This document provides an overview of simple and multiple linear regression analysis. It discusses key concepts such as:

- Dependent and independent variables in bivariate linear regression

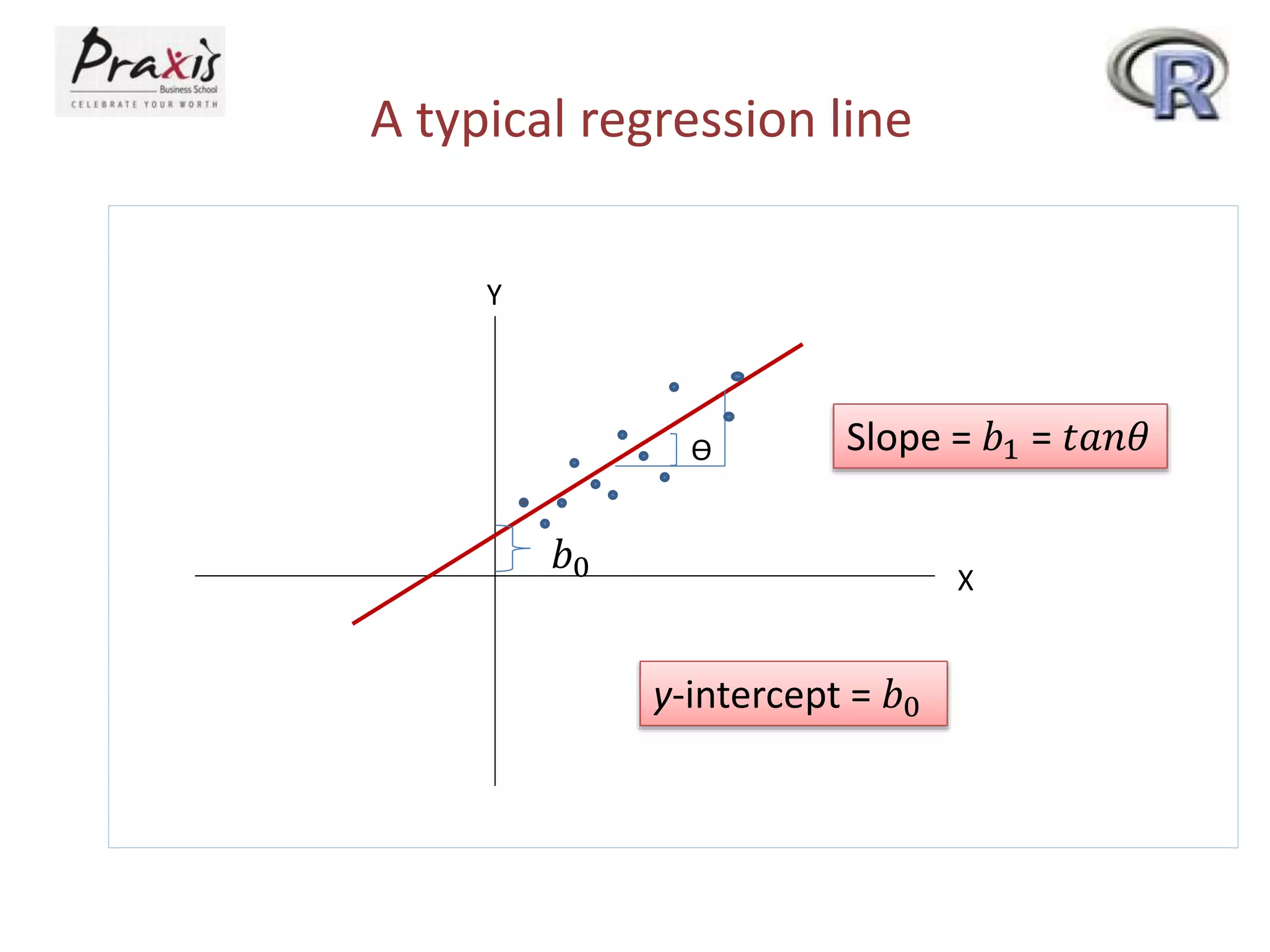

- Using scatter plots to explore relationships

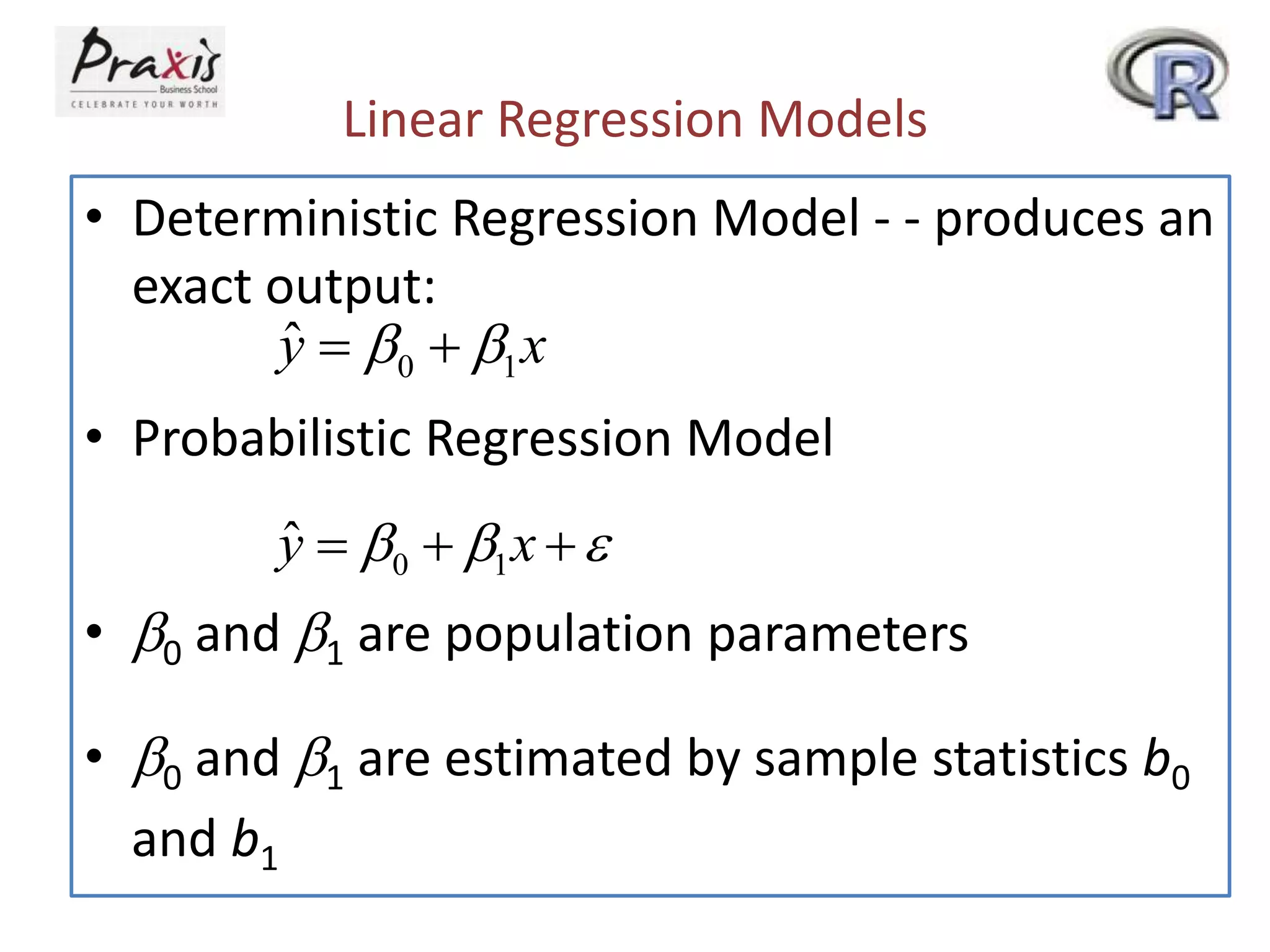

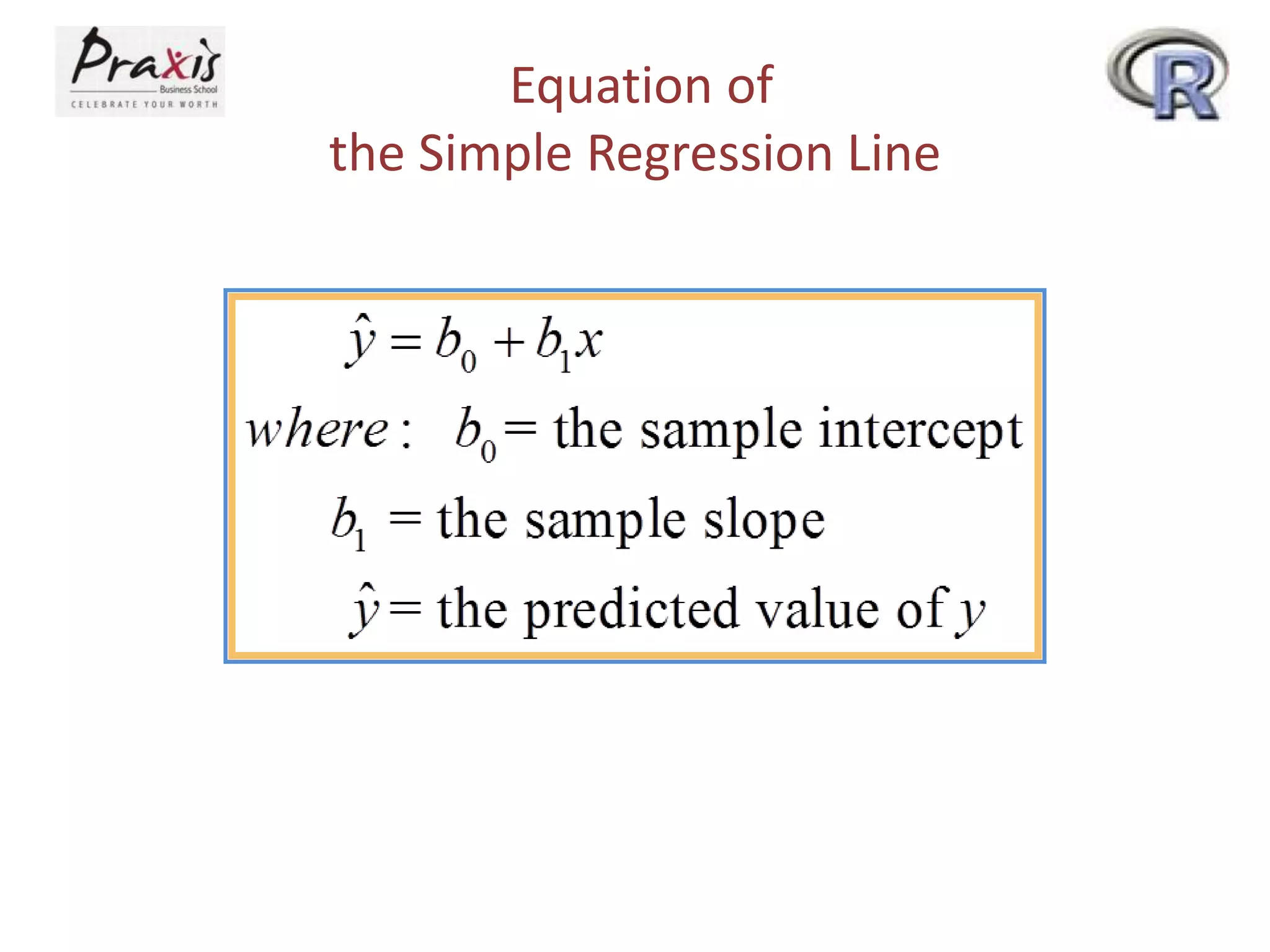

