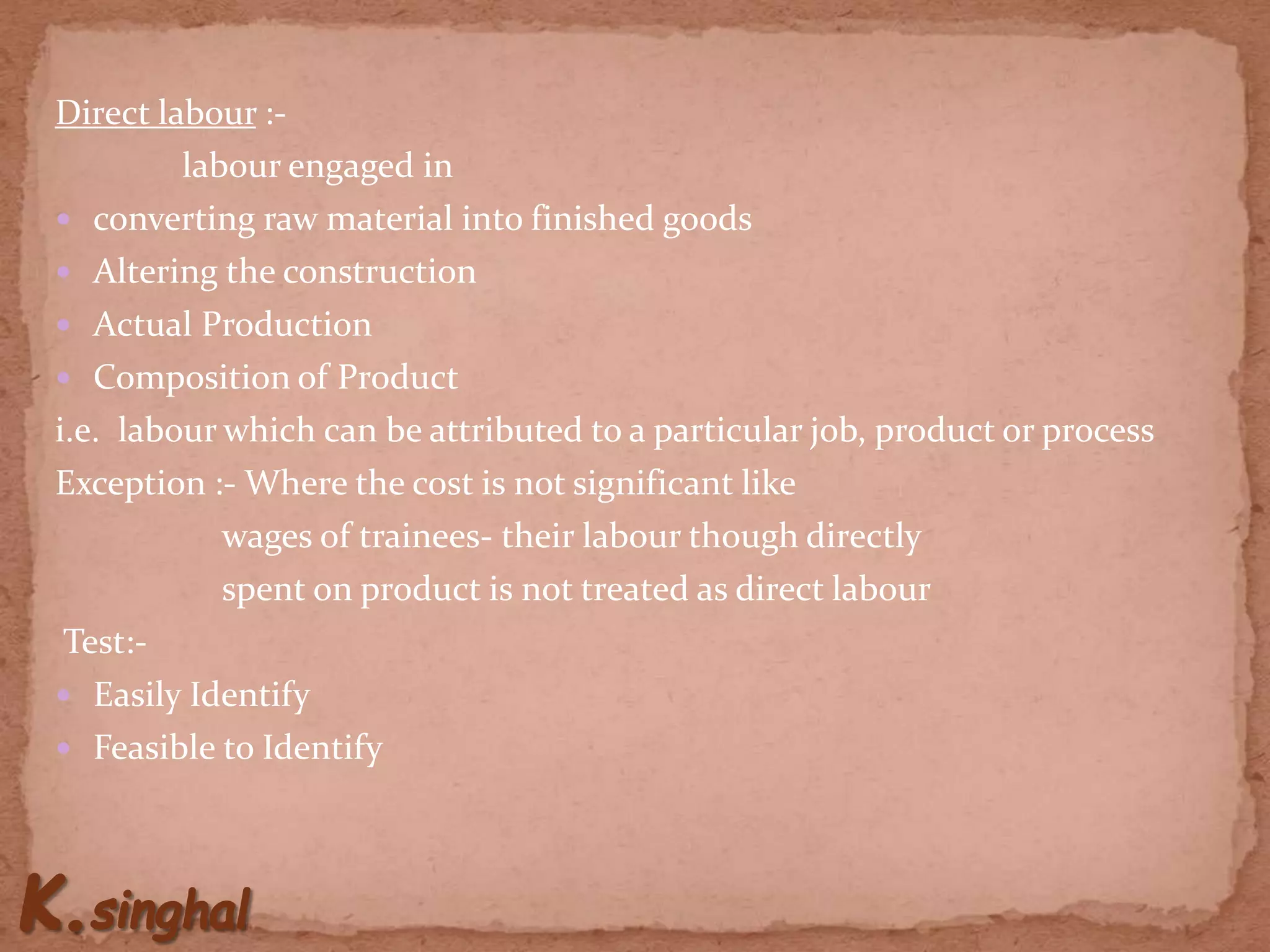

Breakdown of costs into prime, factory, and total costs with definitions of direct material, labor, and overheads.

