Download as PDF, PPTX

![Chapter Nine -- Inflation Accounting

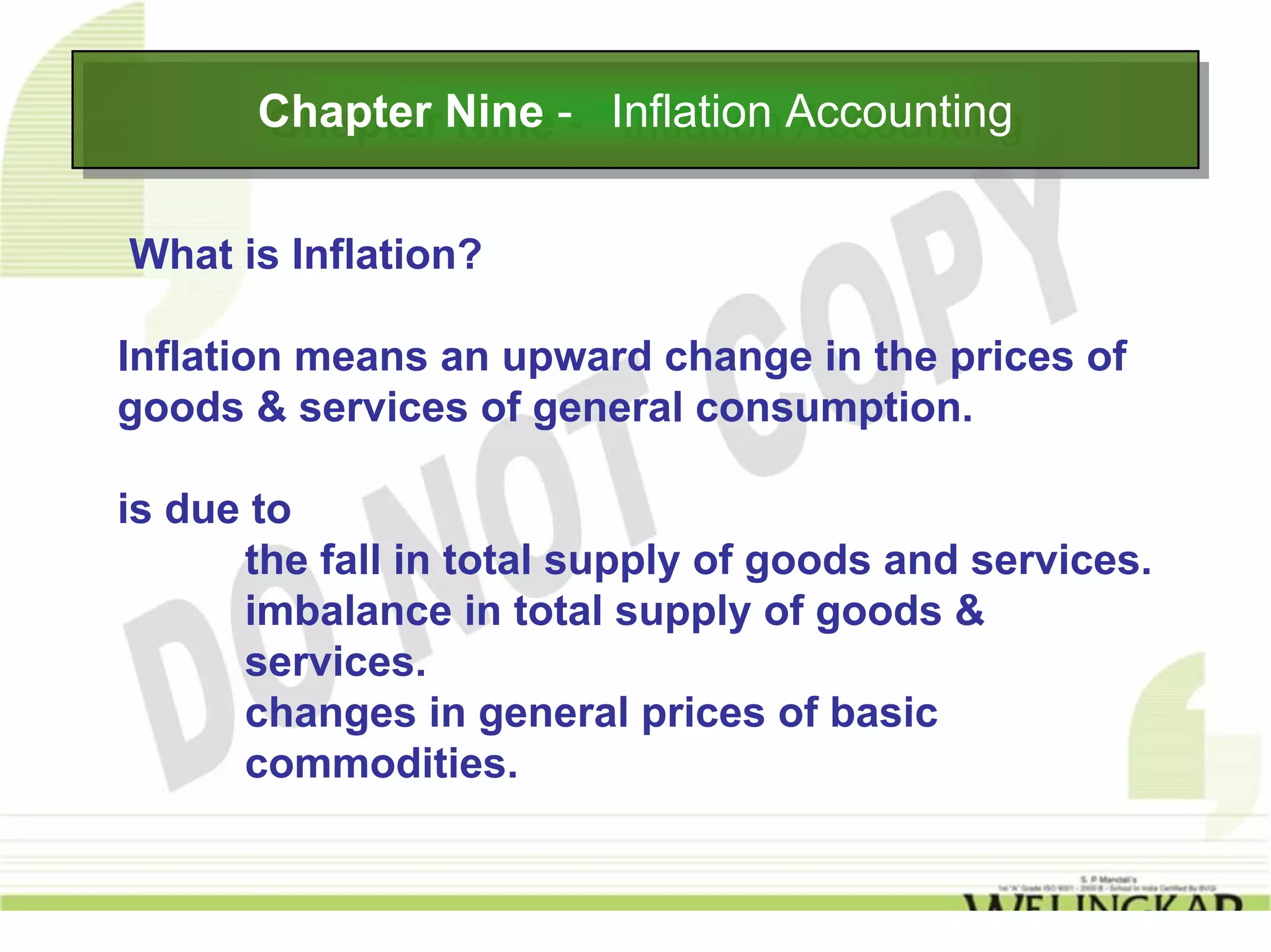

Chapter Nine Inflation Accounting

Methods of Inflation Accounting

Є Current Purchasing Power (CPP)

Є Current Value Systems

Under this method, the current value of an individual asset is

based on the present value of the future cash flows that are

expected to result from the ownership of the asset.

Such present values are calculated from

[a] the estimated cash amount of the future benefits [b] the

timing of these benefits & [c] an appropriate discount factor.](https://image.slidesharecdn.com/inflationaccounting-121220061447-phpapp01/85/Inflation-Accounting-12-320.jpg)

![Chapter Nine -- Inflation Accounting

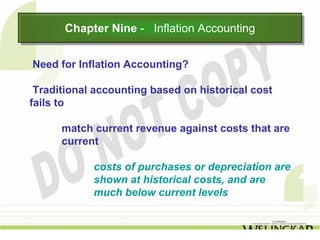

Chapter Nine Inflation Accounting

Methods of Inflation Accounting

Є Current Purchasing Power (CPP)

Є Current Value Systems

Under this method, the current value of an individual asset is

based on the present value of the future cash flows that are

expected to result from the ownership of the asset.

Such present values are calculated from

[a] the estimated cash amount of the future benefits [b] the

timing of these benefits & [c] an appropriate discount factor.

This discount factor usually equals cost of capital to the

company.](https://image.slidesharecdn.com/inflationaccounting-121220061447-phpapp01/85/Inflation-Accounting-13-320.jpg)

This document discusses inflation accounting and its need. Traditional historical cost accounting fails to accurately match current revenues and costs during inflation as historical costs are much lower than current costs. It also fails to realistically report profits. The document describes two methods of inflation accounting: current purchasing power method and current value systems method. Both methods aim to express financial statement figures in terms of their current purchasing power to provide a more accurate picture during inflationary periods.