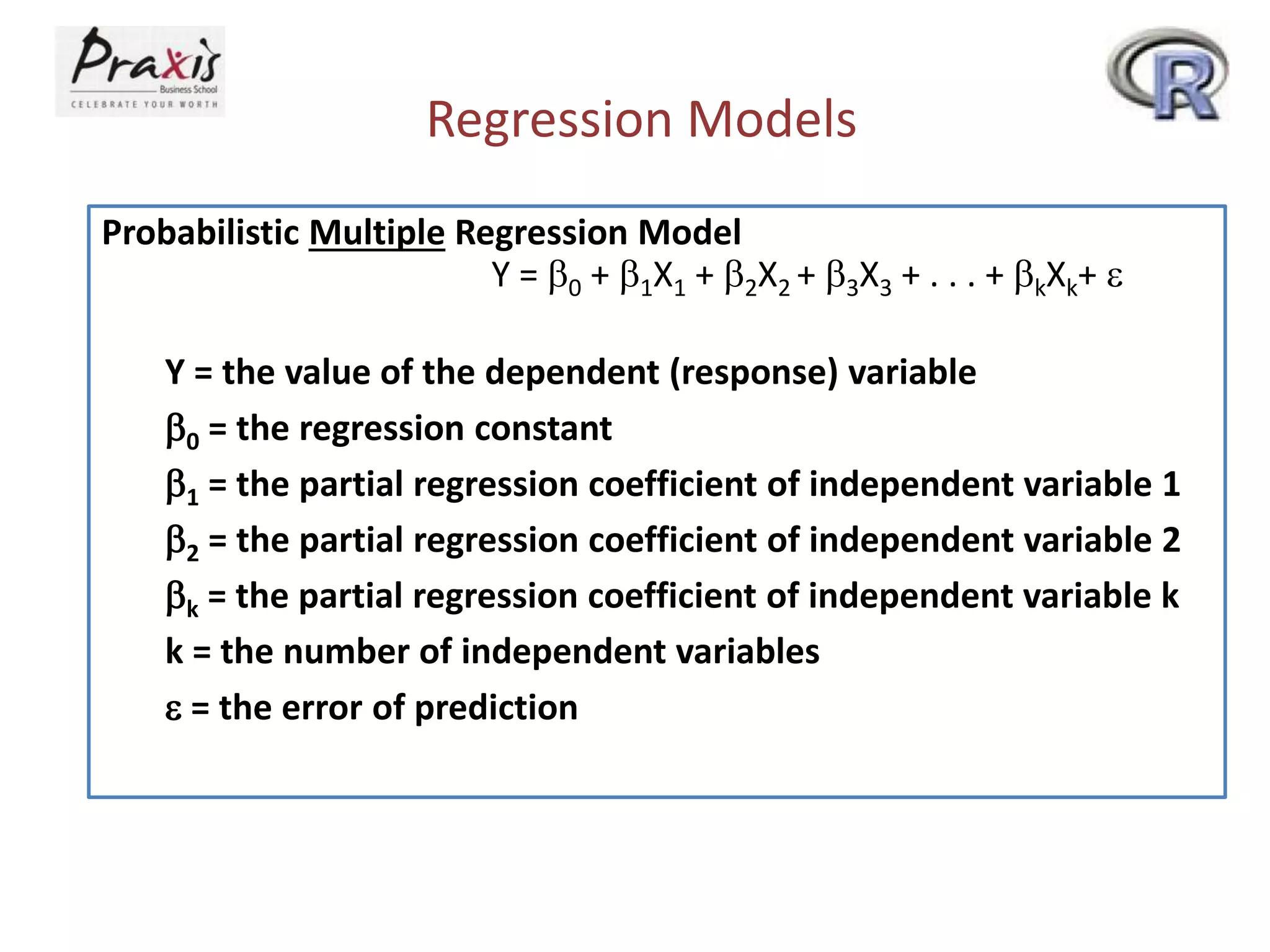

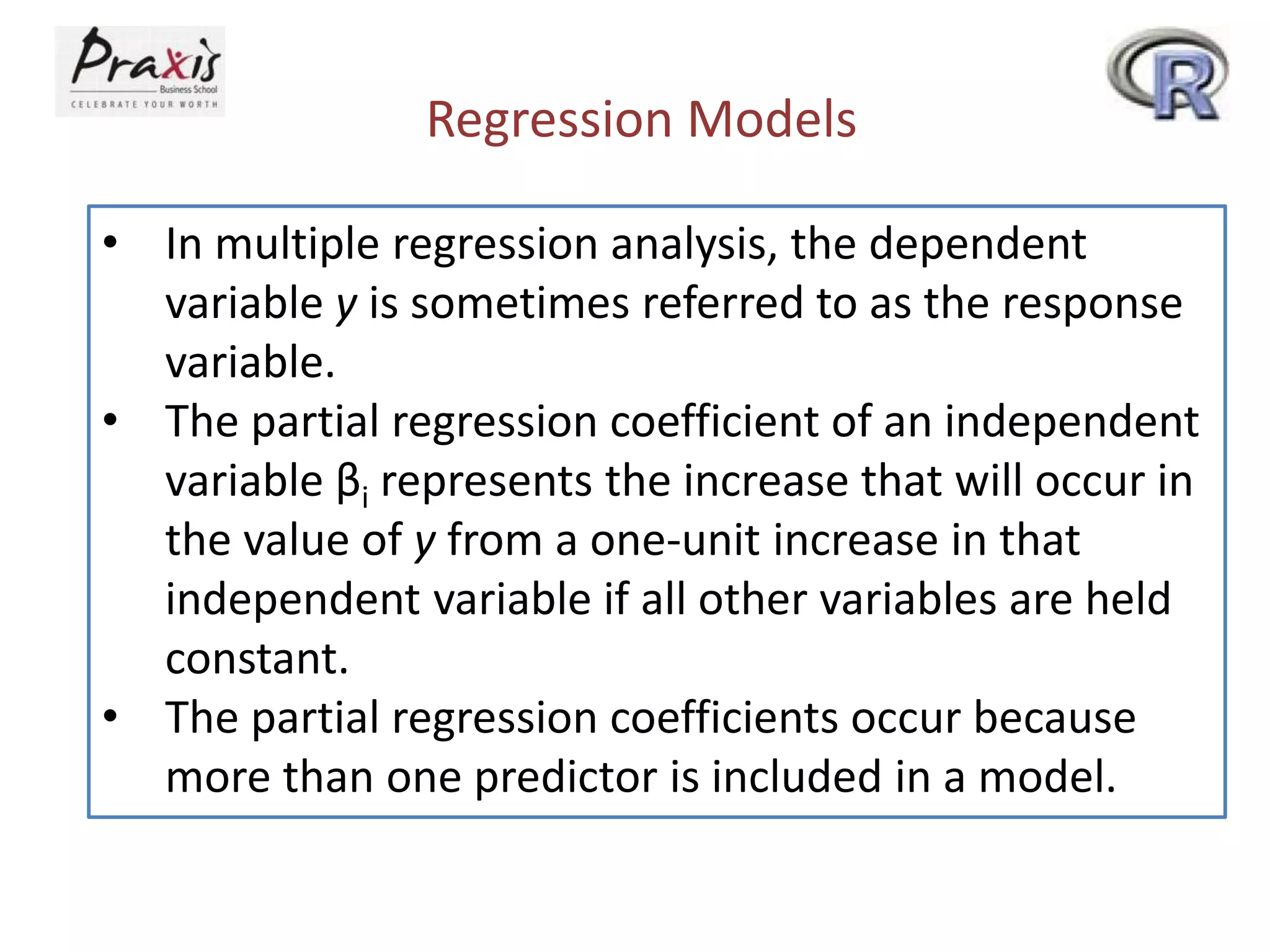

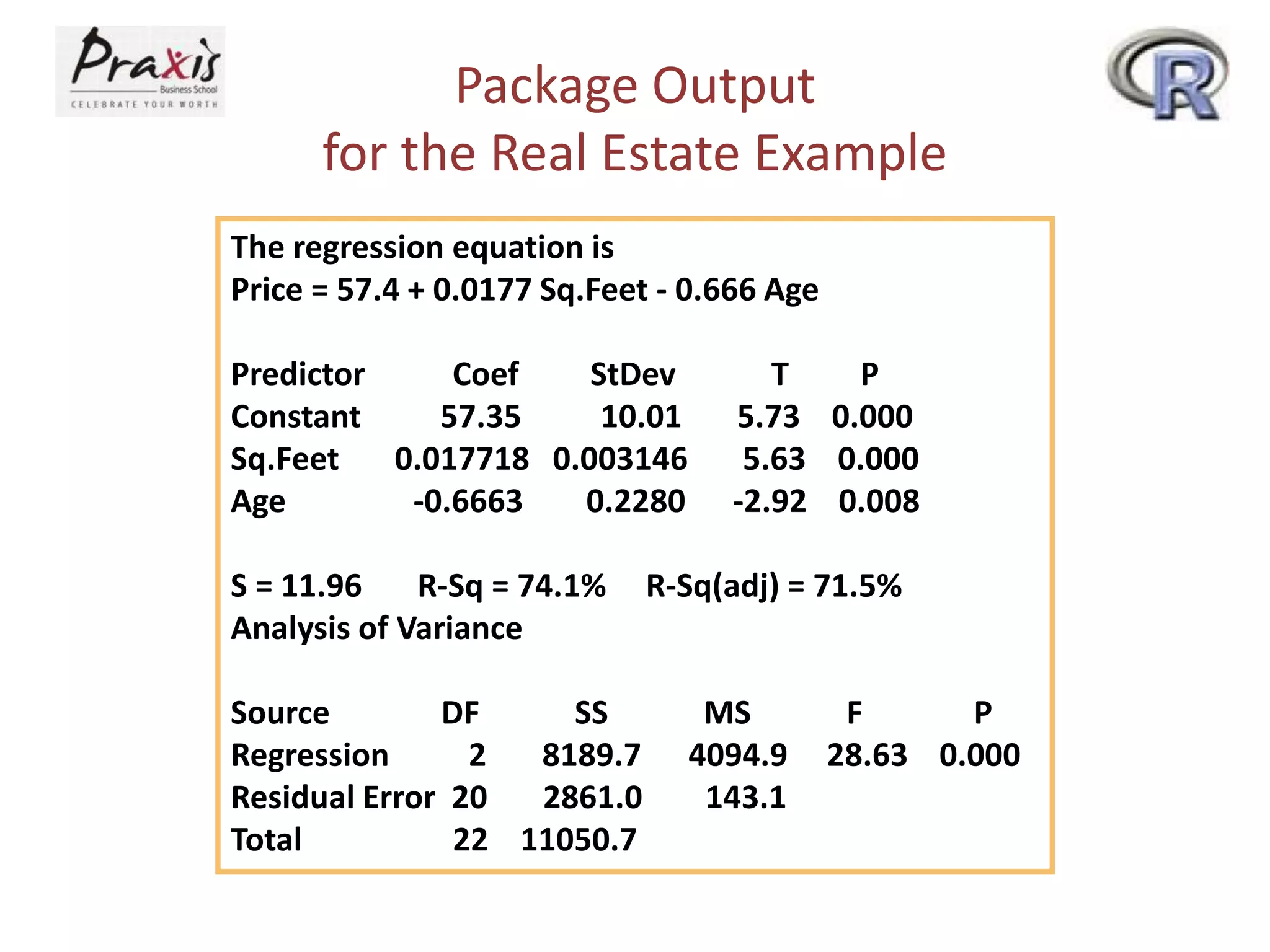

- Estimating regression coefficients and