1. 4QFY2010 Result Update I Oil & Gas

May 26, 2010

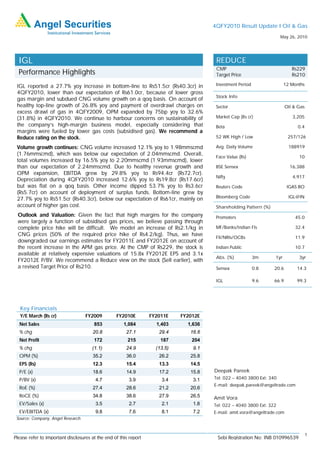

IGL REDUCE

CMP Rs229

Performance Highlights Target Price Rs210

IGL reported a 27.7% yoy increase in bottom-line to Rs51.5cr (Rs40.3cr) in Investment Period 12 Months

4QFY2010, lower than our expectation of Rs61.0cr, because of lower gross

Stock Info

gas margin and subdued CNG volume growth on a qoq basis. On account of

healthy top-line growth of 26.8% yoy and payment of overdrawl charges on Sector Oil & Gas

excess drawl of gas in 4QFY2009, OPM expanded by 75bp yoy to 32.6%

(31.8%) in 4QFY2010. We continue to harbour concerns on sustainability of Market Cap (Rs cr) 3,205

the company’s high-margin business model, especially considering that Beta 0.4

margins were fueled by lower gas costs (subsidised gas). We recommend a

Reduce rating on the stock. 52 WK High / Low 257/126

Volume growth continues: CNG volume increased 12.1% yoy to 1.98mmscmd Avg. Daily Volume 188919

(1.76mmscmd), which was below our expectation of 2.04mmscmd. Overall,

Face Value (Rs) 10

total volumes increased by 16.5% yoy to 2.20mmscmd (1.93mmscmd), lower

than our expectation of 2.24mmscmd. Due to healthy revenue growth and BSE Sensex 16,388

OPM expansion, EBITDA grew by 29.8% yoy to Rs94.4cr (Rs72.7cr).

Nifty 4,917

Depreciation during 4QFY2010 increased 12.6% yoy to Rs19.8cr (Rs17.6cr)

but was flat on a qoq basis. Other income dipped 53.7% yoy to Rs3.6cr Reuters Code IGAS.BO

(Rs5.7cr) on account of deployment of surplus funds. Bottom-line grew by

27.7% yoy to Rs51.5cr (Rs40.3cr), below our expectation of Rs61cr, mainly on Bloomberg Code IGL@IN

account of higher gas cost. Shareholding Pattern (%)

Outlook and Valuation: Given the fact that high margins for the company Promoters 45.0

were largely a function of subsidised gas prices, we believe passing through

complete price hike will be difficult. We model an increase of Rs2.1/kg in MF/Banks/Indian FIs 32.4

CNG prices (50% of the required price hike of Rs4.2/kg). Thus, we have

FII/NRIs/OCBs 11.9

downgraded our earnings estimates for FY2011E and FY2012E on account of

the recent increase in the APM gas price. At the CMP of Rs229, the stock is Indian Public 10.7

