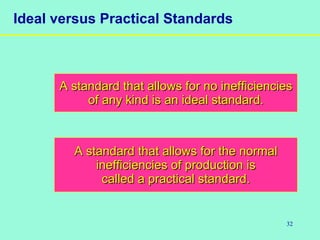

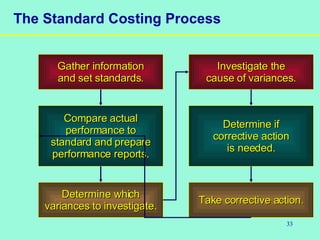

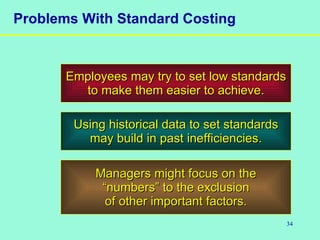

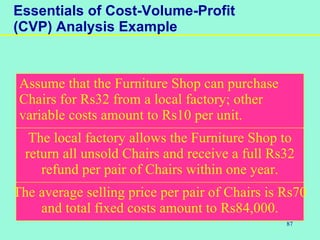

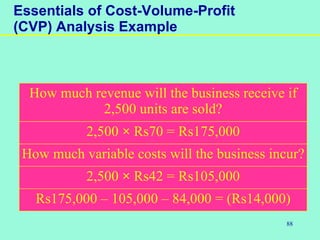

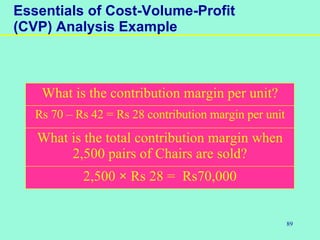

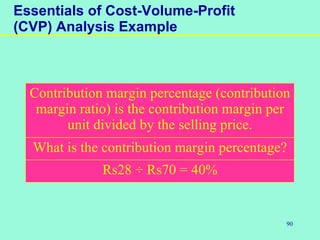

Cost accounting measures and reports on the costs of acquiring and using resources. It provides information for management and financial accounting to aid in planning and control decisions. Standard costing involves setting cost standards for materials, labor, and overhead and comparing actual costs to the standards to analyze variances and maintain efficiency. Standards can be either ideal, allowing for no inefficiencies, or practical, allowing for normal production inefficiencies. The standard costing process involves gathering information to set standards and then comparing actual performance to the standards to prepare performance reports.