Infosys - Result Update

•

0 likes•175 views

Infosys reported a 4.3% quarter-over-quarter growth in revenues to Rs. 6,198 crore for the first quarter of fiscal year 2011, backed by a 7.6% growth in volumes. However, earnings before interest and taxes (EBIT) margins fell by 1.8% due to annual wage hikes. Infosys revised its fiscal year 2011 revenue growth guidance upwards from 16-18% to 19-21% in rupee terms and maintained its earnings per share growth guidance of 7.2-11.5%. The growth was broad-based across services and verticals led by the banking, financial services and insurance sector.

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (20)

Similar to Infosys - Result Update

Similar to Infosys - Result Update (20)

More from Angel Broking

More from Angel Broking (20)

Recently uploaded

Recently uploaded (20)

Infosys - Result Update

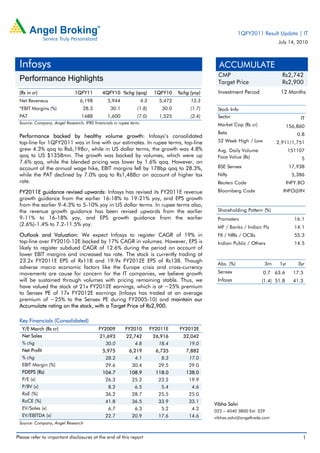

- 1. 1QFY2011 Result Update | IT July 14, 2010 Infosys ACCUMULATE CMP Rs2,742 Performance Highlights Target Price Rs2,900 (Rs in cr) 1QFY11 4QFY10 %chg (qoq) 1QFY10 %chg (yoy) Investment Period 12 Months Net Reveneus 6,198 5,944 4.3 5,472 13.3 *EBIT Margins (%) 28.3 30.1 (1.8) 30.0 (1.7) Stock Info PAT 1488 1,600 (7.0) 1,525 (2.4) Sector IT Source: Company, Angel Research; IFRS financials in rupee term; Market Cap (Rs cr) 156,860 Beta 0.8 Performance backed by healthy volume growth: Infosys’s consolidated top-line for 1QFY2011 was in line with our estimates. In rupee terms, top-line 52 Week High / Low 2,911/1,751 grew 4.3% qoq to Rs6,198cr, while in US dollar terms, the growth was 4.8% Avg. Daily Volume 151107 qoq to US $1358mn. The growth was backed by volumes, which were up Face Value (Rs) 5 7.6% qoq, while the blended pricing was lower by 1.6% qoq. However, on account of the annual wage hike, EBIT margins fell by 178bp qoq to 28.3%, BSE Sensex 17,938 while the PAT declined by 7.0% qoq to Rs1,488cr on account of higher tax Nifty 5,386 rate. Reuters Code INFY.BO FY2011E guidance revised upwards: Infosys has revised its FY2011E revenue Bloomberg Code INFO@IN growth guidance from the earlier 16-18% to 19-21% yoy, and EPS growth from the earlier 9-4.3% to 5-10% yoy in US dollar terms. In rupee terms also, the revenue growth guidance has been revised upwards from the earlier Shareholding Pattern (%) 9-11% to 16-18% yoy, and EPS growth guidance from the earlier Promoters 16.1 (2.6%)-1.4% to 7.2-11.5% yoy. MF / Banks / Indian Fls 14.1 Outlook and Valuation: We expect Infosys to register CAGR of 19% in FII / NRIs / OCBs 55.3 top-line over FY2010-12E backed by 17% CAGR in volumes. However, EPS is Indian Public / Others 14.5 likely to register subdued CAGR of 12.6% during the period on account of lower EBIT margins and increased tax rate. The stock is currently trading at 23.2x FY2011E EPS of Rs118 and 19.9x FY2012E EPS of Rs138. Though Abs. (%) 3m 1yr 3yr adverse macro economic factors like the Europe crisis and cross-currency movements are cause for concern for the IT companies, we believe growth Sensex 0.7 63.6 17.5 will be sustained through volumes with pricing remaining stable. Thus, we Infosys (1.4) 51.8 41.3 have valued the stock at 21x FY2012E earnings, which is at ~25% premium to Sensex PE of 17x FY2012E earnings (Infosys has traded at an average premium of ~25% to the Sensex PE during FY2005-10) and maintain our Accumulate rating on the stock, with a Target Price of Rs2,900. Key Financials (Consolidated) Y/E March (Rs cr) FY2009 FY2010 FY2011E FY2012E Net Sales 21,693 22,742 26,916 32,042 % chg 30.0 4.8 18.4 19.0 Net Profit 5,975 6,219 6,735 7,882 % chg 28.2 4.1 8.3 17.0 EBIT Margin (%) 29.6 30.4 29.5 29.0 FDEPS (Rs) 104.7 108.9 118.0 138.0 P/E (x) 26.3 25.2 23.2 19.9 P/BV (x) 8.2 6.5 5.4 4.6 RoE (%) 36.2 28.7 25.5 25.0 RoCE (%) 41.8 36.5 33.9 33.1 Vibha Salvi EV/Sales (x) 6.7 6.3 5.2 4.2 022 – 4040 3800 Ext: 329 EV/EBITDA (x) 22.7 20.9 17.6 14.6 vibhas.salvi@angeltrade.com Source: Company, Angel Research Please refer to important disclosures at the end of this report 1

