1. 4QFY2010 Result Update I Agri-Business

May 12, 2010

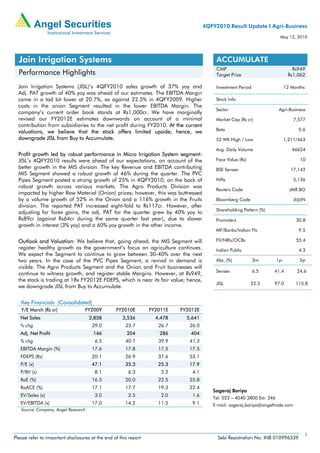

Jain Irrigation Systems ACCUMULATE

CMP Rs949

Performance Highlights Target Price Rs1,062

Jain Irrigation Systems (JISL)’s 4QFY2010 sales growth of 37% yoy and Investment Period 12 Months

Adj. PAT growth of 40% yoy was ahead of our estimates. The EBITDA Margin

came in a tad bit lower at 20.7%, as against 22.5% in 4QFY2009. Higher Stock Info

costs in the onion Segment resulted in the lower EBITDA Margin. The

Sector Agri-Business

company’s current order book stands at Rs1,000cr. We have marginally

revised our FY2012E estimates downwards on account of a minimal Market Cap (Rs cr) 7,577

contribution from subsidiaries to the net profit during FY2010. At the current

valuations, we believe that the stock offers limited upside; hence, we Beta 0.6

downgrade JISL from Buy to Accumulate. 52 WK High / Low 1,211/463

Avg. Daily Volume 46624

Profit growth led by robust performance in Micro Irrigation System segment:

JISL’s 4QFY2010 results were ahead of our expectations, on account of the Face Value (Rs) 10

better growth in the MIS division. The key Revenue and EBITDA contributing BSE Sensex 17,142

MIS Segment showed a robust growth of 46% during the quarter. The PVC

Pipes Segment posted a strong growth of 25% in 4QFY2010, on the back of Nifty 5,136

robust growth across various markets. The Agro Products Division was

Reuters Code JAIR.BO

impacted by higher Raw Material (Onion) prices; however, this was buttressed

by a volume growth of 52% in the Onion and a 116% growth in the Fruits Bloomberg Code JI@IN

division. The reported PAT increased eight-fold to Rs117cr. However, after

Shareholding Pattern (%)

adjusting for forex gains, the adj. PAT for the quarter grew by 40% yoy to

Rs89cr (against Rs64cr during the same quarter last year), due to slower Promoters 30.8

growth in interest (3% yoy) and a 60% yoy growth in the other income.

MF/Banks/Indian FIs 9.5

Outlook and Valuation: We believe that, going ahead, the MIS Segment will FII/NRIs/OCBs 55.4

register healthy growth as the government’s focus on agriculture continues. Indian Public 4.3

We expect the Segment to continue to grow between 30-40% over the next

two years. In the case of the PVC Pipes Segment, a revival in demand is Abs. (%) 3m 1yr 3yr

visible. The Agro Products Segment and the Onion and Fruit businesses will

Sensex 6.5 41.4 24.6

continue to witness growth, and register stable Margins. However, at Rs949,

the stock is trading at 18x FY2012E FDEPS, which is near its fair value; hence,

JISL 22.5 97.0 115.8

we downgrade JISL from Buy to Accumulate.

Key Financials (Consolidated)

Y/E March (Rs cr) FY2009 FY2010E FY2011E FY2012E

Net Sales 2,858 3,536 4,478 5,641

% chg 29.0 23.7 26.7 26.0

Adj. Net Profit 146 204 286 404

% chg 6.5 40.1 39.9 41.3

EBITDA Margin (%) 17.6 17.8 17.5 17.5

FDEPS (Rs) 20.1 26.9 37.6 53.1

P/E (x) 47.1 35.3 25.3 17.9

P/BV (x) 8.1 6.3 5.2 4.1

RoE (%) 16.5 20.0 22.5 25.8

RoACE (%) 17.1 17.7 19.3 22.4

Sageraj Bariya

EV/Sales (x) 3.0 2.5 2.0 1.6

Tel: 022 – 4040 3800 Ext: 346

EV/EBITDA (x) 17.0 14.2 11.5 9.1 E-mail: sageraj.bariya@angeltrade.com

Source: Company, Angel Research

1

Please refer to important disclosures at the end of this report Sebi Registration No: INB 010996539

2. Jain Irrigations Systems I 4QFY2010 Result Update

Exhibit 1: Key Financial (Standalone)

