call girls in Nand Nagri (DELHI) 🔝 >༒9953330565🔝 genuine Escort Service 🔝✔️✔️

Elecon

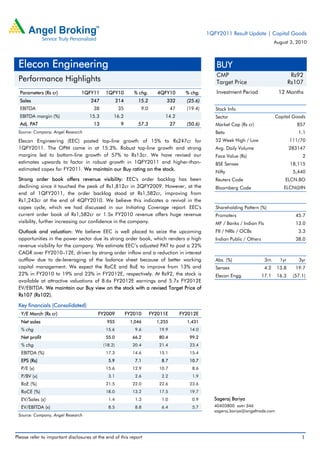

1. 1QFY2011 Result Update | Capital Goods

August 3, 2010

Elecon Engineering BUY

CMP Rs92

Performance Highlights Target Price Rs107

Parameters (Rs cr) 1QFY11 1QFY10 % chg. 4QFY10 % chg. Investment Period 12 Months

Sales 247 214 15.2 332 (25.6)

EBITDA 38 35 9.0 47 (19.4) Stock Info

EBITDA margin (%) 15.3 16.2 14.2 Sector Capital Goods

Adj. PAT 13 9 57.3 27 (50.6) Market Cap (Rs cr) 857

Source: Company, Angel Research Beta 1.1

Elecon Engineering (EEC) posted top-line growth of 15% to Rs247cr for 52 Week High / Low 111/70

1QFY2011. The OPM came in at 15.3%. Robust top-line growth and strong Avg. Daily Volume 283147

margins led to bottom-line growth of 57% to Rs13cr. We have revised our Face Value (Rs) 2

estimates upwards to factor in robust growth in 1QFY2011 and higher-than- BSE Sensex 18,115

estimated capex for FY2011. We maintain our Buy rating on the stock.

Nifty 5,440

Strong order book offers revenue visibility: EEC's order backlog has been Reuters Code ELCN.BO

declining since it touched the peak of Rs1,812cr in 3QFY2009. However, at the Bloomberg Code ELCN@IN

end of 1QFY2011, the order backlog stood at Rs1,582cr, improving from

Rs1,243cr at the end of 4QFY2010. We believe this indicates a revival in the

capex cycle, which we had discussed in our Initiating Coverage report. EEC's Shareholding Pattern (%)

current order book of Rs1,582cr or 1.5x FY2010 revenue offers huge revenue Promoters 45.7

visibility, further increasing our confidence in the company. MF / Banks / Indian Fls 13.0

Outlook and valuation: We believe EEC is well placed to seize the upcoming FII / NRIs / OCBs 3.3

opportunities in the power sector due its strong order book, which renders a high Indian Public / Others 38.0

revenue visibility for the company. We estimate EEC’s adjusted PAT to post a 22%

CAGR over FY2010–12E, driven by strong order inflow and a reduction in interest

outflow due to de-leveraging of the balance sheet because of better working Abs. (%) 3m 1yr 3yr

capital management. We expect the RoCE and RoE to improve from 13% and Sensex 4.2 13.8 19.7

22% in FY2010 to 19% and 23% in FY2012E, respectively. At Rs92, the stock is Elecon Engg. 17.1 16.3 (57.1)

available at attractive valuations of 8.6x FY2012E earnings and 5.7x FY2012E

EV/EBITDA. We maintain our Buy view on the stock with a revised Target Price of

Rs107 (Rs102).

Key financials (Consolidated)