- 2. IT | 1Q FY2011Result Update Exhibit 1: 1QFY2011 Performance (Consolidated, IFRS) Y/E March (Rs cr) FY2011 FY2010 % chg FY2010 % chg FY2010 FY2009 % chg 1Q 4Q (qoq) 1Q (yoy) Net Revenues 6,198 5,944 4.3 5,472 13.3 22,742 21,693 4.8 Software Development Expenses 3,648 3,415 6.8 3,139 16.2 13,020 12,535 3.9 Gross Profit 2,550 2,529 0.8 2,333 9.3 9,722 9,158 6.2 SG&A Expenses 795 740 7.4 689 15.4 2,812 2,737 2.7 EBIT 1,755 1,789 (1.9) 1,644 6.8 6,910 6,421 7.6 Other Income 239 252 (5.2) 269 (11.2) 990 473 109.3 Income before Income Taxes 1,994 2,041 (2.3) 1,913 4.2 7,900 6,894 14.6 Tax 506 441 14.7 388 30.4 1,681 919 82.9 Net Income 1,488 1,600 (7.0) 1,525 (2.4) 6,219 5,975 4.1 Diluted EPS (Rs) 26.1 28.0 (7.0) 26.7 (2.5) 108.9 104.7 4.0 Gross Profit Margin (%) 41.1 42.5 42.6 42.7 42.2 EBIT Margin (%) 28.3 30.1 30.0 30.4 29.6 Net Profit Margin (%) 24.0 26.9 27.9 27.3 27.5 Source: Company, Angel Research Exhibit 2: 1QFY2011 – Actual v/s Angel estimates (Rs cr) Estimates Actual Variation (%) Net Revenues 6,129 6,198 1.1 *EBIT Margin (%) 29.9 28.3 (1.5) PAT 1,550 1488 (4.0) Source: Company, Angel Research Broad-based growth across services and verticals driven by volumes Infosys recorded a 4.3% qoq (13.3% yoy) growth in top-line for 1QFY2011 backed by the 7.6% qoq growth in volumes, despite a 1.6% qoq dip in blended pricing and negative impact of 0.7% qoq appreciation in the rupee vis-à-vis the US dollar. The adverse cross-currency movement also restrained further growth in top-line as the rupee continued to appreciate even against the euro and GBP by 8.6% and 5.1% respectively, during the quarter. Exhibit 3: 1QFY2011 - Infosys guidance v/s actual performance 1QFY2011 IFRS Guidance range Performance In rupee term Revenues (Rs cr) 5,919-5,963 6,198 EPS (Rs) 24.34-24.79 26.05 In US dollar terms Revenues (US $mn) 1,330-1,340 1,358 Basic EPADS (US$) 0.55-0.56 0.57 Source: Company, Angel Research The growth was led by a strong sequential growth of 21.7%, 15.3% and 7.4% in Product Engineering services (PES), Testing and ADM (application development and maintenance) services, respectively. Verticals-wise, Infosys witnessed strong growth of 8.2% in BFSI led by the 13.8% growth recorded in the Insurance domain, while the Energy & Utilities and Retail verticals grew by 7.9% and 5.9%, respectively. July 14, 2010 2