Y/E March (Rs cr) 4QFY2010 4QFY2009 % chg FY2010 FY2009 % chg

Total Revenue 959 699 37.2 2735 2188 25.0

Total RM 575 408 1585 1288

as % of sales 60.0 58.5 58.0 58.9

Gross Profit 383 290 32.1 1150 900 27.8

Gross margin (%) 40.0 41.5 42.0 41.1

Staff cost 31 26 16.9 104 81 29.0

as % of sales 3.2 3.7 3.8 3.7

Other Expenses 154 107 44.3 469 357 31.3

as % of sales 16.1 15.3 17.1 16.3

Total Exp 760 542 40.4 2159 1726 25.1

as % of sales 79.3 77.5 78.9 78.9

EBITDA 198 157 26.2 576 462 24.8

EBITDA % 20.7 22.5 21.1 21.1

Depreciation 18 14 24.3 66 48 37.9

EBIT 180 143 26.4 511 414 23.3

EBIT % 18.8 20.4 18.7 18.9

Other Income 5 3 59.8 5 3 55.6

Interest 50 49 2.7 189 156 21.0

PBT 135 97 39.5 327 261 25.1

Extra-ord Items -34 21 -71 78

PBT 169 76 121.9 398 184 116.7

Total tax 52 63 125 64

tax rate 38 65 38 24

PAT 117 13 785.6 273 120 127.2

PAT (%) 12.2 1.9 10.0 5.5

Adj PAT 89 64 39.5 216 173 25.1

adj PAT (%) 9.3 9.2 7.9 7.9

Equity 76.0 72.4 76.0 72.4

Adj EPS 11.7 8.8 32.8 28.8 23.9 19.1

Source: Company, Angel Research

Key highlights of FY2010 (Standalone)

• The total revenue increased by 25% on the back of strong growth registered in

key divisions like MIS (37%), PVC pipes (27%) and Fruits (30%).

• The company was able to maintain its EBITDA margin, due to a high

contribution from the rich margin MIS division and low volatility in key raw

material prices.

• The Total Adj. PAT grew by 25.1%, to Rs216cr from Rs173cr in FY2009.

May 12, 2010 2

3. Jain Irrigations Systems I 4QFY2010 Result Update

Exhibit 2: Segmental Performance (Standalone)

Divisional performance 4Q FY10 4Q FY09 % chg FY2010 FY2009 % chg

(yoy) (yoy)

Revenue (Rs cr)

MIS 478 328 45.7 1302 952 36.8

PVC pipes 160 128 25.2 525 414 27.1

PE Pipes 104 93 11.7 317 334 (5.1)

PVC Sheet 42 28 47.9 116 117 (0.6)

PC sheets - 15 - 37 56 (34.8)

Onions 66 48 36.8 146 133 9.7

Fruit 104 60 73.8 285 218 30.3

Total 954 700 36.3 2728 2223 22.7

EBITDA (Rs cr)

MIS 154 106 45.4 410 283 44.8

PVC pipes 14 11 23.0 45 32 39.5

PE Pipes 13 12 12.8 39 42 (8.1)

PVC Sheet 3 5 (27.7) 13 16 (20.9)

PC sheets - 2 - 3 6 (49.2)

Onions 1 10 (87.0) 15 36 (58.0)

Fruit 15 11 35.1 57 43 32.2

Total 201 157 28.6 581 458 26.8

EBITDA (%)

MIS 32.3 32.4 - 31.5 29.8 -

PVC pipes 8.7 8.8 - 8.5 7.7 -

PE Pipes 12.7 12.6 - 12.2 12.6 -

PVC Sheet 8.1 16.5 - 10.8 13.6 -

PC sheets - 10.3 - 8.7 11.2 -

Onions 2.0 20.7 - 10.4 27.1 -

Fruit 14.4 18.5 - 19.9 19.6 -

Total 21.1 22.4 - 21.3 20.6 -

Source: Company, Angel Research

Key segmental highlights of FY2010 (Standalone)

• The MIS division maintained its dominance and momentum by growing at

37% for the year. It also increased its contribution to total EBITDA from 62%

in FY2009 to 71% in FY2010, on the back of higher margins, which came in

at 31.5% (29.8%).

• The Fruits sub-division (of agro) was the second-best performer, growing at

30% and contributing 10% to the total EBITDA (against 9% last year).

• The PVC division grew by 27% and increased its contribution to the total

EBITDA by 100bp to 8% in FY2010.

