How Automation is Driving Efficiency Through the Last Mile of Reporting

Axis Bank

1. 1QFY2011 Result Update | Banking

July 15. 2010

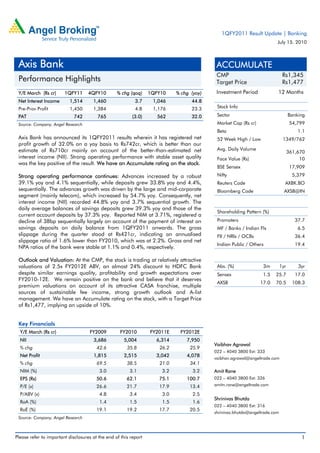

Axis Bank ACCUMULATE

CMP Rs1,345

Performance Highlights Target Price Rs1,477

Y/E March (Rs cr) 1QFY11 4QFY10 % chg (qoq) 1QFY10 % chg (yoy) Investment Period 12 Months

Net Interest Income 1,514 1,460 3.7 1,046 44.8

Pre-Prov Profit 1,450 1,384 4.8 1,176 23.3 Stock Info

PAT 742 765 (3.0) 562 32.0 Sector Banking

Source: Company, Angel Research Market Cap (Rs cr) 54,799

Beta 1.1

Axis Bank has announced its 1QFY2011 results wherein it has registered net 52 Week High / Low 1349/762

profit growth of 32.0% on a yoy basis to Rs742cr, which is better than our

estimate of Rs710cr mainly on account of the better-than-estimated net Avg. Daily Volume

361,670

interest income (NII). Strong operating performance with stable asset quality Face Value (Rs) 10

was the key positive of the result. We have an Accumulate rating on the stock.

BSE Sensex 17,909

Strong operating performance continues: Advances increased by a robust Nifty 5,379

39.1% yoy and 4.1% sequentially, while deposits grew 33.8% yoy and 4.4%, Reuters Code AXBK.BO

sequentially. The advances growth was driven by the large and mid-corporate Bloomberg Code AXSB@IN

segment (mainly telecom), which increased by 54.7% yoy. Consequently, net

interest income (NII) recorded 44.8% yoy and 3.7% sequential growth. The

daily average balances of savings deposits grew 39.3% yoy and those of the

Shareholding Pattern (%)

current account deposits by 37.3% yoy. Reported NIM at 3.71%, registered a

decline of 38bp sequentially largely on account of the payment of interest on Promoters 37.7

savings deposits on daily balance from 1QFY2011 onwards. The gross MF / Banks / Indian Fls 6.5

slippage during the quarter stood at Rs421cr, indicating an annualised FII / NRIs / OCBs 36.4

slippage ratio of 1.6% lower than FY2010, which was at 2.2%. Gross and net

Indian Public / Others 19.4

NPA ratios of the bank were stable at 1.1% and 0.4%, respectively.

Outlook and Valuation: At the CMP, the stock is trading at relatively attractive

valuations of 2.5x FY2012E ABV, an almost 24% discount to HDFC Bank Abs. (%) 3m 1yr 3yr

despite similar earnings quality, profitability and growth expectations over Sensex 1.5 25.7 17.0

FY2010-12E. We remain positive on the bank and believe that it deserves

AXSB 17.0 70.5 108.3

premium valuations on account of its attractive CASA franchise, multiple

sources of sustainable fee income, strong growth outlook and A-list

management. We have an Accumulate rating on the stock, with a Target Price

of Rs1,477, implying an upside of 10%.