- 3. IT | 1Q FY2011Result Update Exhibit 4: Services-wise revenue break-up Particulars (Rs cr) 1QFY11 4QFY10 1QFY10 % chg % chg qoq yoy Application Development & 2,529 2,354 2,326 7.4 8.7 Maintenance Development 1,047 999 1,056 4.9 (0.8) Maintenance 1,481 1,355 1,270 9.3 16.7 Business Process 353 369 334 (4.1) 5.8 Management Consulting and Package 1,543 1,545 1,335 (0.1) 15.6 Implementation Infrastructure Management 428 428 361 (0.1) 18.4 Testing Services 452 392 339 15.3 33.4 Product Engineering Services 130 107 131 21.7 (0.9) Systems Integration 260 267 208 (2.7) 25.2 Others 211 184 219 14.4 (3.7) Total services 5,907 5,647 5,253 4.6 12.4 Products 291 297.2 219 (2.0) 33.1 Total revenues 6,198 5,944 5,472 4.3 13.3 Source: Company, Angel Research Exhibit 5: Vertical-wise revenue break-up Particulars (Rs cr) 1QFY11 4QFY10 1QFY10 % chg % chg qoq yoy BFSI 2,237 2,069 1,806 8.2 23.9 Insurance 521 458 389 13.8 34.0 Banking & Financial Services 1,717 1,611 1,417 6.6 21.1 Manufacturing 1,209 1,201 1,122 0.7 7.7 Retail 818 773 722 5.9 13.3 Telecom 874 909 925 (3.9) (5.5) Energy & Utilities 372 345 312 7.9 19.2 Transportation & logistics 112 107 126 4.3 (11.4) Services 298 291 268 2.1 11.0 Others 279 250 192 11.7 45.6 Total revenues 6,198 5,944 5,472 4.3 13.3 Source: Company, Angel Research Geography-wise, strong growth was delivered by North America, India and Rest of World, which grew by 6.2%, 26.6% and 11.6% respectively, on a qoq basis. However, the 5.9% qoq decline in revenues from Europe on account of the ongoing crisis restrained growth. Exhibit 6: Geography-wise revenue break-up Region (Rs cr) 1QFY11 4QFY10 1QFY10 % chg % chg qoq yoy North America 4,171 3,929 3,540 6.2 17.8 Europe 1,258 1,337 1,352 (5.9) (6.9) India 105 83 49 26.6 113.9 Rest of the world 663 594 531 11.6 24.9 Total revenues 6,198 5,944 5,472 4.3 13.3 Source: Company, Angel Research July 14, 2010 3

- 4. IT | 1Q FY2011Result Update The company added 38 new clients during the quarter, of which 6 were from banking product Finacle, taking the total active clients to 590. The company added two US $100mn clients in 1QFY2011. The company also closed couple of large deals during the quarter whereas few transformational deals are in the pipeline. The Top-10 and -25 client accounts witnessed qoq growth of 6.6% and 5.2% respectively, while repeat business contributed 99.4% of the revenues compared to 95.4% in 4QFY2010. Sustained rupee appreciation across currencies, salary hikes impact margins During 1QFY2011, Infosys recorded a 178bp qoq (173bp yoy) contraction in EBIT margin, of which ~ 300bp impact came from negative impact of cross-currency movement and annual salary hikes effective during the quarter. However, the 160bp qoq increase in utilisation to 78.7% excluding trainees (utilisation including trainees was up by 370bp at 73%) during the quarter had a positive impact of ~100bp on the margins. In terms of operational costs, the negative impact on margins was on account of the 140bp increase in employee costs, as the company incurred US $12mn on visa costs during the quarter in addition to the salary hikes, while the General & Administration expenses also went up by 50bp qoq. Lower operational profitability, higher tax restrains bottom-line growth Infosys reported 5.2% qoq (11.2% yoy) decline in other income mainly on account of the forex loss of Rs81cr v/s gain of Rs97cr in 1QFY10. The tax rate during the quarter also went up from 21.6% in 4QFY2010 to 25.4% in 1QFY2011 as ~80% of profits (compared to 70% taxable earlier) would come under taxable income as the tax benefits availed earlier now phase out. Thus, lower operational profitability and other income coupled with higher tax outgo impacted bottom-line, which fell by 7% qoq (2.4% yoy). Gross addition of 8,859 employees; High attrition Infosys added a gross of 8,859 employees in 1QFY2011, while net additions were 1,026 (vis-à-vis 3,914 employees in 4QFY2010). The company has 114,822 employees on its rolls as of 1QFY2011, and has revised upwards its gross addition guidance from earlier 30,000 to 36,000 employees as on 1QFY11 expecting strong volume growth in FY2011E. The attrition rate however stood high at 15.8% in 1QFY2011 on account of the overall buoyancy in the job market with a strong economic recovery. July 14, 2010 4