Y/E March (Rs cr) FY2009 FY2010 FY2011E FY2012E

Net sales 955 1,046 1,255 1,431

% chg 15.6 9.6 19.9 14.0

Net profit 55.0 66.2 80.4 99.2

% chg (18.2) 20.4 21.4 23.4

EBITDA (%) 17.3 14.6 15.1 15.4

EPS (Rs) 5.9 7.1 8.7 10.7

P/E (x) 15.6 12.9 10.7 8.6

P/BV (x) 3.1 2.6 2.2 1.9

RoE (%) 21.5 22.0 22.6 23.6

RoCE (%) 18.0 13.2 17.5 19.7

EV/Sales (x) 1.4 1.3 1.0 0.9 Sageraj Bariya

EV/EBITDA (x) 8.5 8.8 6.4 5.7 40403800 extn 346

sageraj.bariya@angeltrade.com

Source: Company, Angel Research

Please refer to important disclosures at the end of this report 1

2. Elecon Engineering | 1QFY2011 Result Update

Exhibit 1: Quarterly performance

Y/E March (Rs cr) 1QFY2011 1QFY2010 % chg FY2010 FY2009 % chg

Total sales 246.0 212.3 1035.9 942.3

Other op. income 1.1 2.2 10.4 12.7

Net revenue 247.2 214.5 15.2 1046.4 955.1 9.6

Raw material cost 169.2 142.4 626.9 503.0

Gross profit 76.9 69.9 409.0 439.3

Gross margin 31.2 32.9 39.5 46.6

Employee expenses 12.0 8.9 43.5 43.8

As % of sales 4.8 4.2 4.2 4.6

Other expenditure 28.1 28.4 2168.9 2385.9

As % of sales 11.4 13.2 11.0 11.5

Total expenditure 209.3 179.7 895.1 792.5

Operating profit 37.9 34.8 9.0 151.2 162.6 (7.0)

OPM (%) 15.3 16.2 14.6 17.3

Depreciation 8.9 7.5 33.1 22.1

EBIT 29.0 27.3 6.2 118.1 140.4 (15.9)

EBIT (%) 11.7 12.7 11.4 14.9

Other income 0.1 0.0 24.8 9.6

Interest 9.8 14.4 52.6 61.9

PBT (excl of ext items) 19.2 12.9 49.2 90.3 88.1 2.5

Ext items 0.0 0.0 0.0 0.0

PBT (incl of ext items) 19.2 12.9 90.3 88.1

Tax 5.8 4.4 24.1 30.6

Reported PAT 13.4 8.5 66.2 57.5

Minority & other item 0.0 0.0 0.0 2.5

Adj PAT 13.4 8.5 57.3 66.2 55.0 20.4

Report EPS (Rs) 1.4 0.9 7.1 6.2

Adj EPS (Rs) 1.4 0.9 7.1 5.9

Source: Company, Angel Research

Sales momentum picking up

EEC reported robust 1QFY2011 revenue of Rs247cr (up 15% yoy), supported by

16% growth in the material handling division (MHE) and 11% growth in the gear

division. We believe sales momentum that picked up pace in 4QFY2010 is likely to

be maintained on account of strong order intake.

August 3, 2010 2

4. Elecon Engineering | 1QFY2011 Result Update

Robust order book

Order inflow for 1QFY2011 increased 657% yoy to Rs1,840cr. The order backlog

stood at Rs1,582cr (MHE: Rs1,253cr, Gears: Rs329cr). Strong order inflow was

driven by demand from core sectors such as power, cement, steel and mining. The

company booked new order worth nearly Rs600cr against Rs700cr booked in

FY2010. Given the ongoing live-enquiries worth Rs2,500cr, management

continues to expect better traction in orders from major industries including power

and steel.

Exhibit 5: Order inflow trend Exhibit 6: Order backlog

700 1,600 1,582

585

560 1,492

1,500

420 1,424

(Rs cr)

(Rs cr)

286 1,400 1,362

280 210

187 188

104 1,300

140 77 1,243

0 1,200

2QFY09

3QFY09

4QFY09

1QFY10

2QFY10

3QFY10

4QFY10

1QFY10

2QFY10

3QFY10

4QFY10

1QFY11

Source: Company, Angel Research Source: Company, Angel Research

Lower interest cost leads to higher PAT growth

Although EEC’s EBITDA margin for the quarter declined by 90bp to 15.3%, PAT

managed to grow by 57% to Rs13.4cr on account of lower interest outflow. Interest

outflow for the quarter decreased by 32% to Rs9.8cr (Rs14.4cr).

Exhibit 7: Declining interest outflow Exhibit 8: ...leads to higher PAT growth

16 30 80

14

13 25 60

11 12 20 40

12

(Rs cr)

10

(Rs cr)

15 20

(%)

10 0

8

5 (20)

0 (40)

4

1QFY10 2QFY10 3QFY10 4QFY10 1QFY11

1QFY10 2QFY10 3QFY10 4QFY10 1QFY11

PAT % YoY

Source: Company, Angel Research Source: Company, Angel Research

August 3, 2010 4

5. Elecon Engineering | 1QFY2011 Result Update

Investment arguments

Recovery augurs well for the MHE sector: The Rs5,700cr (FY2009) domestic MHE

industry has a strong correlation with industrial growth. According to the latest

data, IIP grew by an impressive 11.5% in May 2010, with the manufacturing sector

growing by 12.3%. Going ahead, we expect industrial capex to maintain its growth

path, with the economy reviving (indicated by the improvement in IIP), continued

government focus on infrastructure spends and pick-up in private capex.