equations for simple and multiple regression models

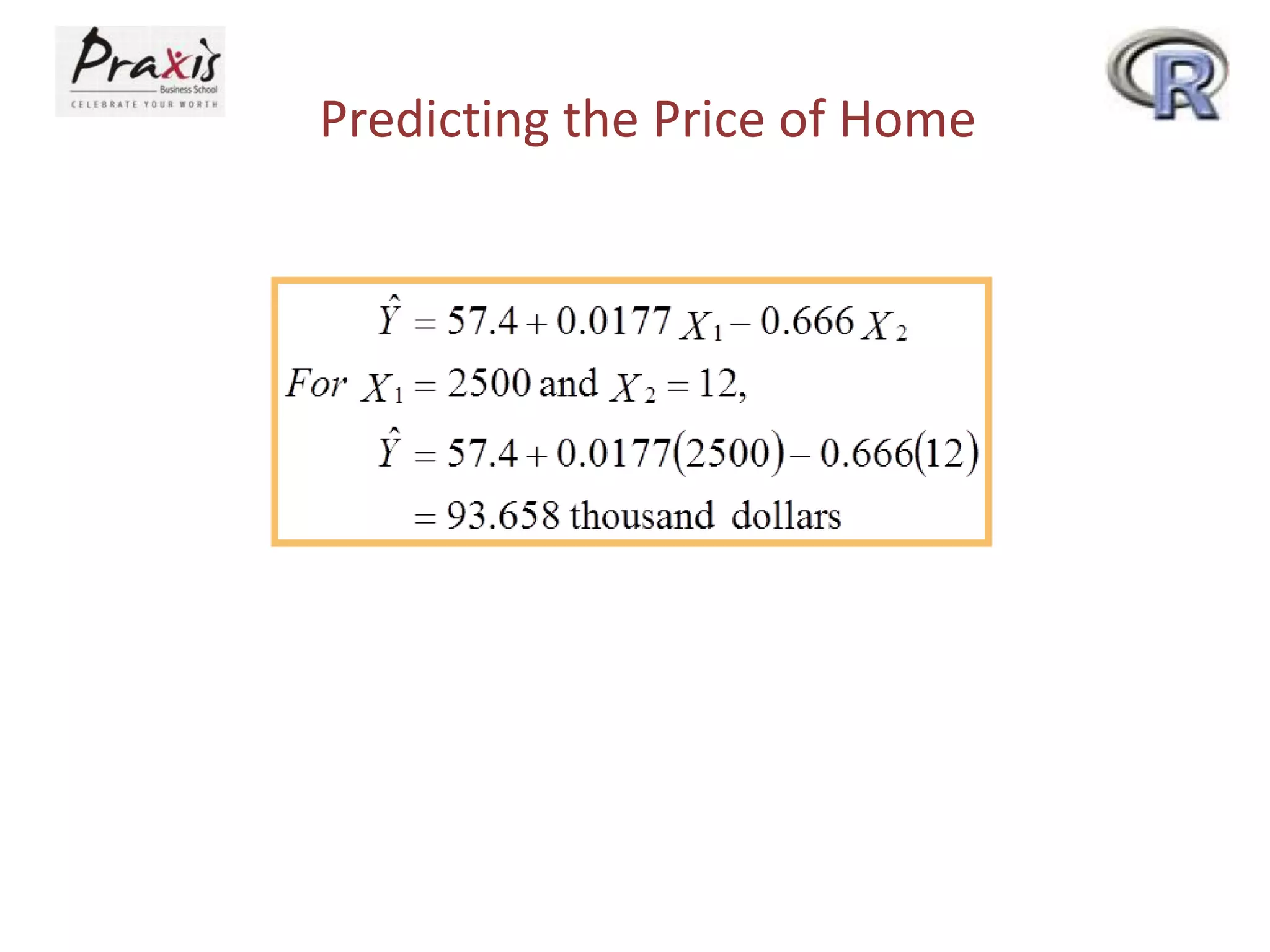

- Using regression models to predict outcomes based on independent variable values