- 5. IT | 1Q FY2011Result Update Exhibit 7: Quarterly attrition trend Source: Company, Angel Research Strong 2QFY2011E guidance Although the company registered a subdued performance for 1QFY2011, it has given a strong revenue growth guidance of 6-7% for 2QFY2011E, in rupee terms backed by growth in volumes. The company also plans to make gross employee addition of 14,000 in 2QF20Y11E. Margins are expected to improve compared to 1QFY2011 as there will be no impact of the annual wage hike, which has already happened in 1QFY2011. The company has guided for 5-7% qoq growth in EPS. FY2011E guidance revised upwards Infosys has revised upwards FY2011E revenue growth guidance in US dollar terms ranging between 19 - 21% yoy, and EPS growth to range between 5.2 - 9.6% yoy. In rupee terms, the revenue guidance ranges between Rs26,441 - 26,885cr, a yoy growth of 16.3 - 18.2%, and EPS ranges between Rs112.2 - 116.7, implying yoy growth of 7.2 -11.5%. The company’s strong upward guidance is based on the robust client feedback with improvement in the demand environment and infusion of 36,000 gross employees to deliver strong volume-backed growth with pricing expected to remain stable. Exhibit 8: 2QFY2011E, FY2011E guidance Guidance 2QFY11E FY2011E Revised FY2011E IFRS As on 4QFY10 As on 1QFY11 Revenues (Rs cr) 6,563-6,626 24,796-25,239 26,441-26,885 EPS (Rs) 27.42-27.95 106.82-111.28 112.21-116.73 IFRS Revenues (US $bn) 1.41-1.43 5.57-5.67 5.72-5.81 Basic EPADS (US$) 0.59-0.60 2.40-2.50 2.42-2.52 Source: Company, Angel Research July 14, 2010 5

- 6. IT | 1Q FY2011Result Update Investment Arguments Strong growth in US and emerging geographies to combat Europe crisis: Though Europe continues to be a spoilt sport for the Indian IT industry till the concerns wear out, some of the other levers for the company’s growth are the recovery in the IT spend from the US and emerging geographies. The company also expects to get increasing wallet share from its existing clients and is witnessing improvement in IT spends more on offshore. Moreover to combat the European concerns the company plans to proactively increase investments in creating capabilities and hence plans for strong manpower intake in FY2011. We expect growth to remain broad-based with key verticals like BFSI, energy and utilities and high-margin services like consulting and package implementation are expected to do well. Strong volume led growth with stable pricing to maintain profitability Though the cross-currency movement remains a concern, we expect the company’s short-term hedging policy to arrest its impact on operational profitability to a large extent. However, the increasing attrition rate is a cause for concern. Hence, we expect employee cost to move up going forward to retain the best of the talents, as the job opportunities are coming back with buoyancy in the overall economy. However, on the back of strong volume-backed growth and stable pricing, we believe that the company will maintain the EBIT margins albeit in a narrow band going forward. Outlook and Valuation We expect Infosys to register CAGR of 19% in top-line over FY2010-12E backed by 17% CAGR in volumes. However, EPS is likely to register subdued CAGR of 12.6% during the period on account of lower EBIT margins and increased tax rate. The stock is currently trading at 23.7x FY2011E EPS of Rs118 and 20x FY2012E EPS of Rs138. Though adverse macro economic factors like the Europe crisis and cross-currency movements are cause for concern for the IT companies, we believe growth will be sustained through volumes with pricing remaining stable. Thus, we have valued the stock at 21x FY2012E earnings, which is at ~25% premium to Sensex PE of 17x FY2012E earnings (Infosys has traded at an average premium of ~25% to the Sensex PE during FY2005-10) and maintain our Accumulate rating on the stock, with a Target Price of Rs2,900. July 14, 2010 6

