Kenya Coconut Production Presentation by Dr. Lalith Perera

Hindalco novelis ru4 qfy2010-280510

1. 4QFY2010 Result Update I Base Metals

May 28, 2010

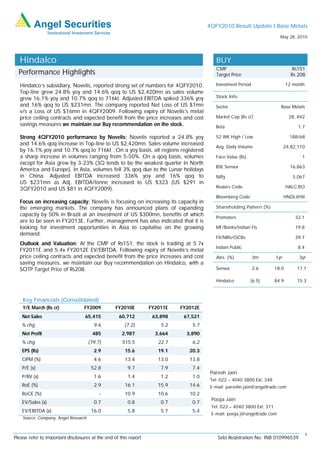

Hindalco BUY

CMP Rs151

Performance Highlights Target Price Rs 208

Hindalco’s subsidiary, Novelis, reported strong set of numbers for 4QFY2010. Investment Period 12 month

Top-line grew 24.8% yoy and 14.6% qoq to US $2,420mn as sales volume

grew 16.1% yoy and 10.7% qoq to 716kt. Adjusted EBITDA spiked 336% yoy Stock Info

and 16% qoq to US $231mn. The company reported Net Loss of US $1mn Sector Base Metals

v/s a Loss of US $16mn in 4QFY2009. Following expiry of Novelis’s metal

price ceiling contracts and expected benefit from the price increases and cost Market Cap (Rs cr) 28, 842

savings measures we maintain our Buy recommendation on the stock. Beta 1.7

Strong 4QFY2010 performance by Novelis: Novelis reported a 24.8% yoy 52 WK High / Low 188/68

and 14.6% qoq increase in Top-line to US $2,420mn. Sales volume increased

Avg. Daily Volume 24,82,110

by 16.1% yoy and 10.7% qoq to 716kt . On a yoy basis, all regions registered

a sharp increase in volumes ranging from 5-50%. On a qoq basis, volumes Face Value (Rs) 1

except for Asia grew by 3-23% (3Q tends to be the weakest quarter in North

BSE Sensex 16,863

America and Europe). In Asia, volumes fell 3% qoq due to the Lunar holidays

in China. Adjusted EBITDA increased 336% yoy and 16% qoq to Nifty 5,067

US $231mn as Adj. EBITDA/tonne increased to US $323 (US $291 in

3QFY2010 and US $81 in 4QFY2009). Reuters Code HALC.BO

Bloomberg Code HNDL@IN

Focus on increasing capacity: Novelis is focusing on increasing its capacity in

the emerging markets. The company has announced plans of expanding Shareholding Pattern (%)

capacity by 50% in Brazil at an investment of US $300mn, benefits of which

Promoters 32.1

are to be seen in FY2013E. Further, management has also indicated that it is

looking for investment opportunities in Asia to capitalise on the growing MF/Banks/Indian FIs 19.8

demand.

FII/NRIs/OCBs 39.7

Outlook and Valuation: At the CMP of Rs151, the stock is trading at 5.7x

Indian Public 8.4

FY2011E and 5.4x FY2012E EV/EBITDA. Following expiry of Novelis’s metal

price ceiling contracts and expected benefit from the price increases and cost Abs. (%) 3m 1yr 3yr

saving measures, we maintain our Buy recommendation on Hindalco, with a

SOTP Target Price of Rs208. Sensex 2.6 18.0 17.1

Hindalco (6.5) 84.9 15.3

Key Financials (Consolidated)

Y/E March (Rs cr) FY2009 FY2010E FY2011E FY2012E

Net Sales 65,415 60,712 63,898 67,521

% chg 9.6 (7.2) 5.2 5.7

Net Profit 485 2,987 3,664 3,890

% chg (79.7) 515.5 22.7 6.2

EPS (Rs) 2.9 15.6 19.1 20.3

OPM (%) 4.6 13.4 13.0 13.8

P/E (x) 52.8 9.7 7.9 7.4

Paresh Jain

P/BV (x) 1.6 1.4 1.2 1.0

Tel: 022 – 4040 3800 Ext: 348

RoE (%) 2.9 16.1 15.9 14.6 E-mail: pareshn.jain@angeltrade.com

RoCE (%) - 10.9 10.6 10.2

Pooja Jain

EV/Sales (x) 0.7 0.8 0.7 0.7

Tel: 022 – 4040 3800 Ext: 311

EV/EBITDA (x) 16.0 5.8 5.7 5.4

E-mail: pooja.j@angeltrade.com

Source: Company, Angel Research

1

Please refer to important disclosures at the end of this report Sebi Registration No: INB 010996539

2. Hindalco I 4QFY2010 Result Update

Exhibit 1: Novelis: 4QFY2010 Performance

(US $mn) 4QFY10 4QFY09 % yoy FY10 FY09 % yoy

Net Revenue 2,420 1,939 24.8 8,673 10,177 (14.8)

Cost of goods sold 2,141 1,606 33.3 7,190 9,251 (22.3)

(% of Net Sales) 88.5 82.8 82.9 90.9

Gross Profit 279 333 (16.2) 1,483 926 60.2

(% of Net Sales) 11.5 17.2 17.1 9.1

Selling and Administrative exp. 100 73 37.0 360 319 12.9

(% of Net Sales) 4.1 3.8 4.2 3.1

Research and Development expenses 11 8 37.5 38 41 (7.3)

(% of Net Sales) 0.5 0.4 0.4 0.4

EBITDA 168 252 (33.3) 1,085 566 91.7

EBITDA margin (%) 6.9 13.0 12.5 5.6

Restructuring charges 7 81 (91.4) 14 95 (85.3)

Depreciation 99 109 (9.2) 384 439 (12.5)

Other Income/(Expense) 4 (33) 25 (86)

