1. 4QFY2010 Result Update I Real Estate

May 17, 2010

DLF NEUTRAL

CMP Rs287

Performance Highlights Target Price -

DLF reported 4QFY2010 results that were marginally below our expectations, Investment Period -

on account of higher interest and tax expenses. The DAL/Caraf merger and

purchase of Compulsorily Convertible Preference shares (CCPS), which were Stock Info

earlier issued by DAL to SC Asia (to the tune of Rs3,085cr), are set to increase

Sector Real Estate

the net debt level to 0.65-0.75x in 1QFY2011 from the current level of 0.53x.

The monetising from non-core assets was Rs1,800cr (much below initial Market Cap (Rs cr) 48,707

guidance) in FY2010, of which Rs566cr was reported in 4Q. The

Beta 1.8

management has given strong sales volume guidance of 15-18mn sq ft in

FY2011E. We believe that the stock’s performance hinges on recovery in the 52 WK High / Low 491/259

commercial segment, non-core assets sales and successful new launches,

which can hive off the high debt level. We recommend a Neutral on the stock. Avg. Daily Volume 3207926

Face Value (Rs) 2

Strong growth, albeit on low base: Revenues for 4QFY2010 grew by 77.7%

yoy to Rs1,994cr, driven by an improvement in volumes and pricing in the BSE Sensex 16,836

residential segment, albeit on a low base; however, they declined by 1.6% Nifty 5,060

qoq. Operating margins came in at 50.1%, higher by 851bp qoq and

3,637bp yoy, on account of revenue recognition from the Shivaji Road project Reuters Code DLFL.BO

in Delhi, where margins were in the mid-40s. Interest costs grew by 93.6% yoy

Bloomberg Code DLFU@IN

to Rs315cr, as a result of increased leverage due to the DLF-DAL integration.

The tax rate stood at 31.8% in 4QFY2010 (against 0% in 4QFY2009 and Shareholding Pattern (%)

26.6% in 3QFY2010). Consequently, the reported PAT came in at Rs426cr, up

by 168% yoy but down by 8.9% qoq. Promoters 78.6

MF/Banks/Indian FIs 2.3

Outlook and Valuation: We estimate DLF to sell 16.4mn sq ft in FY2011E, of FII/NRIs/OCBs 14.9

which 13mn sq ft is from the residential segment. In our view, there is a

limited upside to our launch estimates, considering the steep price rise in Indian Public 4.2

recent months. We have assumed a 5% reduction in commercial and retail Abs. (%) 3m 1yr 3yr

prices, but a 5% rise in residential prices, from current level, in FY2011E. DLF

has underperformed the Sensex over the last six months, on concerns of a Sensex 2.5 38.3 22.0

weak operating cash flow and increasing gearing levels. The stock is trading

at a 4% discount to our 1-year forward NAV of Rs298. Hence, we recommend DLF (6.1) 11.2 (49.7)*

a Neutral on the stock.

*Since listing on July 5, 2007

Key Financials (Consolidated)

Y/E March (Rs cr) FY2009 FY2010E FY2011E FY2012E

Net Sales 10,035 7,421 9,668 14,413

% chg (30.5) (26.1) 30.3 49.1

Net Profit 4,470 1,730 2,338 4,049

% chg (42.8) (61.3) 35.1 73.2

EBITDA Margin (%) 55.8 47.2 46.6 50.4

FDEPS (Rs) 26.2 10.2 13.8 23.9

P/E (x) 10.9 28.2 20.8 12.0

P/BV (x) 2.0 1.6 1.5 1.3

RoE (%) 19.9 6.2 7.2 11.5

RoCE (%) 14.6 6.7 7.4 11.7

Param Desai

EV/Sales (x) 6.4 9.4 7.1 4.8

Tel: 022 – 4040 3800 Ext: 310

EV/EBITDA (x) 11.4 19.8 15.2 9.4

E-mail: paramv.desai@angeltrade.com

Source: Company, Angel Research

1

Please refer to important disclosures at the end of this report Sebi Registration No: INB 010996539

2. DLF 4QFY2010 Result Update

Exhibit 1: 4QFY2010 Performance (Consolidated)