- 7. IT | 1Q FY2011Result Update Exhibit 9: Key Assumptions FY2011E FY2012E Volume growth 18.6 15.2 Pricing growth 1 2 Revenue growth (in US $ terms) 20.4 17.9 USD-INR rate (realised) 46.5 47.0 Revenue growth (in Re terms) 18.4 19 Employee addition (Net) 13,639 12,000 EBIT margin (%) 29.5 29.0 Tax rate (%) 25 25 EPS growth (%) 8.3 17 Source: Company, Angel Research Exhibit 10: Change in Estimates FY2011E FY2012E Parameter Earlier Revised Variation Earlier Revised Variation (Rs cr) Estimates Estimates (%) Estimates Estimates (%) Net Revenues 25,524 26,916 5.5 31,071 32,042 3.1 EBIT (excl. 7,758 7,951 2.5 9,351 9,277 (0.8) other income) Other Income 1,166 1,029 (11.7) 1,476 1,233 (16.5) PBT 8,924 8,980 0.6 10,827 10,510 (2.9) Tax 2,231 2,245 0.6 2,815 2,627 (6.7) PAT 6,693 6,735 0.6 8,012 7,882 (1.6) Source: Company, Angel Research In line with the upward revision in Infosys’s guidance for FY2011E and expected higher infusion of gross manpower, we have also upgraded our FY2011E and FY2012E top-line estimates. We however, expect other income to be lower on account of the expected unfavourable cross-currency movement. We estimate PAT to be slightly higher in FY2011E compared to our earlier estimates, as volume growth would take care of lower margins. However, PAT in FY2012E would be slightly lower than our earlier estimates, as margins are expected to dip with the rise in employee costs to arrest higher attrition. Exhibit 11: Angel EPS forecast v/s consensus Year (%) Angel forecast Bloomberg consensus Variation FY2011E 118.0 121.7 (3.0) FY2012E 138.0 144.9 (4.8) Source: Company, Angel Research July 14, 2010 7

- 8. IT | 1Q FY2011Result Update Exhibit 12: P/E chart 4,000 25x 3,000 Share Price (Rs) 20x 2,000 15x 10x 1,000 0 Jul-05 Jan-06 Jul-06 Jan-07 Jul-07 Jan-08 Jul-08 Jan-09 Jul-09 Jan-10 Jul-10 Apr-05 Apr-06 Apr-07 Apr-08 Apr-09 Apr-10 Oct-05 Oct-06 Oct-07 Oct-08 Oct-09 Source: Company, Angel Research Exhibit 13: Premium/Discount in Infosys P/E v/s Sensex P/E 110.0 90.0 70.0 50.0 30.0 (%) 10.0 (10.0) (30.0) (50.0) Jul-05 Jul-06 Jul-07 Jul-08 Jul-09 Jul-10 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Apr-05 Apr-06 Apr-07 Apr-08 Apr-09 Apr-10 Oct-05 Oct-06 Oct-07 Oct-08 Oct-09 Premium/Discount to Sensex Avg. Historical Premium Source: Company, Angel Research Exhibit 14: Recommendation Summary Company Reco. CMP Tgt Price Upside FY2012E FY2012E FY2010-12E FY2012E FY2012E (Rs) (Rs) (%) P/BV (x) P/E (x) EPS CAGR (%) RoCE (%) RoE (%) 3iInfotech Buy 65 129.0 98.3 0.6 3.7 218.4 15.0 16.5 Educomp Buy 598 734.0 22.8 2.7 13.0 26.9 21.0 22.3 HCL Tech Buy 357 420 17.7 2.9 13.3 17.9 40.9 24.1 Infosys Accumulate 2,742 2900 5.8 4.6 19.9 12.6 33.1 25.0 Infotech Enterprises Buy 176 232.0 32.2 1.4 9.1 12.1 18.1 17.0 Mphasis Buy 624 872.0 39.7 2.5 9.7 14.9 41.6 29.2 NIIT Buy 69 83 19.5 1.8 12.0 16.6 12.1 15.8 TCS Buy 775 921 18.9 5.1 18.5 9.2 50.7 29.8 Tech Mahindra Buy 764 1,168.0 52.9 2.2 11.4 11.8 73.4 22.0 Wipro Buy 398 475.0 19.4 3.6 16.8 12.0 27.9 23.6 Source: Company, Angel Research July 14, 2010 8