available at relatively expensive valuations of 15.8x FY2012E EPS and 3.1x

Abs. (%) 3m 1yr 3yr

FY2012E P/BV. We recommend a Reduce view on the stock (Sell earlier), with

a revised Target Price of Rs210. Sensex 0.8 20.6 14.3

IGL 9.6 66.9 99.3

Key Financials

Y/E March (Rs cr) FY2009 FY2010E FY2011E FY2012E

Net Sales 853 1,084 1,403 1,636

% chg 20.8 27.1 29.4 16.6

Net Profit 172 215 187 204

% chg (1.1) 24.9 (13.5) 9.1

OPM (%) 35.2 36.0 26.2 25.8

EPS (Rs) 12.3 15.4 13.3 14.5

P/E (x) 18.6 14.9 17.2 15.8 Deepak Pareek

P/BV (x) 4.7 3.9 3.4 3.1 Tel: 022 – 4040 3800 Ext: 340

E-mail: deepak.pareek@angeltrade.com

RoE (%) 27.4 28.6 21.2 20.6

RoCE (%) 34.8 38.6 27.9 26.5 Amit Vora

EV/Sales (x) 3.5 2.7 2.1 1.8 Tel: 022 – 4040 3800 Ext: 322

EV/EBITDA (x) 9.8 7.6 8.1 7.2 E-mail: amit.vora@angeltrade.com

Source: Company, Angel Research

1

Please refer to important disclosures at the end of this report Sebi Registration No: INB 010996539

2. IGL I 4QFY2010 Result Update

Exhibit 1: 4QFY2010 Performance

Y/E March (Rs cr) 4QFY10 4QFY10 %chg FY10 FY09 %chg

Total Operating Income 290 228 26.8 1,084 853 27.1

COGS 138 116 19.5 495 411 20.5

Total operating expenditure 195 156 25.4 697 553 26.2

EBITDA 94 73 29.8 387 300 28.8

EBITDA Margin % 32.6 31.8 35.7 35.2

Other Income 3 5 (53.7) 15 26 (41.3)

Depreciation 20 18 12.6 77 67 14.9

Interest - - - -

PBT 77 61 27.4 324 259 25.3

PBT Margin % 26.6 26.5 29.9 30.4

Total Tax 26 20 26.8 109 86 26.1

% of PBT 33.2 33.4 33.6 33.4

PAT 51 40 27.7 215 172 24.9

PAT Margin % 17.8 17.6 19.9 20.2

Source: Company, Angel Research

Exhibit 2: 4QFY2010 Segmental Performance

Segmental 4QFY10 4QFY09 %chg FY10 FY09 %chg

CNG

Volume (mnkgs) 135.7 121.1 12.1 528.7 460.4 14.8

Value (Rs cr) 285 226 26.1 1,076 862 24.8

PNG

Volume (mmscm) 25.0 15.4 62.3 62.7 54.3 15.4

Value (Rs cr) 39 30 30.2 116 100 16.1

Total Gross Sales (Rs cr) 324 256 26.5 1,192 962 23.9

Source: Company, Angel Research

Operating revenue marginally below expectation: For 4QFY2010, IGL reported a

26.8% yoy increase in operating income to Rs290cr (Rs228cr), which was marginally

below our expectation of Rs294cr. CNG volumes increased 12.1% yoy to

1.98mmscmd (1.76mmscmd), below our expectation of 2.04mmscmd. Whereas,

PNG volumes increased 62.3% yoy to 0.28mmscmd (0.17mmscmd) and were much

above our expectation of 0.19mmscmd due to clubbing of the sales to Adani under

the PNG segment during the quarter. Total volume increased by 16.5% yoy to

2.20mmscmd (1.93mmscmd), which was below our expectation of 2.24mmscmd,

due to lower-than-expected CNG volumes. Average gross CNG realisations were

higher on a yoy basis at Rs21/kg (Rs18.7/kg) due to the price hike effected on June

16, 2009, whereas average PNG realisations took a substantial dip on a yoy basis

during the quarter to Rs15.6/scm (Rs19.5/scm) due to clubbing of lower margin

sales to Adani under the PNG segment.

OPM expands by 75bp yoy to 32.6%: Gas sourcing cost increased 19.5% yoy to

Rs138cr (Rs116cr), which was above our expectation of Rs131cr. Gas cost per scm

came in at Rs6.8/scm (Rs6.6/scm) as against our expectation of Rs6.4/scm. Gross

gas spread during the quarter on a yoy basis stood higher at Rs7.5/scm

(Rs6.5/scm), but was lower than our expectation of Rs7.9/scm. On account of higher