Key Financials

Y/E March (Rs cr) FY2009 FY2010 FY2011E FY2012E

NII 3,686 5,004 6,314 7,950

Vaibhav Agrawal

% chg 42.6 35.8 26.2 25.9

022 – 4040 3800 Ext: 333

Net Profit 1,815 2,515 3,042 4,078

vaibhav.agrawal@angeltrade.com

% chg 69.5 38.5 21.0 34.1

NIM (%) 3.0 3.1 3.2 3.2 Amit Rane

EPS (Rs) 50.6 62.1 75.1 100.7 022 – 4040 3800 Ext: 326

P/E (x) 26.6 21.7 17.9 13.4 amitn.rane@angeltrade.com

P/ABV (x) 4.8 3.4 3.0 2.5

Shrinivas Bhutda

RoA (%) 1.4 1.5 1.5 1.6

022 – 4040 3800 Ext: 316

RoE (%) 19.1 19.2 17.7 20.5

shrinivas.bhutda@angeltrade.com

Source: Company, Angel Research

Please refer to important disclosures at the end of this report 1

2. Axis Bank | 1QFY2011 Result Update

Exhibit 1: 1QFY2011 Performance

Particulars (Rs cr) 1QFY2011 4QFY2010 % chg (qoq) 1QFY2010 % chg (yoy)

Interest Earned 3,326 2,988 11.3 2,906 14.5

Interest Expenses 1,812 1,528 18.5 1,860 (2.6)

Net Interest Income 1,514 1,460 3.7 1,046 44.8

Non-Interest Income 1,001 934 7.2 959 4.4

Total Income 2,515 2,394 5.1 2,004 25.5

Operating Expenses 1,065 1,010 5.4 828 28.6

Pre-Prov Profit 1,450 1,384 4.8 1,176 23.3

Provisions & Cont. 333 202 65.0 315 5.6

PBT 1,117 1,182 (5.5) 861 29.7

Prov. for Taxes 375 417 (10.0) 299 25.5

PAT 742 765 (3.0) 562 32.0

EPS (Rs) 18.2 18.9 (3.5) 15.6 16.6

Cost to Income (%) 42.3 42.2 41.3

Effective Tax Rate (%) 33.6 35.3 34.7

Net NPA (%) 0.4 0.4 0.4

Source: Company, Angel research

Stronger-than-expected advances growth

Advances increased by a robust 39.1% yoy and 4.1% sequentially to Rs1,08,609cr,

while deposits increased to Rs1,47,479cr, a growth of 33.8% yoy and 4.4%

sequentially. The advances growth was driven by the large and mid-corporate

segment (mainly telecom), which increased by 54.7% yoy. Consequently, the NII of

the bank recorded a growth of 44.8% yoy and 3.7% sequentially.

The deposit growth was driven by 17.2% qoq growth in Term deposits. The CASA

ratio of the bank declined to 40.2% (which is a seasonal phenomenon in the first

quarter of the financial year) from 46.7% in 4QFY2010, though it was stable on

yoy basis. On the positive side, the daily average balances of savings deposits

grew 39.3% yoy, while those of the current account deposits grew by 37.3% yoy.

Reported NIM at 3.71%, registered a decline of 38bp sequentially largely on

account of the payment of interest on savings deposits on daily balance from

1QFY2011 onwards.

July 15, 2010 2

4. Axis Bank | 1QFY2011 Result Update

Exhibit 4: Advances break-up (1QFY2011)

Agri

10%

SME

16%

Medium and

large Retail

corporates 19%

55%

Source: Company, Angel Research

Reasonable non-interest income growth

Fee income registered 19% yoy growth, rising to Rs743cr (Rs627cr) during

Q1FY2011, with strong contribution from the corporate segment. Fee income from

large and mid-corporate credit (including infrastructure) grew 42% yoy, followed

by that from treasury and debt and capital markets (22% yoy), capital markets

(10% yoy), retail business (8% yoy), business banking (6% yoy) and fee income

from the SME and agri lending businesses declined by 6%.

The bank generated Rs196cr (Rs326cr) of trading profits during Q1FY2011, a

decline of 40% yoy. About 60% of the total trading profit was related to trading of

corporate bonds.