- 9. IT | 1Q FY2011Result Update Profit & Loss Statement (Consolidated IFRS) Y/E March (Rs cr) FY2009 FY2010 FY2011E FY2012E Gross sales 21,693 22,742 26,916 32,042 Less: Excise duty - - - - Net Sales 21,693 22,742 26,916 32,042 Other operating income 473 990 1,029 1,233 Total operating income 22,166 23,732 27,946 33,275 % chg 27.4 7.1 17.8 19.1 Total Expenditure 15,272 15,832 18,966 22,765 Cost of Services 12,535 13,020 15,716 19,225 SGA 2,737 2,812 3,250 3,540 EBIT 6,894 7,900 8,980 10,510 % chg 16.6 14.6 13.7 17.0 (% of Net Sales) 29.6 30.4 29.5 29.0 Interest & other Charges - - - - Recurring PBT 6,894 7,900 8,980 10,510 % chg 29.0 14.6 13.7 17.0 Extraordinary Expense/(Inc.) - - - - PBT (reported) 6,894 7,900 8,980 10,510 Tax 919 1,681 2,245 2,627 (% of PBT) 13.3 21.3 25.0 25.0 PAT (reported) 5,975 6,219 6,735 7,882 Add: Share of earnings of associate - - - - Less: Minority interest (MI) - - - - Prior period items - - - - PAT after MI (reported) 5,975 6,219 6,735 7,882 ADJ. PAT 5,975 6,219 6,735 7,882 % chg 28.2 4.1 8.3 17.0 (% of Net Sales) 27.5 27.3 25.0 24.6 Basic EPS (Rs) 104.9 109.0 118.0 138.0 Fully Diluted EPS (Rs) 104.7 108.9 118.0 138.0 % chg 28.2 4.1 8.3 17.0 July 14, 2010 9

- 10. IT | 1Q FY2011Result Update Balance Sheet (Consolidated IFRS) Y/E March (Rs cr) FY2009 FY2010 FY2011E FY2012E SOURCES OF FUNDS Equity Share Capital 286 286 286 286 Reserves& Surplus 18,908 23,787 28,514 34,054 Shareholders Funds 19,194 24,073 28,800 34,340 Minority Interest - - - - Total Loans - - - - Deferred Tax Liability (408) (232.0) (232.0) (232.0) Total Liabilities 18,786 23,841 28,568 34,108 APPLICATION OF FUNDS Net Block 5,666 5,991 6,291 6,691 Capital Work-in-Progress 262 347 447 547 Investments - - - - Current Assets 15,826 20,928 26,229 32,434 Cash 10,993 12,111 16,112 20,917 Loans & Advances - - - - Other 4,833 8,817 10,117 11,517 Current liabilities 2,968 3,425 4,399 5,564 Net Current Assets 12,858 17,503 21,830 26,870 Total Assets 18,786 23,841 28,568 34,108 Cash Flow Statement (Consolidated IFRS) Y/E March (Rs cr) FY2009 FY2010 FY2011E FY2012E Profit before tax 6,894 7,900 8,980 10,510 Depreciation - - - - Change in Working Capital (1,419) (3,017) (226) (135) Less: Other income 473 990 1,029 1,233 Direct taxes paid 919 1,681 2,245 2,627 Cash Flow from Operations 4,083 2,212 5,480 6,515 Inc./ (Dec.) in Fixed Assets (835) 410 500 600 Inc./ (Dec.) in Investments - - - - Inc./ (Dec.) in loans and advances Other income 473 990 1,029 1,233 Cash Flow from Investing (1,308) (580) (529) (633) Issue of Equity 64 - - - Inc./(Dec.) in loans - - - - Dividend Paid (Incl. Tax) 1,573 1,674 2,008 2,342 Others Cash Flow from Financing (1,509) (1,674) (2,008) (2,342) Inc./(Dec.) in Cash 3,882 1,118 4,001 4,805 Opening Cash balances 7,111 10,993 12,111 16,112 Closing Cash balances 10,993 12,111 16,112 20,917 July 14, 2010 10