(Rs cr) 3QFY10 4QFY09 4QFY10 %yoy %qoq

Revenues 2,026 1,122 1,994 77.7 (1.6)

Total expenditure 1,183 968 994 2.8 (15.9)

EBIDTA 843 155 1,000 546.9 18.6

EBIDTA margin (%) 41.6 13.8 50.1 3,637bp 851bp

Depreciation 80 52 95 83.4 18.4

Interest 257 163 315 93.6 22.5

Other income 126 229 152 (33.8) 20.4

PBT 633 170 742 337.9 17.4

Tax 168 (0) 236 40.3

Tax rate (%) 26.6 (0.1) 31.8

Share of ass / Minority Int/ EO 4 (11) (80)

Adj PAT 464 170 506 198.3 9.1

PAT margin (%) 22.9 15.1 25.4 1026bp 247bp

Reported PAT 468 159 426 168.1 (8.9)

Reported EPS (Rs) 2.8 0.9 2.5

Source: Company, Angel Research

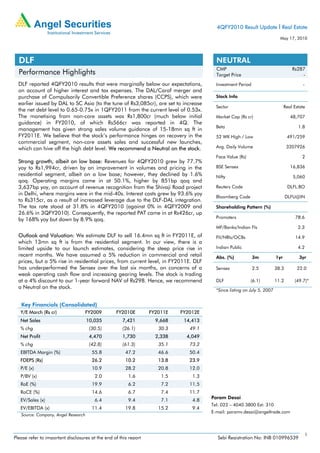

Deleveraging holds the key for the stock’s performance

The DAL/Caraf merger and purchase of Compulsorily Convertible Preference shares

(CCPS), which were earlier issued by DAL to SC Asia (to the tune of Rs3,085cr), are

set to increase the net debt level to 0.65-0.75x from the current level of 0.53x. This

will result in gross debt of ~Rs24,000cr by the end of 1QFY2011E. DLF repaid

Rs5,600cr debt in FY2010, against the mandatory debt payable of Rs3,550cr. Debt

repayments due in FY2011E are Rs26bn. DLF is targeting to reduce its net

debt/equity to 0.4-0.5x by the end of FY2011E. The reduction in the gearing level

will depend on hiving off non-core assets, successfully new launches, like the

Mumbai NTC mill, and a recovery in the commercial leasing segment.

Exhibit 2: Integration with DAL/Caraf led to higher Debt

17,000 0.58 0.60

0.48 0.53

15,000

0.48 0.49 0.50

13,000

(Rs cr)

(x)

11,000 0.40

9,000

0.30

7,000

5,000 0.20

4QFY09 1QFY10 2QFY10 3QFY10 4QFY10

Net Debt Net Debt: Equity

Source: Company, Angel Research

May 17, 2010 2

3. DLF 4QFY2010 Result Update

Update on Non-core assets

The monetising from non-core assets was Rs1800cr (much below the initial guidance

of Rs5,500cr in FY2010), of which Rs566cr was reported in 4Q. The management

has decided to retain its wind business, as it is getting 15% post-tax returns on these

assets. In FY2011E, the management has earmarked Rs2,700cr from the sale of

non-core assets, largely from Dwarka (Rs800cr) and TIDCO (Rs900cr).

Expects commercial demand to pick up over the next 12 months

DLF’s non-residential segment accounts for 55% of our GNAV. After the sharp

decline in the past few quarters, capital values have started to strengthen and have

registered marginal appreciation across most micro markets in the NCR. Industry

participants have indicated that the surge in leasing enquiries has come on the back

of a renewed interest from corporates. Recovery in the Commercial and Retail

Segments generally lag a recovery in the economy. Accordingly, we believe that

demand in office space will start picking up from 2HFY2011E onwards. Cushman

and Wakefield estimates pan-India cumulative demand for office space during

CY2009-13E to be 196mn sq ft. We expect a net employee addition of 15% in the

IT/ITES sector over FY2010-12E.

Rental visibility to improve after the merger of DLF-DAL/Caraf

DLF reported ~Rs750cr of rental income in FY2010. After the merger of DLF and

DAL/Caraf, the company has 19mn sq ft of rent-yielding assets, which will generate

Rs1,500-1,600cr of rental income in FY2011E. The company expects to list DAL by

the end of FY2011E, which can be value accretive for DLF shareholders at the lower

cap rate. However, this will depend on a recovery in the commercial leasing

segment.