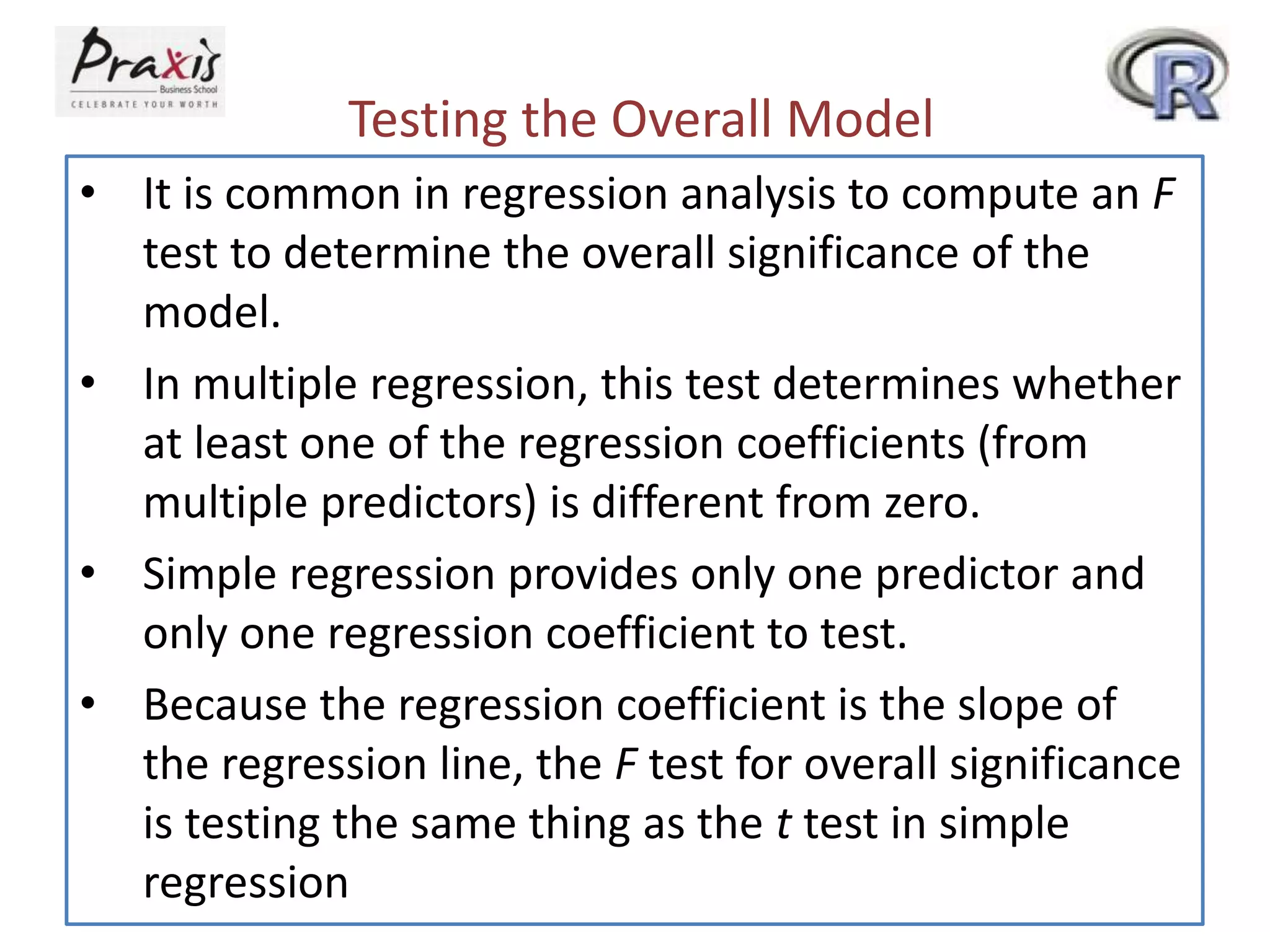

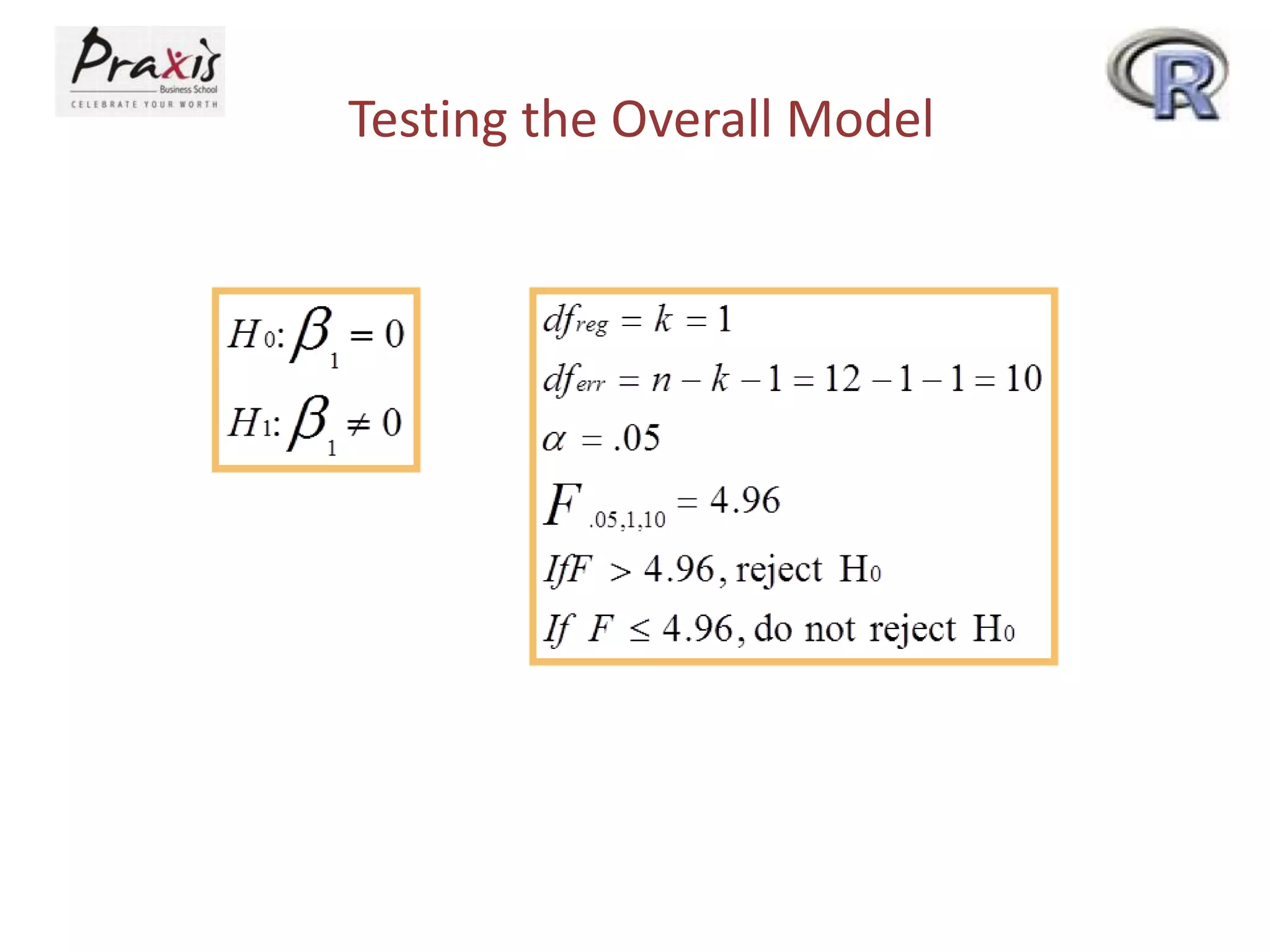