- 11. IT | 1Q FY2011Result Update Key Ratios Y/E March FY2009 FY2010 FY2011E FY2012E Valuation Ratio (x) P/E (on FDEPS) 26.3 25.2 23.2 19.9 P/CEPS 26.3 25.2 23.2 19.9 P/BV 8.2 6.5 5.4 4.6 Dividend yield (%) 0.9 0.9 1.1 1.3 EV/Sales 6.7 6.3 5.2 4.2 EV/EBITDA 22.7 20.9 17.6 14.6 EV / Total Assets 6.7 5.3 4.2 3.4 Per Share Data (Rs) EPS (Basic) 104.9 109.0 118.0 138.0 EPS (fully diluted) 104.7 108.9 118.0 138.0 Cash EPS 104.3 108.9 118.0 138.0 DPS 23.5 25.1 30.1 35.1 Book Value 335.1 421.6 504.4 601.4 Dupont Analysis EBIT margin 29.6 30.4 29.5 29.0 Tax retention ratio 86.7 78.7 75.0 75.0 Asset turnover (x) 2.1 1.6 1.6 1.8 ROIC (Post-tax) 52.8 37.5 36.5 38.1 Cost of Debt (Post Tax) - - - - Leverage (x) - - - - Operating ROE 31.1 25.8 23.3 22.8 Returns (%) ROCE (Pre-tax) 41.9 36.5 33.9 33.1 Angel ROIC (Pre-tax) 41.9 36.5 33.9 33.1 ROE 36.2 28.7 25.5 25.0 Turnover ratios (x) Asset Turnover (Gross Block) 4.7 5.1 5.6 6.0 Inventory / Sales (days) - - - - Receivables (days) 61.8 56.1 55.5 54.6 Payables (days) 19.6 18.8 18.8 18.4 Working capital cycle (ex-cash) (days) 22.3 90.3 80.7 70.5 Solvency ratios (x) Net debt to equity - - - - Net debt to EBITDA - - - - Interest Coverage (EBIT / Interest) - - - - July 14, 2010 11

- 12. IT | 1Q FY2011Result Update Disclaimer This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and risks of such an investment. Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this document are those of the analyst, and the company may or may not subscribe to all the views expressed within. Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's fundamentals. The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this document is for general guidance only. Angel Broking or any of its affiliates/ group companies shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report. Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory, compliance, or other reasons that prevent us from doing so. This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced, redistributed or passed on, directly or indirectly. Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in the past. Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in connection with the use of this information. Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Disclosure of Interest Statement (Company name) Infosys 1. Analyst ownership of the stock No 2. Angel and its Group companies ownership of the stock No 3. Angel and its Group companies' Directors ownership of the stock No 4. Broking relationship with company covered No Note: We have not considered any Exposure below Rs 1 lakh for Angel, its Group companies and Directors. Ratings (Returns) : Buy (> 15%) Accumulate (5% to 15%) Neutral (-5 to 5%) Reduce (-5% to 15%) Sell (< -15%) July 14, 2010 12