Opportunity abound: The overall emerging opportunities in the MHE industry are

estimated to be around Rs32,500cr over FY2009–12E (Source: Crisil Research

Report). This augurs well for companies providing MHE solutions. Nonetheless,

near-term growth for MHE companies is expected to be driven by the high capex

likely to be incurred in the company’s key core sectors, such as power and coal.

Robust order book: EEC's current order book is pegged at Rs1,582cr (end of

1QFY2011), translating into 1.5x FY2010 revenue. The MHE segment is the

largest contributor to the company’s order book, with a share of Rs1,253cr,

followed by the gears segment, which accounts for Rs329cr of the order book.

We expect order inflows to gather pace in FY2011, which is evident from around

Rs600cr of order booking that the company registered in 1QFY2011. We estimate

EEC's order inflow to increase by a 40% CAGR over FY2010–12E.

Outlook and valuation

We have revised our estimates upwards to take into account the company’s robust

order book and higher-than-estimated capex for FY2011.

Exhibit 9: Change in estimates

Old New % chg

Parameters (Rs cr) FY11 FY12 FY11 FY12 FY11 FY12

Sales 1,201 1,358 1,255 1,431 5 5

EBITDA 179 208 188 219 5 5

EBITDA margin (%) 15 15 15 15

PAT 73 95 80 99 10 4

Source: Company, Angel Research

We believe an improving economic scenario (indicated by the revival in IIP),

continued government focus on infrastructure spends and pick-up in private capex

augur well for companies providing MHE solutions for the core sectors of the

economy. The government's strong focus on the power sector, through ’Power for

all by 2012’, is expected to result in an expansion of the sector’s generation

capacity, leading to higher opportunities for MHE players, while the mining and

port sectors would throw up combined opportunities worth around Rs7,000cr.

We believe EEC is well placed to seize the upcoming opportunities in the power

sector due its strong order book of Rs1,582cr at the end of 1QFY2011 (1.5x

FY2010 sales), which renders a high revenue visibility for the company.

August 3, 2010 5

6. Elecon Engineering | 1QFY2011 Result Update

We estimate the company's adjusted PAT to register a 22% CAGR over

FY2010–12E, driven by the stronger order inflow and a reduction in interest

outflow due to de-leveraging of the balance sheet on account of better working

capital management. We expect the RoCE and RoE to improve from 13% and 22%

in FY2010 to 19% and 23% in FY2012E, respectively.

At Rs92, the stock is available at attractive valuations of 8.6x FY2012E earnings

and 5.7x FY2012E EV/EBITDA. We maintain our Buy view on the stock with a

revised Target Price of Rs107 (Rs102).

Exhibit 10: Key assumption

Parameters (Rs cr) FY2011E FY2012E

Order backlog (Y/E) 1,171 1,321

Order inflow 1,172 1,569

% yoy 46 34

Sales 1,393 1,589

% yoy 26 14

Order book to sales (x) 0.8 0.8

Source: Company, Angel Research

Exhibit 11: One-year forward rolling P/E band

350

300

250

200

(Rs)

150

100

50

0

Apr-06

Jul-06

Apr-07

Jul-07

Apr-08

Jul-08

Apr-09

Jul-09

Apr-10

Jul-10

Oct-06

Oct-07

Oct-08

Oct-09

Jan-07

Jan-08

Jan-09

Jan-10

Price 5x 10x 15x 20x 25x

Source: C-line, Angel Research

August 3, 2010 6

11. Elecon Engineering | 1QFY2011 Result Update

Research Team Tel: 022 - 4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or

other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in

the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please

refer to the latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and

its affiliates may have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement Elecon Engineering

1. Analyst ownership of the stock No

2. Angel and its Group companies ownership of the stock No

3. Angel and its Group companies' Directors ownership of the stock No

4. Broking relationship with company covered No

Note: We have not considered any Exposure below Rs 1 lakh for Angel, its Group companies and Directors.

Ratings (Returns) : Buy (> 15%) Accumulate (5% to 15%) Neutral (-5 to 5%)

Reduce (-5% to 15%) Sell (< -15%)

August 3, 2010 11