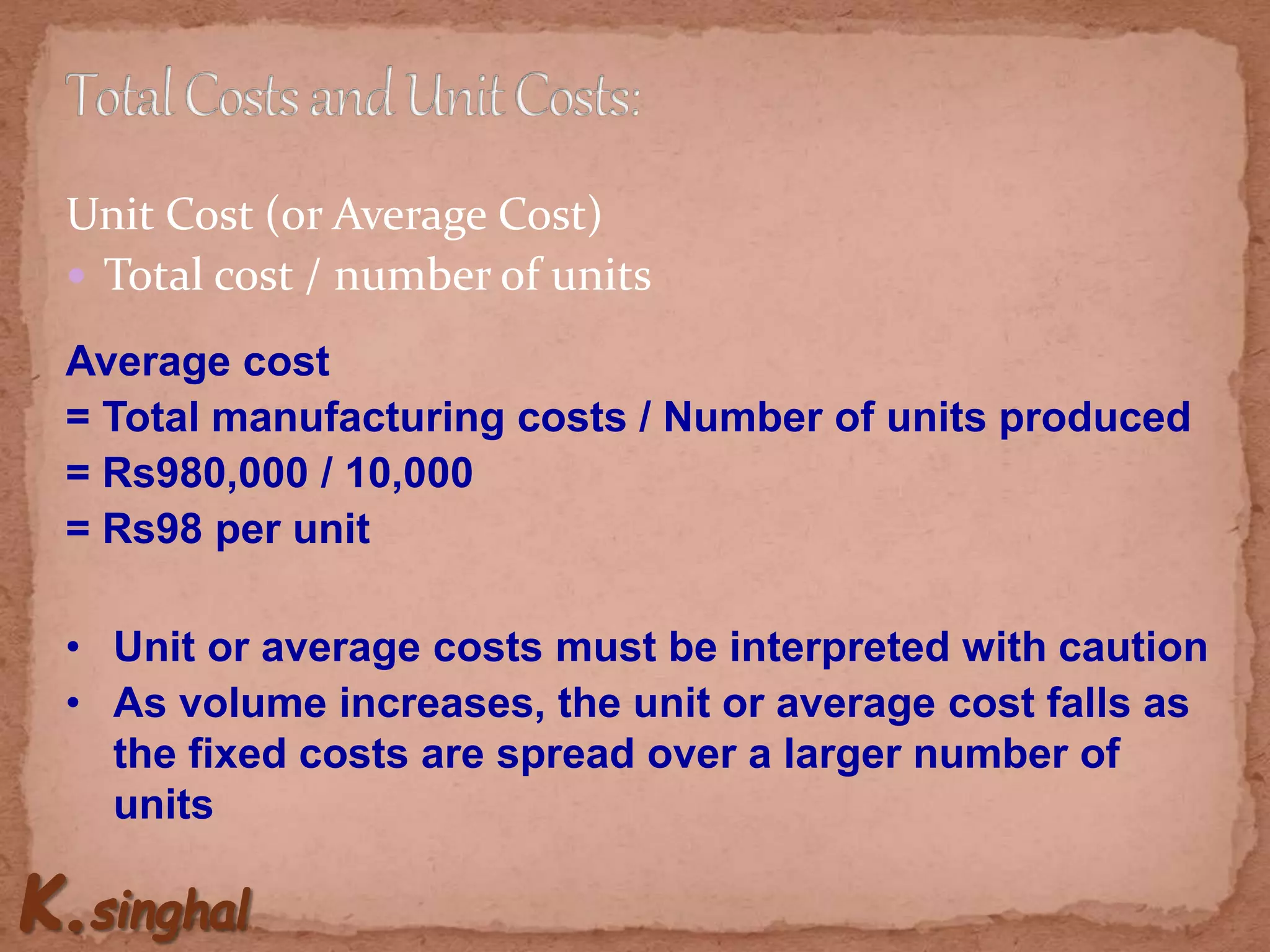

Structure and purpose of cost sheets in summarizing costs and aiding in pricing and cost control.