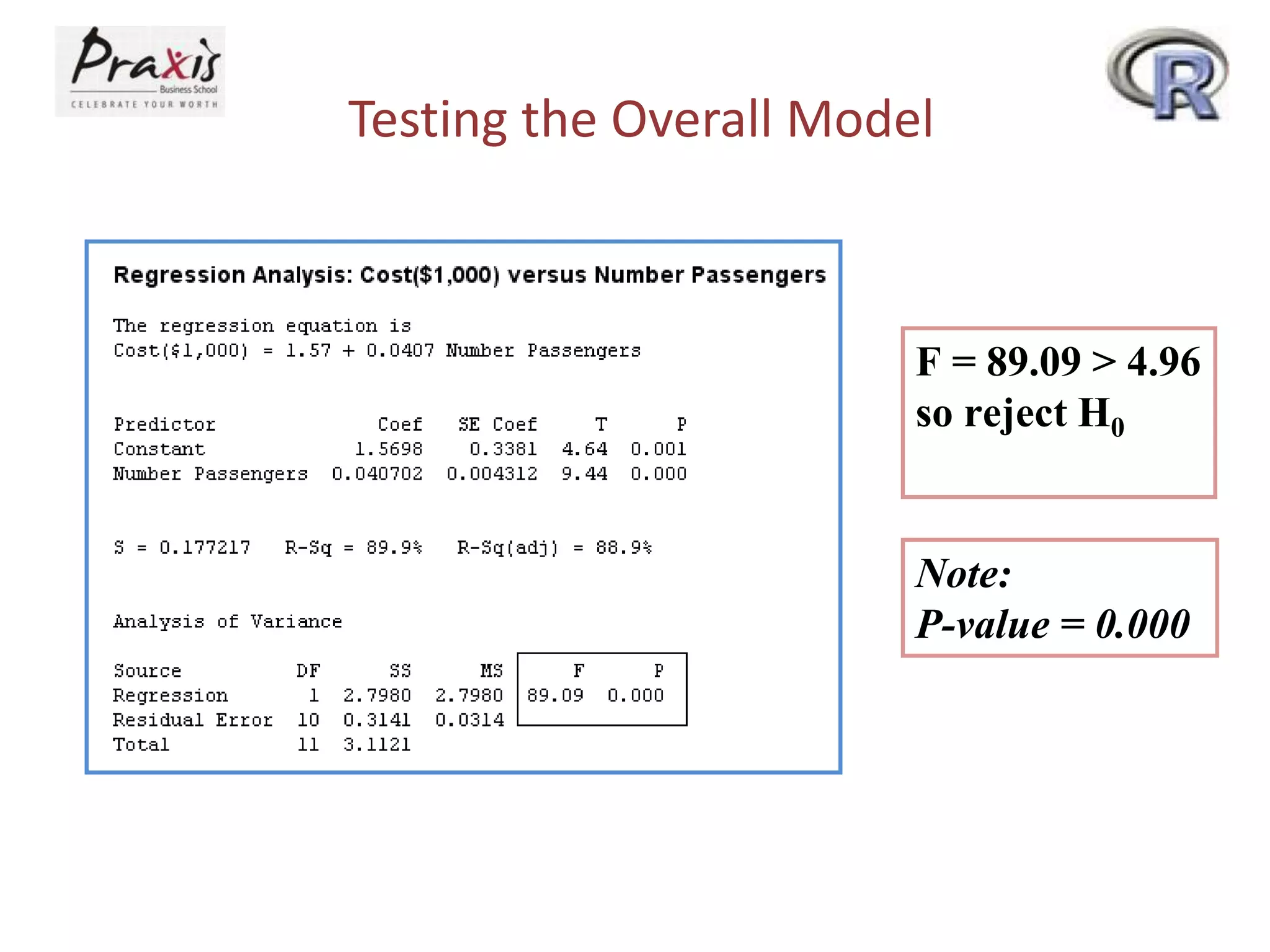

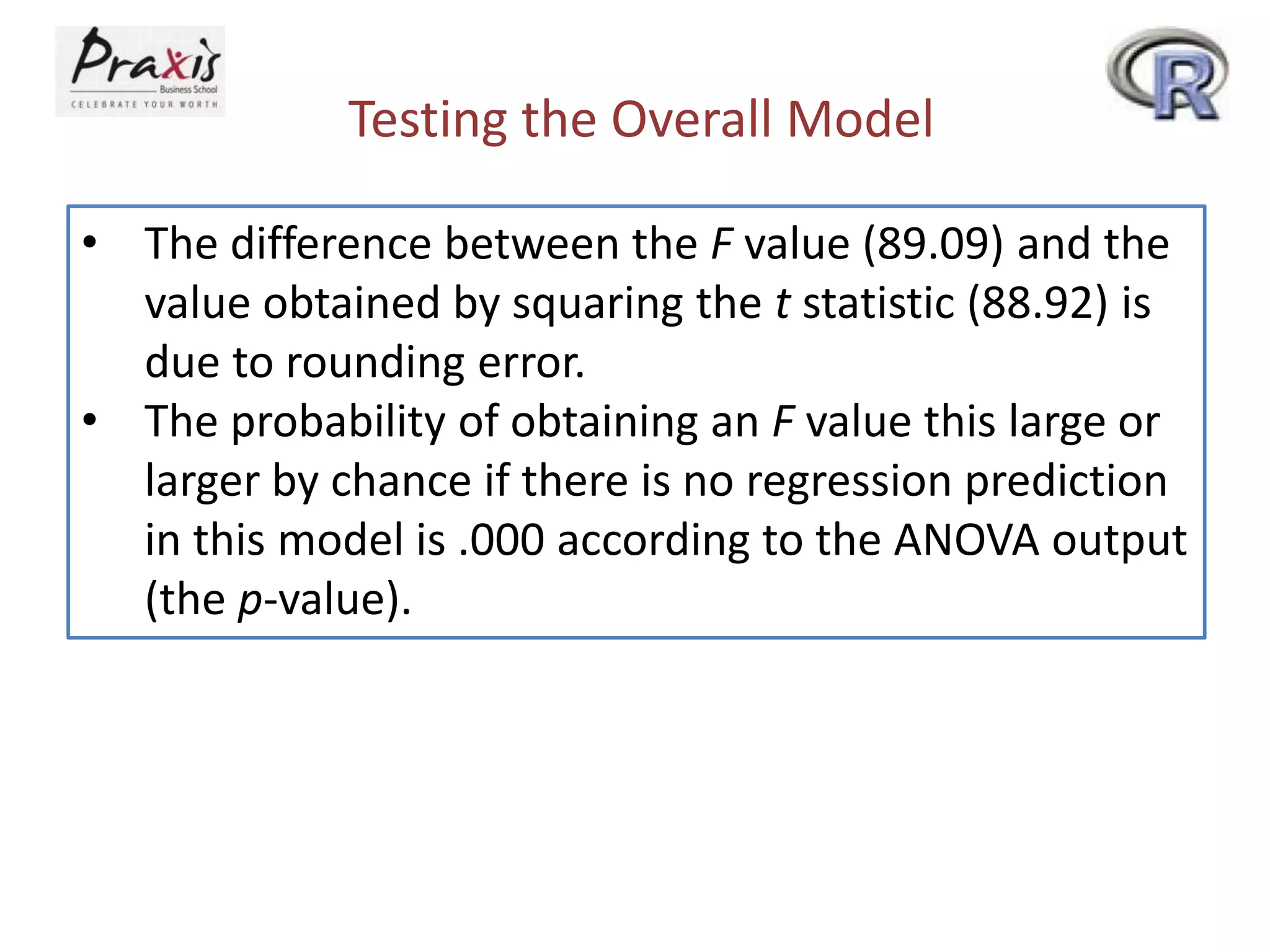

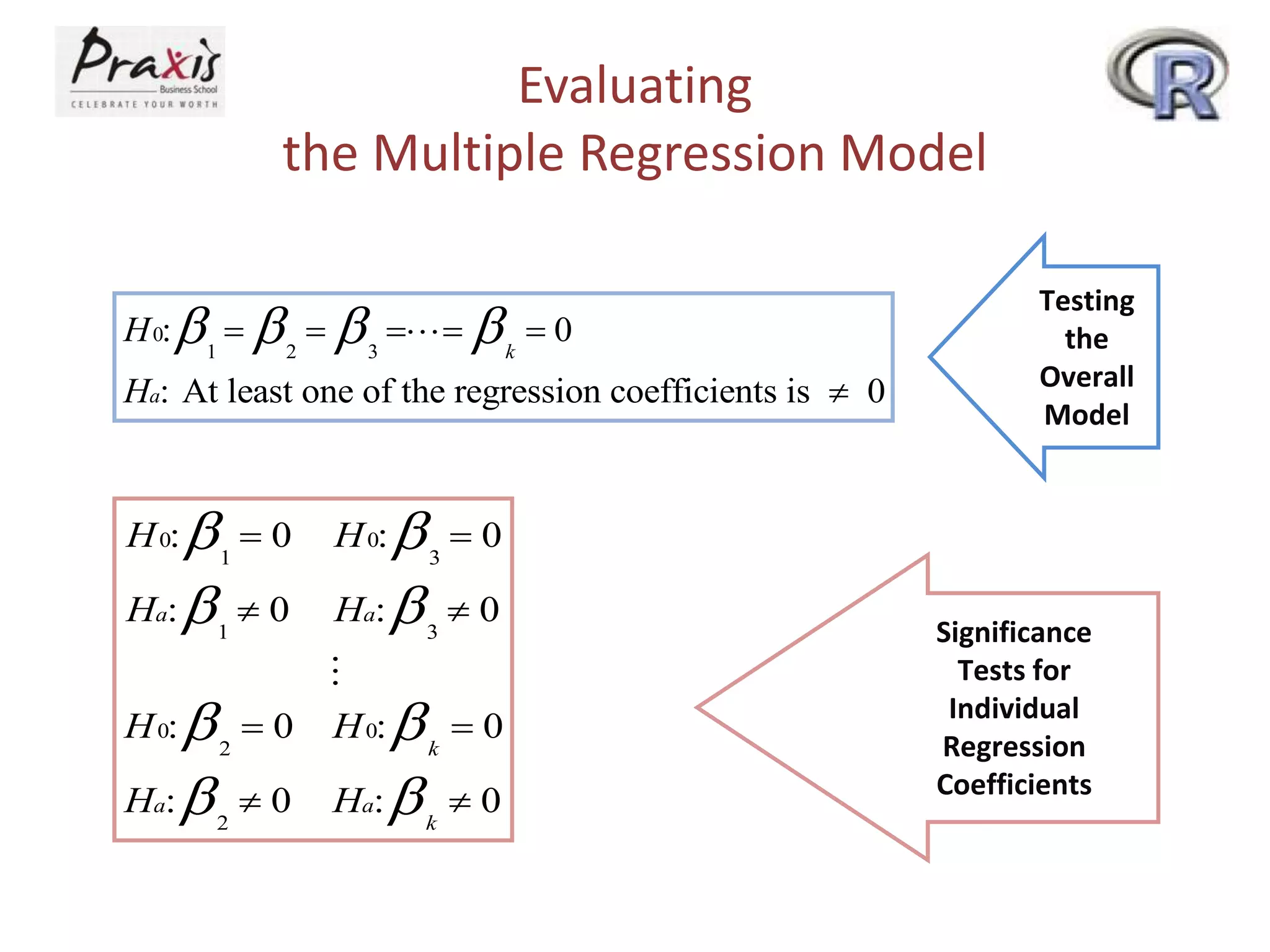

