1. 2QFY2011 Result Update | IT

October 14, 2010

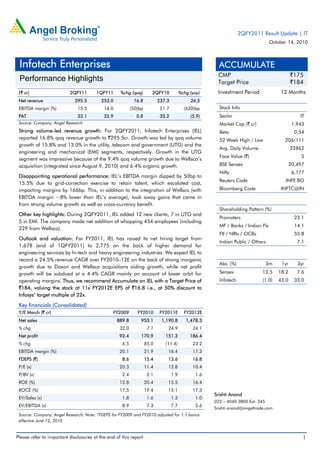

Infotech Enterprises ACCUMULATE

CMP `175

Performance Highlights Target Price `184

(` cr) 2QFY11 1QFY11 %chg (qoq) 2QFY10 %chg (yoy) Investment Period 12 Months

Net revenue 295.5 253.0 16.8 237.3 24.5

EBITDA margin (%) 15.5 16.0 (50)bp 21.7 (620)bp Stock Info

PAT 33.1 32.9 0.8 35.2 (5.9) Sector IT

Source: Company, Angel Research Market Cap (` cr) 1,943

Strong volume-led revenue growth: For 2QFY2011, Infotech Enterprises (IEL) Beta 0.54

reported 16.8% qoq revenue growth to `295.5cr. Growth was led by qoq volume 52 Week High / Low 206/111

growth of 15.8% and 13.0% in the utility, telecom and government (UTG) and the

Avg. Daily Volume 22862

engineering and mechanical (EMI) segments, respectively. Growth in the UTG

Face Value (`) 5

segment was impressive because of the 9.4% qoq volume growth due to Wellsco’s

acquisition (integrated since August 9, 2010) and 6.4% organic growth. BSE Sensex 20,497

Nifty 6,177

Disappointing operational performance: IEL’s EBITDA margin dipped by 50bp to

Reuters Code INFE.BO

15.5% due to grid-correction exercise to retain talent, which escalated cost,

impacting margins by 166bp. This, in addition to the integration of Wellsco (with Bloomberg Code INFTC@IN

EBITDA margin ~8% lower than IEL’s average), took away gains that came in

from strong volume growth as well as cross-currency benefit.

Shareholding Pattern (%)

Other key highlights: During 2QFY2011, IEL added 12 new clients, 7 in UTG and

Promoters 23.1

5 in EMI. The company made net addition of whopping 454 employees (including

MF / Banks / Indian Fls 14.1

229 from Wellsco).

FII / NRIs / OCBs 55.8

Outlook and valuation: For FY2011, IEL has raised its net hiring target from

Indian Public / Others 7.1

1,678 (end of 1QFY2011) to 2,775 on the back of higher demand for

engineering services by hi-tech and heavy engineering industries. We expect IEL to

record a 24.5% revenue CAGR over FY2010–12E on the back of strong inorganic

Abs. (%) 3m 1yr 3yr

growth due to Daxon and Wellsco acquisitions aiding growth, while net profit

growth will be subdued at a 4.4% CAGR mainly on account of lower orbit for Sensex 13.5 18.2 7.6

operating margins. Thus, we recommend Accumulate on IEL with a Target Price of Infotech (1.0) 43.0 33.0

`184, valuing the stock at 11x FY2012E EPS of `16.8 i.e., at 50% discount to

Infosys’ target multiple of 22x.

Key financials (Consolidated)

Y/E March (` cr) FY2009 FY2010 FY2011E FY2012E

Net sales 889.8 953.1 1,190.8 1,478.3

% chg 32.0 7.1 24.9 24.1

Net profit 92.4 170.9 151.3 186.4

% chg 6.5 85.0 (11.4) 23.2

EBITDA margin (%) 20.1 21.9 16.4 17.3

FDEPS (`) 8.6 15.4 13.6 16.8

P/E (x) 20.3 11.4 12.8 10.4

P/BV (x) 2.4 2.1 1.9 1.6

ROE (%) 12.8 20.4 15.5 16.4

ROCE (%) 17.5 19.4 15.1 17.3

Srishti Anand

EV/Sales (x) 1.8 1.6 1.3 1.0

022 – 4040 3800 Ext: 345

EV/EBITDA (x) 8.9 7.3 7.7 5.6

Srishti.anand@angeltrade.com

Source: Company, Angel Research; Note: *FDEPS for FY2009 and FY2010 adjusted for 1:1 bonus

effective June 12, 2010

Please refer to important disclosures at the end of this report 1

2. IT | 2QFY2011 Result Update

Exhibit 1: 2QFY2011 performance (Consolidated)

