Downloaded 20 times

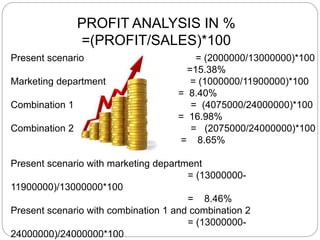

Target costing is a cost management tool used by Roller System, a manufacturer of inline skates and components, to reduce product costs over the lifecycle. The company currently produces one skate model but is developing a new "City" model for urban transportation. It defined the target costs for the new City model based on marketing's suggested sale price and margin goals. Two component combinations were analyzed to meet the target costs for a production run of 200,000 units. Combination 1 had the lowest total cost and highest profit margin of 16.98%.