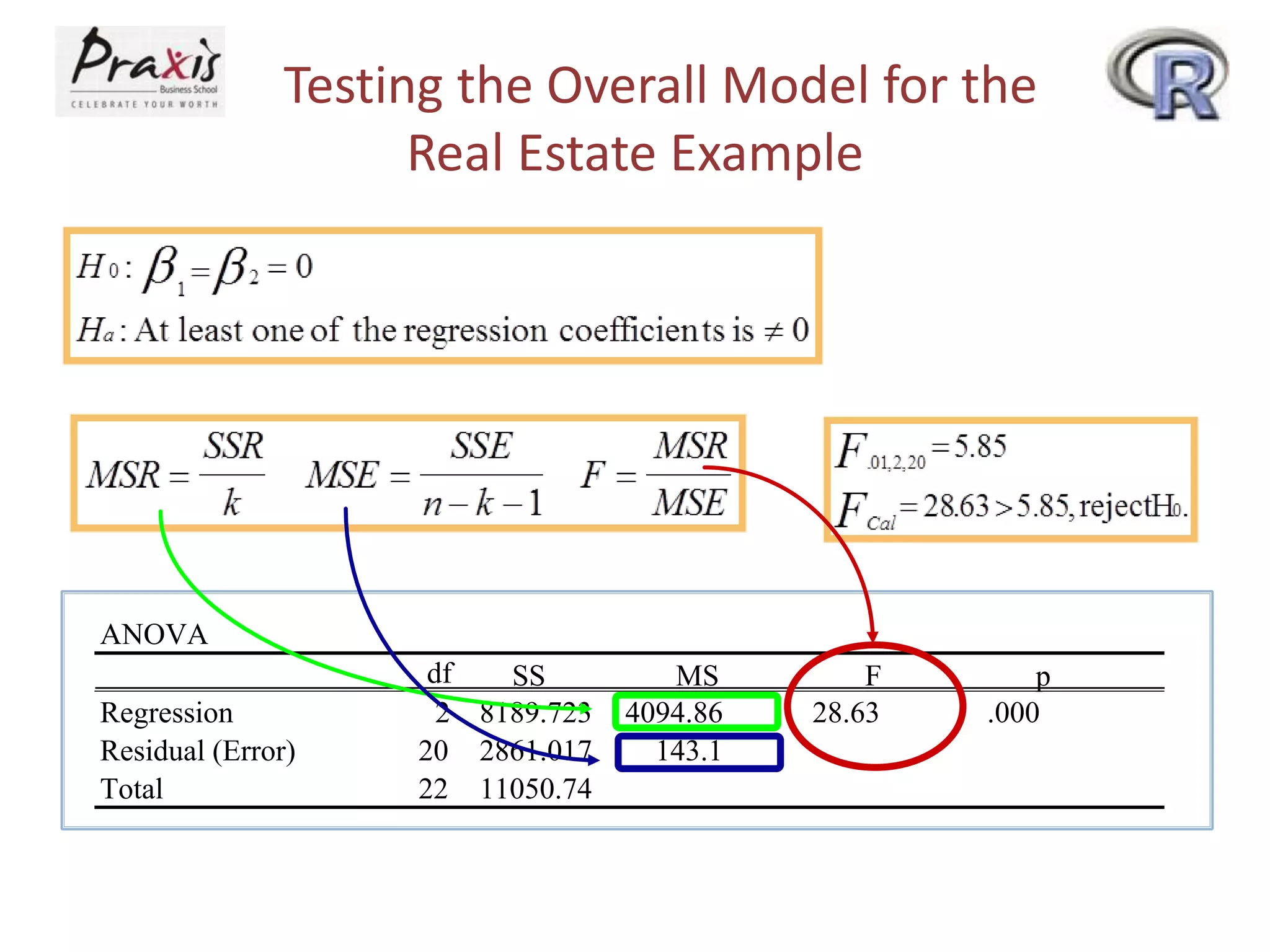

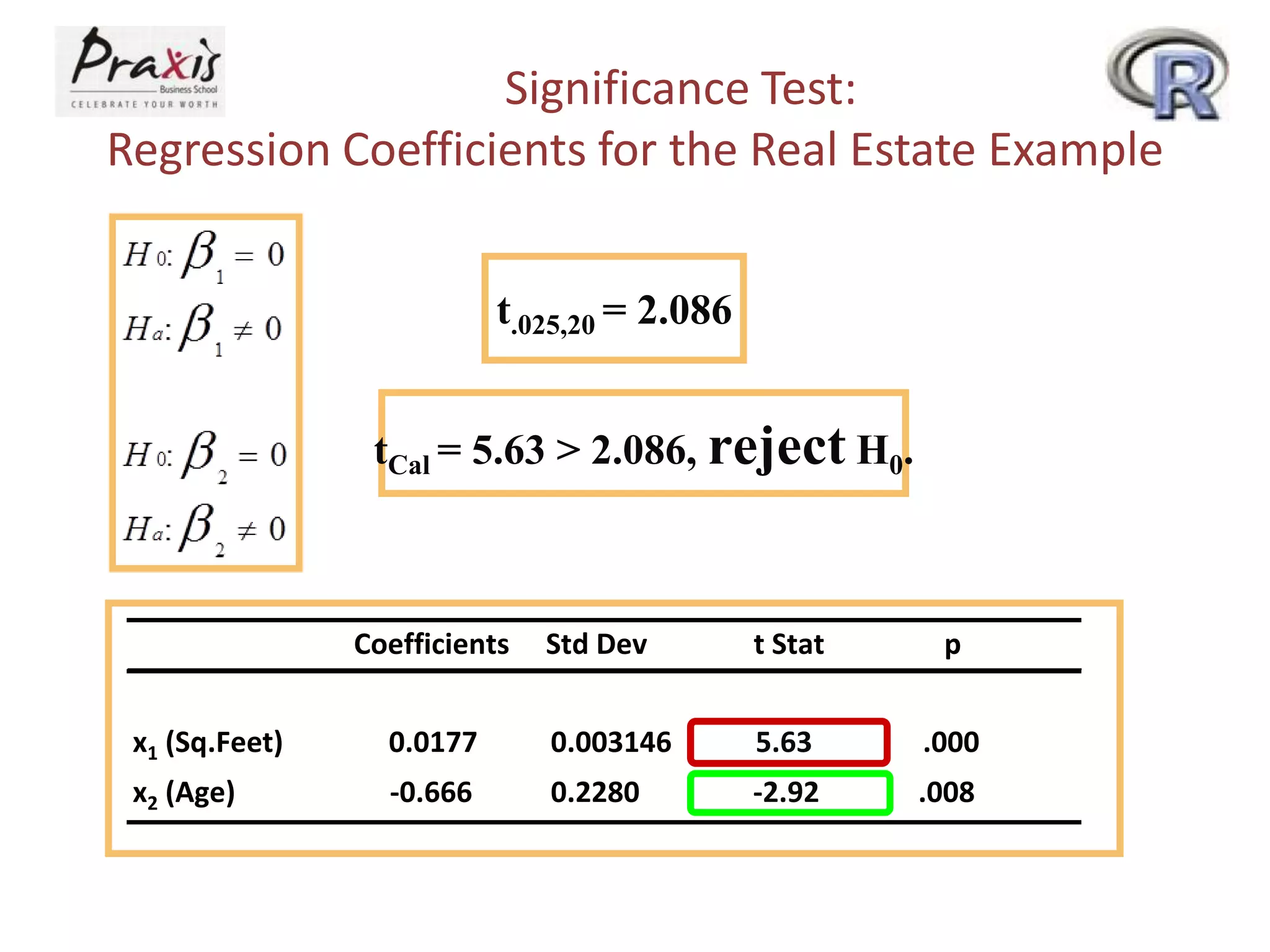

- Conducting statistical tests on overall regression models and individual coefficients