Y/E March (` cr) 2QFY2011 1QFY2011 % chg 2QFY2010 % chg 1HFY2011 1HFY2010 % chg

Total revenue 295.5 252.9 16.9 237.4 24.5 548.4 470.0 16.7

Salary cost 184.5 156.7 17.7 133.7 38.0 341.2 267.2 27.7

Gross Profit 111.0 96.2 15.4 103.7 7.0 207.2 202.8 2.1

% margins 37.6 38.0 (47 ) bp 43.7 (612) bp 37.8 43.2 (538 ) bp

Travel expenditure 18.8 16.4 14.8 13.6 38.2 35.2 25.0 40.7

Purchases for products/re-sale 10.4 8.6 20.2 6.8 51.3 19.0 15.4 23.0

Professional charges 7.6 7.6 (0.4) - 15.2 6.8 123.7

Other operating costs 28.5 23.2 22.7 31.8 (10.3) 51.7 51.7 0.0

EBITDA 45.8 40.4 13.4 51.5 (11.1) 86.2 103.9 (17.1)

% margins 15.5 16.0 (50) bp 21.7 (620) bp 15.7 22.1 (640) bp

Depreciation & amortisation 12.4 11.7 6.3 11.4 8.9 24.1 23.2 4.0

Financial expenses 0.6 0.2 137.5 0.2 137.5 0.8 0.5 68.8

Other Income 6.6 8.1 (17.8) 4.5 48.7 14.7 20.8 (29.3)

PBT 39.4 36.5 7.9 44.3 (11.1) 75.9 101.1 (24.9)

Tax 8.0 7.4 7.6 12.4 (35.5) 15.4 27.3 (43.8)

PAT 31.5 29.1 8.0 32.0 (1.6) 60.6 73.8 (17.9)

Share of profits 1.6 3.7 (56.0) 3.3 (50.8) 5.3 7.4 (28.7)

Minority Interest (0.0) (0.1) (20.0) 0.1 (0.1) 0.5 (118.8)

PAT after share of profits 33.1 32.9 0.8 35.2 (5.9) 66.0 80.7 (18.3)

PAT margins (%) 11.0 12.6 (163) bp 14.5 (359) bp 11.7 16.4 (473) bp

EPS (`) 3.0 3.0 0.3 3.3 (9.7) 5.9 5.3 11.9

Source: Company, Angel Research

Strong volume growth aiding top line

For 2QFY2011, IEL posted 16.9% qoq (24.5% yoy) revenue growth, backed by

qoq volume growth of 15.8% and 13.0% in the UTG and EMI segments,

respectively. Growth momentum in the EMI segment continues, whereas growth in

the UTG segment was stupendous because of 9.4% volume growth due to

Wellsco’s acquisition, which further aided the 6.4% organic volume growth. The

cross-currency movement, which acted as a spoilsport in 1QFY2011, aided the

top line by 3% as USD depreciated by 4%, 1.8% and 3% against GBP, Euro and

AUD, respectively. In USD terms, revenue grew by 14.6% qoq to US $63.5mn.

Exhibit 2: Segment-wise trend in volume growth

20.0%

15.0%

10.0%

% qoq

5.0%

0.0%

1QFY10 2QFY10 3QFY10 4QFY10 1QFY11 2QFY11

-5.0%

EMI UTG

Source: Company, Angel Research

October 14, 2010 2

3. IT | 2QFY2011 Result Update

Exhibit 3: Segment-wise trend in utilisation

90%

85%

80%

75%

%

70%

65%

60%

1QFY10 2QFY10 3QFY10 4QFY10 1QFY11

EMI UTG

Source: Company, Angel Research

During the quarter, upbeat demand for engineering services from verticals like

aerospace, heavy engineering and hi-tech resulted in strong utilisations despite the

spurt in voluntary attrition, which was as high as 5.6%. Demand for geospacial

information solutions (GIS) services also gained traction, with IEL witnessing over

20% qoq growth in its top two clients in the UTG segment. During 2QFY2011,

utilisation of the UTG segment fell primarily because of addition of 229 employees

from Wellsco’s acquisition.

Poor margin performance due to unanticipated cost escalation

EBITDA margin slipped by 50bp qoq due to unplanned grid correction exercise,

which became a necessity for the company to retain key skills. This impacted

EBITDA margin by 166bp qoq, which was further accentuated by lower pricing

and margin dilution due to Wellsco’s integration (with ~8% EBITDA margin lower

than the company’s average) taking away gains due to strong volume growth as

well as favourable cross-currency benefit.

Exhibit 4: Trend in margins

25.0

20.0

15.0

%

10.0

5.0

-

1QFY10 2QFY10 3QFY10 4QFY10 1QFY11 2QFY11E

EBITDA EBIT

Source: Company, Angel Research

October 14, 2010 3

4. IT | 2QFY2011 Result Update

Back to the hiring spree

During 2QFY2011, IEL made net employee addition of 454, with 229 employees

from Wellsco’s integration. For FY2011, the company has increased its net hiring

target from 1,678 to 2,775 on the back of a pick-up in demand.