Execution gradually picking up

DLF has 56 mn sq ft of projects under execution as of 4QFY2010 (compared to

51mn sq ft as of 3QFY2010), as it added 5.4mn sq ft comprising of homes and

commercial complexes in Capital Greens (2mn sq ft), SIEL (0.5mn sq ft) and 2.8mn

sq ft in Bangalore.

Exhibit 3: Projects under construction

60

56

55

51

49

50

(mn sqft)

45

42

40

36

35

30

25

4QFY09 1QFY10 2QFY10 3QFY10 4QFY10

Source: Company, Angel Research

May 17, 2010 3

4. DLF 4QFY2010 Result Update

Outlook and Valuation

DLF has a challenging task in FY2011E to bring down its gearing levels, for getting

fast approvals in order to have successful new launches and for monetizing its non-

core assets at a reasonable value. We estimate DLF to sell 16.4mn sq ft in FY2011E,

of which 13mn sq ft is from the residential segment. In our view, there is a limited

upside to our launch estimates, considering the steep price rise in recent months. We

have assumed a 5% reduction in commercial and retail prices, but a 5% rise in

residential prices, from the current level, in FY2011E. DLF has underperformed the

Sensex over the last six months, on concerns of a weak operating cash flow and

increasing gearing levels. The stock is trading at a 4% discount to our 1-year

forward NAV of 298. Hence, we recommend a Neutral on the stock.

Exhibit 4: Sales assumptions

25.0

22.6

21.8

20.0

16.4

15.0

(mn sqft)

12.4 12.5

10.0

5.0

0.0

FY08 FY09 FY10 FY11E FY12E

Source: Company, Angel Research

May 17, 2010 4

8. DLF 4QFY2010 Result Update

Research Team Tel: 022-4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment decision. Nothing in this

document should be construed as investment or financial advice. Each recipient of this document should make such investigations as they deem necessary to

arrive at an independent evaluation of an investment in the securities of the companies referred to in this document (including the merits and risks involved),

and should consult their own advisors to determine the merits and risks of such an investment.

Angel Securities Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make investment decisions that are

inconsistent with or contradictory to the recommendations expressed herein. The views contained in this document are those of the analyst, and the company

may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and trading volume, as

opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources believed to be true,

and are for general guidance only. Angel Securities Limited has not independently verified all the information contained within this document. Accordingly,

we cannot testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While Angel

Securities Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory, compliance, or other

reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced, redistributed or passed on,

directly or indirectly.

Angel Securities Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or other advisory services

in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in the past.

Neither Angel Securities Limited nor its directors, employees and affiliates shall be liable for any loss or damage that may arise from or in connection with the

use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section).

Disclosure of Interest Statement DLF

1. Analyst ownership of the stock No

2. Angel and its Group companies ownership of the stock Yes

3. Angel and its Group companies’ Directors ownership of the stock No

4. Broking relationship with company covered No

Note: We have not considered any Exposure below Rs 1 lakh for Angel and its Group companies.

Address: Acme Plaza, ‘A’ Wing, 3rd Floor, M.V. Road, Opp. Sangam Cinema, Andheri (E), Mumbai - 400 059.

Tel : (022) 3952 4568 / 4040 3800

Angel Broking Ltd: BSE Sebi Regn No : INB 010996539 / CDSL Regn No: IN - DP - CDSL - 234 - 2004 / PMS Regn Code: PM/INP000001546 Angel Securities Ltd:BSE: INB010994639/INF010994639 NSE:

INB230994635/INF230994635 Membership numbers: BSE 028/NSE:09946

Angel Capital & Debt Market Ltd: INB 231279838 / NSE FNO: INF 231279838 / NSE Member code -12798 Angel Commodities Broking (P) Ltd: MCX Member ID: 12685 / FMC Regn No: MCX / TCM /

CORP / 0037 NCDEX : Member ID 00220 / FMC Regn No: NCDEX / TCM / CORP / 0302

May 17, 2010 8