Downloaded 185 times

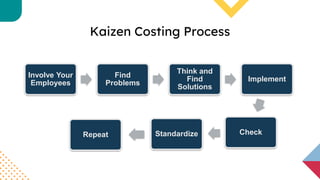

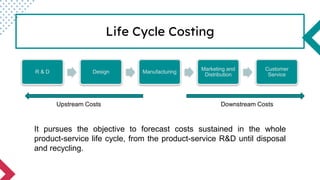

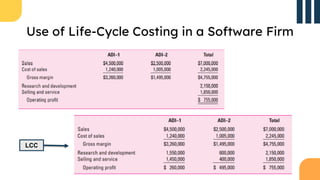

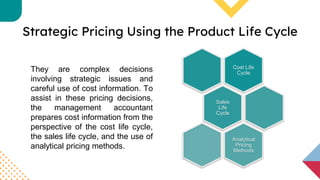

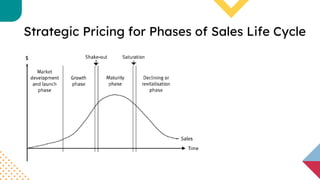

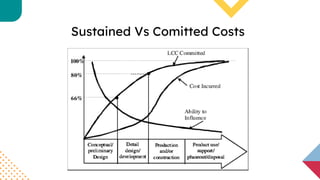

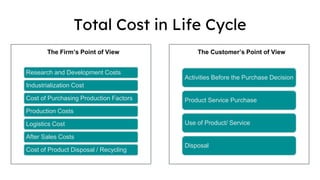

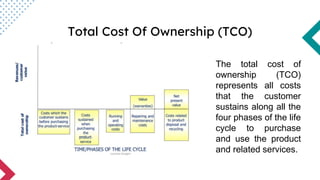

Target and Life Cycle Costing discusses target costing, kaizen costing, and life cycle costing. Target costing determines the cost needed for a product to be profitable at its selling price. Kaizen costing uses continuous improvement to maintain costs. Life cycle costing considers all costs over a product's lifetime from development to disposal. It helps companies strategically price products over their sales lifecycles and understand costs from the customer perspective through total cost of ownership analysis.