gas cost per scm, gross gas spread also stood lower on a qoq basis at Rs7.5/scm

(Rs7.9/scm). Staff cost increased 49.1% yoy to Rs9.6cr (Rs6.5cr) owing to increased

minimum wage, whereas other operating expenditure increased 41.4% yoy to

Rs47.5cr (Rs33.6cr). OPM during the quarter expanded by 75bp yoy to 32.6%

(31.8%); however, it was lower than our expectation of 36.6%. On account of

healthy revenue growth and OPM expansion, operating profit grew by 29.8% yoy to

Rs94.4cr (Rs72.7cr). However, the same declined by 10.2% on a qoq basis due to

lower CNG volumes and increased gas cost.

May 26, 2010 2

3. IGL I 4QFY2010 Result Update

Depreciation flat qoq; other income dips: Depreciation during 4QFY2010 increased

12.6% yoy to Rs19.8cr (Rs17.6cr), but was flat on a qoq basis. Other income dipped

53.7% yoy to Rs3.6cr (Rs5.7cr) on account of deployment of surplus funds.

PAT up 27.7% yoy, but below our expectation: Higher revenue growth and OPM

expansion resulted in bottom-line growing 27.7% yoy to Rs51.5cr (Rs40.3cr), which

was below our expectation of Rs61cr, mainly on account of higher gas cost and

lower-than-anticipated CNG sales volumes.

Segment-wise performance

Robust growth continues in CNG and PNG volumes: On a sequential basis, IGL’s

CNG volumes declined marginally by 0.3% to 1.98mmscmd (1.94mmscmd), but

were higher on a yoy basis, primarily on the back of growth in CNG vehicle

conversions. However, PNG volumes registered robust growth of 53.4% sequentially

to 0.28mmscmd (0.18mmscmd) on account of clubbing of sales to Adani under the

PNG segment from the current quarter. PNG volumes were also higher on a yoy

basis by robust 62.3% yoy.

Exhibit 3: CNG, PNG Volume Trend

160.0 25.0 30.0 70.0

140.0 60.0

25.0

20.0

120.0

50.0

20.0

% yoy growth

100.0

% yoy growth

15.0

mmscm

40.0

mn kgs

80.0 15.0

30.0

60.0 10.0

10.0

20.0

40.0

5.0

5.0 10.0

20.0

0.0 0.0 0.0 0.0

1QFY2007

2QFY2007

3QFY2007

4QFY2007

1QFY2008

2QFY2008

3QFY2008

4QFY2008

1QFY2009

2QFY2009

3QFY2009

4QFY2009

1QFY2010

2QFY2010

3QFY2010

4QFY2010

1QFY2007

2QFY2007

3QFY2007

4QFY2007

1QFY2008

2QFY2008

3QFY2008

4QFY2008

1QFY2009

2QFY2009

3QFY2009

4QFY2009

1QFY2010

2QFY2010

3QFY2010

4QFY2010

CNG sales volumes % yoy growth (RHS) PNG sales volumes % yoy growth (RHS)

Source: Company, Angel Research

CNG realisations up; PNG realisations decline substantially: Net CNG realisations

stood flat on a qoq basis to Rs18.3/kg, but were higher on a yoy basis at Rs18.3/kg

(Rs16.3/kg) on account of price hike effected on June 16, 2009, while PNG

realisations declined by substantial 18.7% qoq to Rs15.6/scm (Rs19.5/scm) on

account of clubbing of low-margin sales to Adani under the PNG segment. The net

CNG sales increased marginally on a qoq basis to Rs248.8cr (Rs248.4cr), while

PNG sales registered robust growth of 24.6% qoq to Rs39.0cr (Rs31.3cr).