• The Onion Division’s performance was muted, due to higher raw material

prices (supply crunch, on account of drought)

May 12, 2010 3

4. Jain Irrigations Systems I 4QFY2010 Result Update

Quarterly performance

Exhibit 3: Standalone Revenue mix (%)

4QFY2009 4QFY2010

9

11

2 7

0 7

4

47 4

13 11 50

18 17

MIS PVC pipes PE Pipes PVC Sheet

MIS PVC pipes PE Pipes PVC Sheet

PC sheets Onions Fruit

PC sheets Onions Fruit

Source - Company, Angel Research

Changes in Revenue-mix continue: The revenue contribution from the high-Margin

MIS segment increased by 300bp to 50% (47%) in 4QFY2010. Contribution from

the PVC and PE Pipes Segments, however, dropped by 100bp and 200bp, to 17%

(18%) and 11% (13%), respectively.

Robust growth in MIS Segment: JISL’s key revenue and EBITDA contributing segment,

MIS, posted one of its fastest growths in the past five quarters. The company’s MIS

business grew by 46% yoy for 4QFY2010, and increased its contribution to 50% of

sales (47% in 3QFY2010 and 2QFY2010, and 45% in 1QFY2010). Himachal

Pradesh and Punjab were the fastest growing states for the company, and grew by

2.7x and 1.4x, respectively. The other key states that contributed to the growth were,

Gujarat (grew by 92%), Tamil Nadu (grew by 77%), Rajasthan (grew by 79%), and

Maharashtra (grew by 75%). The EBITDA Margin for the Segment during the quarter

remained steady at 32%.

Exhibit 4: MIS sales growth picks-up

100

87 85

80

60

% YoY

46

39 38

36

40 33

27

20

0

1QFY2009 2QFY2009 3QFY2009 4QFY2009 1QFY2010 2QFY2010 3QFY2010 4QFY2010

Source - Company, Angel Research

May 12, 2010 4

5. Jain Irrigations Systems I 4QFY2010 Result Update

Diversification of market helps PVC Pipes Segment: For the quarter, the Segment

grew by 25% yoy to Rs160cr, led by robust growth across the market. The key

Northern market posted a growth of 82%. The other key market that witnessed good

growth was Karnataka (54%), Tamil Nadu (41%) and Gujarat (39%). The EBITDA

Margin of the Segment remained steady at 8.8%.

Exhibit 5: PVC pipe sales’ trend

18

16

16 14 15

14 14 14

14

12

10

Rs cr

8 7

6

4

2

0

1QFY2009 2QFY2009 3QFY2009 4QFY2009 1QFY2010 2QFY2010 3QFY2010

Source - Company, Angel Research

PE Pipes Segment rebounds: After breaking the declining Sales trend in 2QFY2010,

the Segment continued on the growth path, driven by strong demand from the gas

segment (growth of 141%). The segment’s sales for 4QFY2010 grew by 12% to

Rs104cr, while the EBITDA Margin remained steady at 12.7%.

Exhibit 6: PE Pipes’ sales trend: on the rebound

110

104

93

95

85

Rs cr

80

72

65

56

50

4QFY2009 1QFY2010 2QFY2010 3QFY2010 4QFY2010

Source - Company, Angel Research

May 12, 2010 5

6. Jain Irrigations Systems I 4QFY2010 Result Update

Agro Products (onions and fruit puree): The Total Revenues of the Segment grew by

57%. The revenues of the Onion Segment increased by 37% to Rs66cr, while the

Total Volume grew 52% for the quarter. The Onion Segment continued to record

one of the lowest EBITDA Margins of 2%, due to higher raw material prices. The Fruit

Puree Segment witnessed a stupendous growth of 74% yoy to Rs104cr, while the

total volume grew by 116%, due to higher off take from key customers like Coke

(grew by 2.8x). The Division’s sequential decline in the EBITDA Margin continued,

which came in at 14%, due to a higher contribution from Totapuri mangoes

(realisation of Totapuri mangoes are lower than that of Alphonso mangoes).

