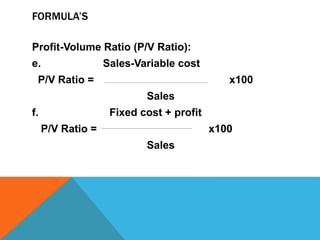

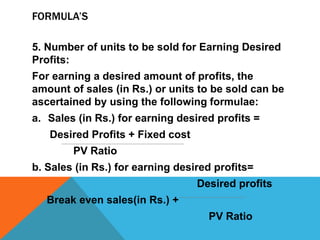

Marginal costing and absorption costing are two methods used to ascertain product costs. Marginal costing only includes variable costs in product costs, while absorption costing includes both fixed and variable costs. Key terms in marginal costing include variable costs, fixed costs, marginal costs, contribution, and break-even point. Formulas are provided to calculate metrics like profit-volume ratio, break-even point, margin of safety, and profits at different production levels using marginal cost principles. Limiting factors that can restrict growth, like material shortages or lack of capacity, are also discussed.