Exhibit 5: Fee income mix

Rs Cr

Corporate Treasury Agri & SME Business banking Capital markets Retail

900

800

700

600

500

400

300

200

100

-

1QFY09

2QFY09

3QFY09

4QFY09

1QFY10

2QFY10

3QFY10

4QFY10

1QFY11

Source: Company, Angel Research

Asset quality stable

The gross slippage during the quarter stood at Rs421cr, indicating an annualised

slippage ratio of 1.6% lower than FY2010, which was at 2.2%. Gross NPAs

increased by 1.7% sequentially to Rs1,341cr, while net NPAs stood at Rs413cr

(Rs419cr). The NPA provisions were higher sequentially at Rs304cr in 1QFY2011

v/s 180cr in 4QFY2010. The bank has very healthy provision coverage ratio of

July 15, 2010 4

5. Axis Bank | 1QFY2011 Result Update

89.6% including technical write-offs. Gross and net NPA ratios of the bank were

stable at 1.1% and 0.4%, respectively.

The bank restructured loans aggregating Rs30cr during Q1FY2011. The

cumulative restructured assets till 1QFY2011, however declined to Rs 2,151cr

(1.81% of gross customer assets). The bank restructured ~69% in the large and

mid corporate credit, and 20% in the SME segment, while the balance was

restructured in agriculture and capital markets. A sector-wise analysis by the bank

indicates that restructuring of textiles was the highest at 22%, followed by shipping

22%, sugar, petroleum and real estate at 8% each.

Asset quality pressures have shown signs of easing, with an improving economic

outlook and reducing corporate leverage owing to which the NPA provisions are

expected to decline, going forward. Accordingly, we estimate a decline in NPA

provisions by 21.1% in FY2011E (implies NPA provision at 0.5% of assets in

FY2011E v/s an average of 0.3% over FY2005-09).

Exhibit 6: Asset quality trend

% Gross NPA % Net NPA % NPA Coverage (RHS) %

2.5 70.0

2.0

60.0

1.5

50.0

1.0

40.0

0.5

0.0 30.0

1QFY09 2QFY09 3QFY09 4QFY09 1QFY10 2QFY10 3QFY10 4QFY10 1QFY11

Source: Company, Angel Research

Operating expenses rise

Operating expenses were up by 28.6% yoy, with a cost-to-income ratio of 42.3%

(42.2% in 4QFY2010 and 41.3% in 1QFY2010) on the back of the strong

operating performance of the bank. During 1QFY2011, the bank added another

15 branches (191 during FY2010) and 181 ATMs, taking the network size to

1,050 branches and 4,474 ATMs. Operating costs of the bank are expected to

increase above the industry average due to its aggressive branch expansion plans

- the bank plans to open about 200 branches in FY2011E.

July 15, 2010 5

6. Axis Bank | 1QFY2011 Result Update

Exhibit 7: Trend in productivity

% Cost-to-income ratio

55

51

47

Flat cost-to-income ratio on the back

of strong operating performance

43

39

35

1QFY09

2QFY09

3QFY09

4QFY09

1QFY10

2QFY10

3QFY10

4QFY10

1QFY11

Source: Company, Angel Research

Strong capital adequacy

The bank has a healthy CAR of 14.5%, with tier-I capital of 10.3% at the end of

1QFY2011. The bank has not included profit during the quarter in tier-I capital as

per the RBI guidelines. With the leverage (assets/net worth) at 11.2x, the bank is

adequately capitalised to grow its advances at 5% above industry growth over

FY2010-12E.

High AFS exposure in investment book

The bank’s AFS portfolio constituted 32.7% and its HFT portfolio 6.4% of its total

investment book. The non-SLR investment was 32.5% of the total investment book.

The modified duration of AFS and HTM stood at 2.8 years and 4.6 years,

respectively.

July 15, 2010 6

7. Axis Bank | 1QFY2011 Result Update

Investment Arguments

Equity capital increased to support faster market share gains

We believe the bank’s Rs3,800cr QIP strongly positions it for market share gains

as the GDP and capital market activity continue to revive, with at least 500bp

higher growth than industry over FY2010-12E. The bank has expanded its network

at 35% CAGR since FY2003, driving fourfold increase in CASA market share to

4.0% by FY2010 (20bp yoy increase in FY2010). In our view, such gains (30-50bp

every year) will continue going forward, especially as network expansion (200+

additions, about 20-25% yoy) remains strong.