Exhibit 7: Onion business-all time low EBITDA margins Exhibit 8: Fruit segment - strong uptick in demand

70 28 30 110 26 28

25

56 22 24 90

21 19 19 21

42 18 70 14

Rs cr

14

Rs cr

%

%

28 12 50

7

14 6 30

2 2

10 0

0 0

4QFY2009 1QFY2010 2QFY2010 3QFY2010 4QFY2010

4QFY2009 1QFY2010 2QFY2010 3QFY2010 4QFY2010

Sales EBITDA (%) Sales EBITDA (%)

Source - Company , Angel Research Source - Company , Angel Research

May 12, 2010 6

7. Jain Irrigations Systems I 4QFY2010 Result Update

Outlook and Valuation

Going ahead, we believe that the MIS Segment will continue to witness healthy

growth, as the Central government focuses on increasing farm output to tackle the

long-term food security issue, along with increasing the farmers’ income. We expect

the Segment to continue to grow between 30-40% over the next two years. In the

case of the PE Pipes Segment, a revival in demand is visible. The Agro Products

Segment (comprising of the Onion and Fruit businesses) will continue to witness

growth and register stable Margins.

We have marginally revised our FY2012E estimates downwards on account of a

minimal contribution from subsidiaries to the net profit during FY2010.

Exhibit 9: Segmental Performance (Consolidated)

Rs crore Old New % chg

FY2011 FY2012 FY2011 FY2012 FY2011 FY2012

Sales 4120 4930 4478 5641 8.7 14.4

EBITDA 721 858 784 987 8.7 15.1

EBITDA % 17.5 17.4 17.5 17.5

PAT 306 403 286 404 (6.7) 0.2

EPS 40.6 53.4 37.6 53.1 (7.4) (0.6)

Source: Company, Angel Research

At Rs949, the stock is trading at 18x FY2012E FDEPS, which is near to its fair value;

hence, we downgrade JISL from Buy to Accumulate, with a Target Price of Rs1,062.

May 12, 2010 7

8. Jain Irrigations Systems I 4QFY2010 Result Update

Profit & Loss Statement (Consolidated) (Rs cr)

Y/E March FY2007 FY2008 FY2009 FY2010 FY2011E FY2012E

Gross sales 1,458 2,304 2,945 3,642 4,613 5,810

Less: Excise duty 66 88 86 106 134 169

Net Sales 1,392 2,216 2,858 3,536 4,478 5,641

Other operating income

Total operating income 1,392 2,216 2,858 3,536 4,478 5,641

% chg 65 59 29 24 27 26

Total Expenditure 1,205 1,870 2,356 2,908 3,695 4,653

Net Raw Materials 781 1,177 1,551 1,909 2,418 3,046

Other Mfg costs 129 176 229 276 349 440

Personnel 125 245 293 325 412 519

Other 170 272 283 397 515 649

EBITDA 187 346 503 628 784 987

% chg 46 84 46 25 25 26

(% of Net Sales) 13 16 18 18 18 18

Depreciation& Amortisation 43 56 68 96 138 154

EBIT 144 290 434 532 646 833

% chg 73 101 50 22 21 29

(% of Net Sales) 10 13 15 15 14 15

Interest & other Charges* 77 137 244 202 229 241

Other Income 33 37 12 14 14 16

(% of PBT) 33 19 6 4 3 3

Recurring PBT 100 190 202 344 431 607

% chg 72 89 7 70 25 41

Extraordinary Expense/(Inc.) (1) (7) (7) 71 - -

PBT (reported) 99 183 196 415 431 607

Tax 20 54 66 139 145 204

(% of PBT) 20 30 34 34 34 34

PAT (reported) 79 129 130 275 286 404

Add: Share of earnings of

- - - - - -

associate

Less: Minority interest (MI) - 3 4 4 5 6

Prior period items 0 (2) 0 - - -

PAT after MI (reported) 79 126 126 271 280 397

ADJ. PAT 80 137 146 204 286 404

% chg 39 70 7 40 40 41

(% of Net Sales) 6 6 5 6 6 7

Basic EPS (Rs) 13 19 20 27 38 53

Fully Diluted EPS (Rs) 13 19 20 27 38 53

% chg 31 46 6 33 40 41

* including preference dividend

May 12, 2010 8

9. Jain Irrigations Systems I 4QFY2010 Result Update

Balance Sheet (Consolidated) (Rs cr)