Exhibit 4: CNG, PNG — Net Realisations, Gross Margin

15.0 8.0 25.0 14.0

14.0

7.5 13.0

13.0 20.0

12.0 7.0 12.0

15.0

Rs/scm

Rs/scm

11.0

Rs/scm

Rs/scm

6.5 11.0

10.0 10.0

10.0

9.0 6.0

8.0 5.0

9.0

5.5

7.0

0.0 8.0

6.0 5.0

1QFY2007

2QFY2007

3QFY2007

4QFY2007

1QFY2008

2QFY2008

3QFY2008

4QFY2008

1QFY2009

2QFY2009

3QFY2009

4QFY2009

1QFY2010

2QFY2010

3QFY2010

4QFY2010

1QFY2007

2QFY2007

3QFY2007

4QFY2007

1QFY2008

2QFY2008

3QFY2008

4QFY2008

1QFY2009

2QFY2009

3QFY2009

4QFY2009

1QFY2010

2QFY2010

3QFY2010

4QFY2010

Net realisation of PNG Gross margin (RHS)

Net realisation of CNG Gross margin (RHS)

Source: Company, Angel Research

May 26, 2010 3

4. IGL I 4QFY2010 Result Update

Outlook and Valuation

IGL’s 4QFY2010 performance was lower than our expectations driven by

lower-than-expected gross margins because of higher-than-expected gas cost. On

account of the recent hike in APM gas prices, the profitability and outlook for the

stock will be significantly dependent on the extent of the pass through of the price

hike to end-users by the company.

We have been building a scenario of margin compression for IGL on account of

increased APM gas prices post the end of the marketing exclusivity (CY2012E

onwards). We have been long maintaining our stance that IGL’s gas sourcing cost

should increase to provide a level playing field for all the new entrants in the region.

As PNGRB does not regulate Marketing Margins of the CGD companies, it will have

to ensure that IGL does not get gas at lower prices vis-à-vis the new entrants in the

NCR and NCT region, so that there is free and fair determination of marketing

margins on a competitive basis. We believe that the recent increase in APM gas

prices provides a level playing field to the possible entrants.

IGL’s exorbitant margins in the past were fueled on account of three major factors:

1) liquid fuel-based pricing and APM gas pricing, 2) differential taxes structure on

CNG and other transport fuels, and 3) substitution of gas with liquid fuels. IGL has

historically charged its CNG and PNG customers based on prices of alternative

liquid fuel, while the company procures subsidised gas. Thus, IGL enjoys the benefits

of subsidy rather than passing it on to customers. Going ahead, we expect margins

to come under pressure, as this arbitrage should get eliminated to an extent by

de-regulation of APM gas prices. Recently, the government has increased APM gas

prices; however, there is no corresponding increase in CNG and PNG gas prices till

date, as the company is still mulling the extent of the hike. Given the fact that high

margins for the company were largely a function of subsidised gas prices, we

believe that passing through complete price hike will be difficult for IGL. On account

of this, we model an increase of Rs2.1/kg in CNG prices (50% of the required price

hike to maintain margins-Rs4.2/kg). Hence, we downgrade our earnings estimates

for FY2011E and FY2012E.

Exhibit 5: Revision in Estimates

Particulars Old estimates New estimates % chg

(Rs cr) FY11E FY12E FY11E FY12E FY11E FY12E

Revenues 1,275 1,534 1,403 1,636 10.1 6.7

EBITDA 449 482 367 422 (18.1) (12.6)

EBITDA margins (%) 35.2 31.4 26.2 25.8 901bp 567bp

EPS (Rs) 16.4 14.7 13.3 14.5 (18.7) (1.2)

Source: Company, Angel Research

However, considering that the APM gas price has been frozen until FY2014, the

possibility for price hikes on regular intervals will not arise for IGL, which will enable

the company to pass through increases in other operational expenditure post

FY2011E with relative ease. Earlier, we were expecting a steeper decline in

operating margins, assuming that large part of the increase in cost will be retained

by the company. However, now we model IGL to bear 50% of the total increase in

input cost due to recent APM gas price hike, which boosts our earnings estimates for

FY2013E and beyond.