Investment arguments

Strong growth momentum in EMI continues with UTG back on

the growth path

IEL is witnessing strong deal discussions in North America and Europe. In the EMI

segment, IEL along with aerospace (57% to revenue) verticals like heavy

engineering (10% to revenue) and hi-tech (11% to revenue) is gaining strong

momentum. Thus, the nature of spend in the EMI segment is becoming more

broad-based, resulting in robust volume growth. Some of the new long-term

projects in the EMI segment, such as the Hamilton Sunstrand, Seawell (engineering

support services for its drilling operations) and the recently signed US-based

Westinghouse (for providing nuclear energy-related network) projects, are

expected to witness strong ramp-ups with qoq growth of over 30% in the Hamilton

Sunstrand project and triple-digit growth in each of the latter two projects.

Moreover, IEL is witnessing deal discussions, which are larger in size typically

demanding 100–200 people instead of 30–40 billable resources few

quarters back.

The UTG segment is also back to strong growth after declining for more than two

quarters. Though the 15.8% volume growth was on the back of 9.4% coming in

from Wellsco’s acquisition, organically the company grew by 6.3% qoq. This is

primarily because the company’s top two clients grew by over 20% qoq. In fact,

going forward, IEL expects growth to be persistent in the UTG segment.

Outlook and valuation

Management is confident of recording an 8–10% CQGR over 2HFY2011 on the

back of broad-based growth in the EMI segment as well as stability in the UTG

vertical. We expect the company to grow at a 24.5% CAGR over FY2010–12E due

to inorganic initiatives like Daxon and Wellsco boosting volumes. However,

margins for FY2011 and FY2012 will settle at lower orbits of 16.4% and 17.3%,

respectively, as compared to 21.9% for FY2010 due to stronger rupee, competitive

cost pressures such as wage inflation and dilution due to integration of the

above-mentioned acquisition. This will lead to muted PAT CAGR of 4.4% over

FY2010–12E. Hence, we recommend an Accumulate rating on the stock with a

Target Price of Rs184, valuing the stock at 11x FY2012E EPS of `16.8 i.e., at

historical discount of 50% to Infosys’ target multiple of 22x, implying an upside of

5% from current levels.

October 14, 2010 4

5. IT | 2QFY2011 Result Update

Exhibit 5: Key assumptions

FY2011E FY2012E

Revenue growth (US $) 30.0 27.0

USD-INR rate (realised) 45.5 44.5

Net revenue growth (`) 24.9 24.2

EBIDTA margin (%) 16.4 17.3

Effective tax rate (%) 24.0 25.0

PAT growth (%) (11.5) 23.2

Source: Company, Angel Research

Exhibit 6: Change in estimates

FY2011E FY2012E

Parameter Earlier Revised Var. Earlier Revised Var.

(` cr) estimates estimates (%) estimates estimates (%)

Net revenue 1,095.0 1,190.6 8.7 1,264.0 1,478.3 17.0

EBITDA 199.0 195.0 (2.0) 228 255.0 11.8

PAT 154.0 151.3 (1.8) 178 186 4.5

Source: Company, Angel Research

We have upgraded our FY2011E and FY2012E revenue estimates due to

integration of strong growth in acquisitions like Daxon and factoring in Wellsco’s

numbers. EBITDA margins have been downgraded due to acquisition integration

effect, stronger rupee and competitive cost pressure like wage inflation to be

persistent.

Exhibit 7: One-year forward P/E band

350

300

250

Share Price (Rs)

200

150

100

50

0

Oct-05

Oct-06

Oct-07

Oct-08

Oct-09

Oct-10

Jan-06

Jan-07

Jan-08

Jan-09

Jan-10

Apr-05

Jul-05

Apr-06

Jul-06

Apr-07

Jul-07

Apr-08

Jul-08

Apr-09

Jul-09

Apr-10

Jul-10

Price 5x 10x 15x 20x

Source: Company, Angel Research

October 14, 2010 5

11. IT | 2QFY2011 Result Update

Research Team Tel: 022 - 4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or

other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in

the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please

refer to the latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and

its affiliates may have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement Infotech

1. Analyst ownership of the stock No

2. Angel and its Group companies ownership of the stock No

3. Angel and its Group companies' Directors ownership of the stock No

4. Broking relationship with company covered No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Returns): Buy (> 15%) Accumulate (5% to 15%) Neutral (-5 to 5%)

Reduce (-5% to 15%) Sell (< -15%)

October 14, 2010 11