Fee income continues to drive higher RoEs

Fee income contribution across a spectrum of services has been a meaningful

1.9% of assets (almost twice the level in PSBs) over FY2008-10. With the capital

markets reviving, appetite for equity-based savings instruments is increasing and

general loan growth picking up. Fee income growth is also expected to gain

traction (30% CAGR over FY2010-12E), taking the contribution to 2.0% of assets

by FY2012E.

NPA concerns receding

In our view, the bank’s high credit growth was backed by strong low-cost deposit

growth, rather than chasing risky loans using high-cost deposits. Moreover, with

the improving economic outlook and reducing corporate leverage, NPA concerns

are receding. We expect NPA provisions/Avg Assets to decline to 0.3% by FY2012E

from 0.8% in FY2010.

July 15, 2010 7

8. Axis Bank | 1QFY2011 Result Update

Outlook and Valuation

At the CMP, the stock is trading at relatively attractive valuations of 2.5x FY2012E

ABV, a 24% discount to HDFC Bank. We remain positive on the bank and believe

that it deserves premium valuations on account of its attractive CASA franchise,

multiple sources of sustainable fee income, strong growth outlook and A-list

management.

Our Target P/ABV multiple of 2.8x on FY2012E estimates, represents a 20%

discount to our Target P/ABV multiple of 3.5x for HDFC Bank, keeping in mind the

relatively higher credit and market risks, though we believe that as the bank

establishes a longer and more credible track record of pricing and managing risks,

this gap vis-à-vis HDFC Bank could narrow down. We have an Accumulate rating

on the stock, with a Target Price of Rs1,477, implying an upside of 10% from

current levels.

Exhibit 8: Key Assumptions

Particulars (%) Earlier Estimates Revised Estimates

FY2011E FY2012E FY2011E FY2012E

Credit growth 25.0 25.0 26.0 27.0

Deposit growth 28.0 26.0 28.0 26.0

CASA Ratio 46.4 46.2 46.4 46.2

NIMs 3.1 3.1 3.2 3.2

Other Income growth 10.9 27.7 10.8 27.6

Growth in Staff Expenses 22.9 29.2 22.9 29.2

Growth in Other Expenses 22.9 29.2 22.9 29.2

Slippages 1.5 1.0 1.5 1.0

Coverage Ratio 69.4 70.4 69.4 70.4

Treasury gain/(loss) (% of investments) 0.25 0.20 0.25 0.20

Source: Company, Angel Research

Exhibit 9: Change in estimates

Particulars FY2011E FY2012E

Earlier Revised Earlier Revised

(Rs cr) Var (%) Var (%)

Estimates Estimates Estimates Estimates

Net Interest Income 6,154 6,314 2.6 7,739 7,950 2.7

Non-Interest Income 4,181 4,179 (0.0) 5,338 5,333 (0.1)

Total Income 10,335 10,494 1.5 13,076 13,283 1.6

Operating Expenses 4,561 4,561 - 5,891 5,891 -

Pre-Prov Profit 5,774 5,933 2.7 7,186 7,392 2.9

Provisions & Cont. 1,326 1,324 (0.2) 1,219 1,213 (0.5)

PBT 4,448 4,609 3.6 5,966 6,179 3.6

Prov. for Taxes 1,512 1,567 3.6 2,029 2,101 3.6

PAT 2,936 3,042 3.6 3,938 4,078 3.6

Source: Company, Angel Research

July 15, 2010 8

12. Axis Bank | 1QFY2011 Result Update

Research Team Tel: 022 - 4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or

other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in

the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please

refer to the latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and

its affiliates may have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement (Company name) Axis Bank

1. Analyst ownership of the stock No

2. Angel and its Group companies ownership of the stock Yes

3. Angel and its Group companies' Directors ownership of the stock Yes

4. Broking relationship with company covered No

Note: We have not considered any Exposure below Rs 1 lakh for Angel, its Group companies and Directors.

Ratings (Returns): Buy (> 15%) Accumulate (5% to 15%) Neutral (-5 to 5%)

Reduce (-5% to 15%) Sell (< -15%)

July 15, 2010 12