EBIT 62 62 687 32

(% of Net Sales) 2.6 3.2 7.9 0.3

Net Interest expense 41 43 (4.7) 164 168 (2.4)

Unrealised Gain/(loss) on derivative 2 (40) 194 (556)

Exceptional items 0 122 0 (1,218)

Profit before tax 27 68 (60.3) 742 (1,996) -

(% of Net Sales) 1.1 3.5 8.6 (19.6)

Taxes 15 83 (81.9) 262 (246) -

(% of PBT) 55.6 122.1 35.3 12.3

PAT 12.0 (15.0) - 480 (1,750) -

(% of Net Sales) 0.5 (0.8) 5.5 (17.2)

Profit from Associates (3) (6) - (15) (172) -

Minority Interest (10) 5 - (60) 12 -

Net Income (1) (16) - 405 (1,910) -

Source: Company, Angel Research

Key Concall takeaways

Capacity utilisation is Asia and South America was more than 100%. While

Europe witnessed average utilisation rate of close to 100% (after closure of

Rogerstone plant which is being shifted to India), North America suffered from

over capacity. The company expects demand supply balance to be restored by

3QFY2011E.

FY2011E is likely to register volume growth of around 5% over FY2010E due to

debottlenecking.

The company incurred capex of US $101mn in FY2010. It proposes to increase

capex to US $250mn for FY2011E, with maintenance capex of

US $250mn

Novelis expects Adj. EBITDA to exceed US $1bn, though the time frame was not

specified.

May 28, 2010 2

3. Hindalco I 4QFY2010 Result Update

Exhibit 2: Shipments across geographies

(Kt) 4QFY2010 4QFY2009 % yoy 3QFY2010 % qoq

Total Sales 756 651 16.1 683 10.7

North America 282 256 10.2 254 11.0

Europe 250 219 14.2 204 22.5

Asia 130 87 49.4 134 (3.0)

South America 94 89 5.6 91 3.3

Source: Company, Angel Research

Exhibit 3: Average Realisation across geographies

(US $/tonne) 4QFY2010 4QFY2009 % yoy 3QFY2010 % qoq

Average Realisation 3,201 2,978 7.5 3,092 3.5

North America 3,252 3,273 (0.7) 3,094 5.1

Europe 3,400 3,059 11.1 3,554 (4.3)

Asia 3,100 2,575 20.4 2,910 6.5

South America 2,734 2,326 17.6 2,582 5.9

Source: Company, Angel Research

Outlook and Valuation

At the CMP of Rs151, the stock is trading at 5.7x FY2011E and 5.4x FY2012E

EV/EBITDA. Following expiry of Novelis’s metal price ceiling contracts and expected

benefit from the price increases and cost saving measures, we maintain our Buy

recommendation on Hindalco, with a SOTP Target Price of Rs208.

Exhibit 4: SOTP Valuation

FY2012E Multiple EV Stake Attributable Value

EBITDA (Rs cr) (x) (Rs cr) (%) EV (Rs cr) (Rs/share)

Hindalco (Standalone) 4,380 6.5 28,471 100 28,471 149

Novelis 4,945 5.5 27,196 100 27,196 142

Total EV 55,667 291

Less: Net Debt

18,380 95

(FY11E)

Value of Investments

2,280 12

@25% discount

Value per share 208

Source: Angel Research

Key risks to our call: 1) Significant movement in metal prices, 2) Adverse exchange

rate movements, and 3) Delay in completion of expansion projects.

May 28, 2010 3

9. Hindalco I 4QFY2010 Result Update

Research Team Tel: 022 - 4040 3800 E-mail: research@angeltrade.com Website: ww.angeltrade.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment decision. Nothing in this

document should be construed as investment or financial advice. Each recipient of this document should make such investigations as they deem necessary to

arrive at an independent evaluation of an investment in the securities of the companies referred to in this document (including the merits and risks involved),

and should consult their own advisors to determine the merits and risks of such an investment.

Angel Securities Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make investment decisions that are

inconsistent with or contradictory to the recommendations expressed herein. The views contained in this document are those of the analyst, and the company

may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and trading volume, as

opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources believed to be true,

and is for general guidance only. Angel Securities Limited has not independently verified all the information contained within this document. Accordingly, we

cannot testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While Angel

Securities Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory, compliance, or other

reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced, redistributed or passed on,

directly or indirectly.

Angel Securities Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or other advisory services

in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in the past.

Neither Angel Securities Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in connection with the

use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section).

Disclosure of Interest Statement Hindalco

1. Analyst ownership of the stock No

2. Angel and its Group companies ownership of the stock Yes

3. Angel and its Group companies’ Directors ownership of the stock No

4. Broking relationship with company covered No

Note: We have not considered any Exposure below Rs 1 lakh for Angel and its Group companies

Address: Acme Plaza, ‘A’ Wing, 3rd Floor, M.V. Road, Opp. Sangam Cinema, Andheri (E), Mumbai - 400 059.

Tel: (022) 3952 4568 / 4040 3800

Angel Broking Ltd: BSE Sebi Regn No : INB 010996539 / CDSL Regn No: IN - DP - CDSL - 234 - 2004 / PMS Regn Code: PM/INP000001546 Angel Securities Ltd:BSE: INB010994639/INF010994639 NSE:

INB230994635/INF230994635 Membership numbers: BSE 028/NSE:09946

Angel Capital & Debt Market Ltd: INB 231279838 / NSE FNO: INF 231279838 / NSE Member code -12798 Angel Commodities Broking (P) Ltd: MCX Member ID: 12685 / FMC Regn No: MCX / TCM /

CORP / 0037 NCDEX : Member ID 00220 / FMC Regn No: NCDEX / TCM / CORP / 0302

May 28, 2010 9