At the CMP of Rs229, the stock is available at relatively expensive valuations of

15.8x FY2012E EPS and 3.1x FY2012E P/BV. On account of the change in our

estimates, we have revised the target price for the stock upwards to Rs210/share

(Rs190/share earlier), which provides a downside of 8.3% from the current level.

Thus, we upgrade our rating on the stock to Reduce (Sell earlier).

May 26, 2010 4

5. IGL I 4QFY2010 Result Update

Exhibit 6: One-year Forward Rolling P/E Band

230

15x

180 13x

Share Price (Rs)

11x

130

9x

7x

80

30

Apr-04

Aug-05

Apr-06

Aug-07

Apr-08

Aug-09

Apr-10

Dec-04

Dec-06

Dec-08

Source: Company, Angel Research

May 26, 2010 5

6. IGL I 4QFY2010 Result Update

Profit & Loss Statement (Rs cr)

Y/E March FY2007 FY2008 FY2009 FY2010 FY2011E FY2012E

Total operating income 614 706 853 1,084 1,403 1,636

% chg 15.0 20.8 27.1 29.4 16.6

Total Expenditure 359 406 553 697 1,035 1,214

Purchase of gas 268 303 411 495 839 989

Staff expenditure 14 15 24 31 37 42

Other operating expenditure 77 88 118 172 160 184

EBITDA 255 300 300 387 367 422

% chg 17.6 0.0 28.8 (4.9) 14.7

(% of Net Sales) 41.6 42.5 35.2 36.0 26.2 25.8

Depreciation and amortisation 60 63 67 77 103 128

EBIT 195 237 233 309 264 294

% chg 21.5 (2.0) 32.8 (14.5) 11.1

(% of Net Sales) 31.8 33.6 27.3 28.8 18.8 18.0

Interest & other Charges - - - - 4 8

Other Income 10 23 26 15 21 21

(% of PBT) 5.0 9.0 10.1 4.7 7.5 6.9

Share in profit of Associates - - - - - -

Recurring PBT 206 261 259 324 281 307

% chg 26.9 (0.8) 25.3 (13.3) 9.1

Extraordinary Expense/(Inc.) - - - - - -

PBT (reported) 206 261 259 324 281 307

Tax 68 86 86 109 95 104

(% of PBT) 32.9 33.1 33.4 33.6 33.7 33.7

PAT (reported) 138 174 172 215 187 204

Add: Share of earnings of

- - - - - -

associate

Less: Minority interest (MI) - - - - - -

Prior period items - - - - - -

PAT after MI (reported) 138 174 172 215 187 204

ADJ. PAT 138 174 172 215 187 204

% chg 26.5 (1.1) 24.9 (13.5) 9.1

(% of Net Sales) 22.5 24.7 20.2 20.1 13.3 12.4

Basic EPS (Rs) 9.9 12.5 12.3 15.4 13.3 14.5

Fully Diluted EPS (Rs) 9.9 12.5 12.3 15.4 13.3 14.5

% chg 26.5 (1.1) 24.9 (13.5) 9.1

May 26, 2010 6

7. IGL I 4QFY2010 Result Update

Balance Sheet (Rs cr)

Y/E March FY2007 FY2008 FY2009 FY2010E FY2011E FY2012E

SOURCES OF FUNDS

Equity Share Capital 140 140 140 140 140 140

Preference Capital - - - - - -

Reserves & Surplus 328 436 543 685 793 906

Shareholders Funds 468 576 683 825 933 1,046

Minority Interest - - - - - -

Total Loans - - - - 50 100

Net Deferred Tax Liability 30 24 21 17 14 14

Deposits from customers 5 7 27 27 28 30

Total Liabilities 503 607 731 870 1,025 1,190

APPLICATION OF FUNDS

Gross Block 613 668 817 959 1,249 1,549

Less: Acc. Depreciation 250 310 378 455 558 686

Net Block 363 358 439 504 691 863

Capital Work-in-Progress 31 59 82 140 150 150

Goodwill - - - - - -

Investments 128 109 104 104 104 104

Current Assets 106 228 259 314 358 386

Cash 40 140 146 172 182 184

Loans & Advances 25 41 55 70 91 106

Other 40 47 58 73 85 97

Current liabilities 125 146 154 192 277 314

Net Current Assets (19) 82 106 122 81 73

Mis. Exp. not written off - - - - - -

Total Assets 503 607 731 870 1,025 1,190

Cash Flow Statement (Rs cr)

