Downloaded 113 times

![16 | P a g e

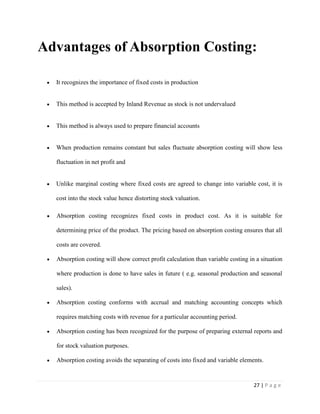

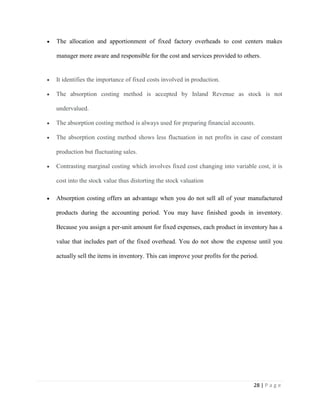

Formulas of Marginal Costing:

Marginal cost = prime cost + total variable overheads

Or

Marginal cost = total variable cost.

Contribution = selling price – variable (marginal) cost

Or Contribution = fixed cost + profit (or-loss)

Or Contribution – fixed cost = profit (or loss)

Thus,

Sales = Variable cost + fixed cost + profit (or – loss)

Sales = Variable cost = fixed cost + profit (or – loss)

P/V = contribution/sales = S/C

Or = [Fixed Costs + Profit/sales] = [F+P/S]

Or = [Sales-Variable Cost/Sales] = [S-V/S]

Break-even Point (units) = Total fixed costs/Contribution per unit [F/C per unit]](https://image.slidesharecdn.com/marginalcosting-130514041514-phpapp02/85/Marginal-costing-16-320.jpg)

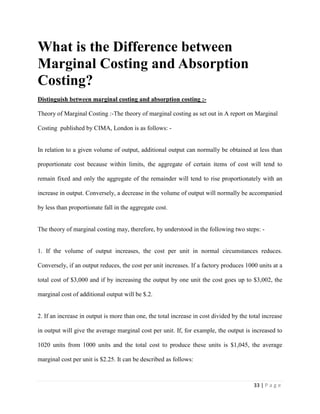

![17 | P a g e

Break-even Sales = Total Fixed Costs x selling price per unit / contribution per unit

[F/C*S]

Fixed Cost/P/V Ratio [F/P/V]](https://image.slidesharecdn.com/marginalcosting-130514041514-phpapp02/85/Marginal-costing-17-320.jpg)

Marginal costing is a technique that differentiates between fixed and variable costs. It assigns only variable costs to cost units and writes off fixed costs for the period against total contribution. Contribution is calculated as sales revenue minus variable costs. Marginal costing is useful for decision making as it shows the effect on profit of changes in volume or product mix. Key aspects include classifying costs, calculating contribution, and using contribution to determine the break-even point where total revenues equal total costs. Marginal costing provides information on product and segment profitability without needing to allocate fixed overhead costs.