Y/E March FY2007 FY2008 FY2009 FY2010E FY2011E FY2012E

SOURCES OF FUNDS

Equity Share Capital 62 72 72 76 76 76

Preference Capital 89 89 45 2 - -

Reserves& Surplus 264 713 780 1,069 1,311 1,663

Shareholders Funds 414 873 897 1,147 1,387 1,739

Minority Interest 10 65 70 75 80 87

Total Loans 859 1,276 1,817 1,820 2,002 2,022

Deferred Tax Liability - 11 71 102 90 32

Total Liabilities 1,284 2,225 2,855 3,144 3,559 3,879

APPLICATION OF FUNDS

Gross Block 862 1,262 1,750 2,150 2,450 2,695

Less: Acc. Depreciation 282 486 581 677 815 969

Net Block 580 776 1,170 1,474 1,636 1,726

Capital Work-in-Progress 79 120 121 121 123 135

Goodwill 66 120 167 167 167 167

Investments 20 60 20 20 20 20

Current Assets 999 1,873 2,312 2,458 2,999 3,624

Cash 44 104 117 142 202 231

Loans & Advances 116 287 320 352 401 506

Other 838 1,483 1,874 1,964 2,396 2,887

Current liabilities 514 741 964 1,125 1,414 1,822

Net Current Assets 484 1,132 1,348 1,333 1,585 1,802

Mis. Exp. not written off 54 16 30 30 30 30

Total Assets 1,284 2,225 2,855 3,144 3,559 3,879

Cash Flow (Consolidated) (Rs cr)

Y/E March FY2007 FY2008 FY2009 FY2010E FY2011E FY2012E

Profit before tax 104 194 199 415 431 607

Depreciation 41 56 68 96 138 154

Change in Working Capital (120) (488) (18) 244 31 2

Less: Other income

Direct taxes paid (9) (23) (22) (139) (145) (204)

Cash Flow from Operations 16 (261) 227 616 455 560

(Inc.)/ Dec. in Fixed Assets (256) (291) (464) (400) (302) (257)

(Inc.)/ Dec. in Investments (64) (51) (6) - - 0

Inc./ (Dec.) in loans and adv. (320) (343) (470) (400) (302) (257)

Other income

Cash Flow from Investing (320) (343) (470) (400) (302) (257)

Issue of Equity 42 174 (43) 43 (3) -

Inc./(Dec.) in loans 159 596 530 3 182 20

Dividend Paid (Incl. Tax) (26) (20) (23) (35) (43) (52)

Others (66) (136) (183) (202) (229) (241)

Cash Flow from Financing 109 615 281 (191) (93) (273)

Inc./(Dec.) in Cash (195) 11 38 25 60 29

Opening Cash balances 239 56 67 117 142 202

Closing Cash balances 44 67 105 142 202 231

May 12, 2010 9

11. Jain Irrigations Systems I 4QFY2010 Result Update

Research Team Tel: 022-4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment decision. Nothing in this

document should be construed as investment or financial advice. Each recipient of this document should make such investigations as they deem necessary to

arrive at an independent evaluation of an investment in the securities of the companies referred to in this document (including the merits and risks involved),

and should consult their own advisors to determine the merits and risks of such an investment.

Angel Securities Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make investment decisions that are

inconsistent with or contradictory to the recommendations expressed herein. The views contained in this document are those of the analyst, and the company

may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and trading volume, as

opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources believed to be true,

and are for general guidance only. Angel Securities Limited has not independently verified all the information contained within this document. Accordingly,

we cannot testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While Angel

Securities Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory, compliance, or other

reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced, redistributed or passed on,

directly or indirectly.

Angel Securities Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or other advisory services

in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in the past.

Neither Angel Securities Limited nor its directors, employees and affiliates shall be liable for any loss or damage that may arise from or in connection with the

use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section).

Disclosure of Interest Statement Jain Irrigation

1. Analyst ownership of the stock No

2. Angel and its Group companies ownership of the stock No

3. Angel and its Group companies’ Directors ownership of the stock No

4. Broking relationship with company covered No

Note: We have not considered any Exposure below Rs 1 lakh for Angel and its Group companies.

Address: Acme Plaza, ‘A’ Wing, 3rd Floor, M.V. Road, Opp. Sangam Cinema, Andheri (E), Mumbai - 400 059.

Tel : (022) 3952 4568 / 4040 3800

Angel Broking Ltd: BSE Sebi Regn No : INB 010996539 / CDSL Regn No: IN - DP - CDSL - 234 - 2004 / PMS Regn Code: PM/INP000001546 Angel Securities Ltd:BSE: INB010994639/INF010994639 NSE:

INB230994635/INF230994635 Membership numbers: BSE 028/NSE:09946

Angel Capital & Debt Market Ltd: INB 231279838 / NSE FNO: INF 231279838 / NSE Member code -12798 Angel Commodities Broking (P) Ltd: MCX Member ID: 12685 / FMC Regn No: MCX / TCM /

CORP / 0037 NCDEX : Member ID 00220 / FMC Regn No: NCDEX / TCM / CORP / 0302

May 12, 2010 11