Y/E March FY2007 FY2008 FY2009 FY2010E FY2011E FY2012E

Profit before tax 206 261 259 324 281 307

Depreciation 60 63 67 77 103 128

Deposits accepted during the year 1 1 20 1 1 1

Change in Working Capital 29 (2) (18) 9 51 10

Less: Other income (10) (23) (26) (15) (21) (21)

Direct taxes paid (73) (93) (89) (113) (98) (104)

Cash Flow from Operations 213 207 212 284 317 321

(Inc.)/ Dec. in Fixed Assets (58) (83) (172) (200) (300) (300)

(Inc.)/ Dec. in Investments (85) 19 5 - - -

Other income 10 23 26 15 21 21

Cash Flow from Investing (133) (41) (141) (185) (279) (279)

Issue of Equity - - - - - -

Inc./(Dec.) in loans - - - - 50 50

Dividend Paid (Incl. Tax) (39.9) (49) (66) (74) (79) (90)

Others (10.1) (18) 0 - - -

Cash Flow from Financing (50.0) (67) (65) (74) (29) (40)

Inc./(Dec.) in Cash 29.4 99 6 26 10 2

Opening Cash balances 11.0 40 140 146 172 182

Closing Cash balances 40.4 140 146 172 182 184

May 26, 2010 7

9. IGL I 4QFY2010 Result Update

Research Team Tel: 4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment decision. Nothing in this

document should be construed as investment or financial advice. Each recipient of this document should make such investigations as they deem necessary to

arrive at an independent evaluation of an investment in the securities of the companies referred to in this document (including the merits and risks involved),

and should consult their own advisors to determine the merits and risks of such an investment.

Angel Securities Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make investment decisions that are

inconsistent with or contradictory to the recommendations expressed herein. The views contained in this document are those of the analyst, and the company

may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and trading volume, as

opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources believed to be true,

and are for general guidance only. Angel Securities Limited has not independently verified all the information contained within this document. Accordingly,

we cannot testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Securities Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory, compliance, or

other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced, redistributed or passed on,

directly or indirectly.

Angel Securities Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or other advisory services

in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in the past.

Neither Angel Securities Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in connection with the

use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section).

Disclosure of Interest Statement IGL

1. Analyst ownership of the stock No

2. Angel and its Group companies ownership of the stock No

3. Angel and its Group companies’ Directors ownership of the stock No

4. Broking relationship with company covered No

Note: We have not considered any Exposure below Rs 1 lakh for Angel and its Group companies.

Address: Acme Plaza, ‘A’ Wing, 3rd Floor, M.V. Road, Opp. Sangam Cinema, Andheri (E), Mumbai - 400 059.

Tel: (022) 3952 4568 / 4040 3800

Angel Broking Ltd: BSE Sebi Regn No : INB 010996539 / CDSL Regn No: IN - DP - CDSL - 234 - 2004 / PMS Regn Code: PM/INP000001546 Angel Securities Ltd:BSE: INB010994639/INF010994639 NSE:

INB230994635/INF230994635 Membership numbers: BSE 028/NSE:09946

Angel Capital & Debt Market Ltd: INB 231279838 / NSE FNO: INF 231279838 / NSE Member code -12798 Angel Commodities Broking (P) Ltd: MCX Member ID: 12685 / FMC Regn No: MCX / TCM /

CORP / 0037 NCDEX : Member ID 00220 / FMC Regn No: NCDEX / TCM / CORP / 0302

May 26, 2010 9