Call Girls In Connaught Place Delhi ❤️88604**77959_Russian 100% Genuine Escor...

Bhel ru4 qfy2010-280510

1. 4QFY2010 Result Update I Capital Goods

May 28, 2010

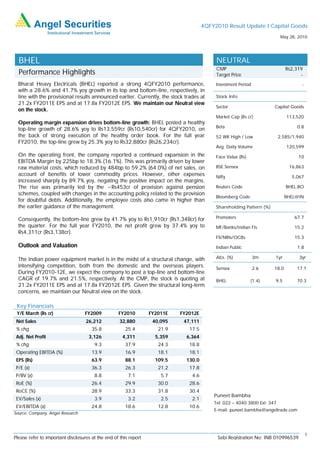

BHEL NEUTRAL

CMP Rs2,319

Performance Highlights Target Price -

Bharat Heavy Electricals (BHEL) reported a strong 4QFY2010 performance, Investment Period -

with a 28.6% and 41.7% yoy growth in its top and bottom-line, respectively, in

line with the provisional results announced earlier. Currently, the stock trades at Stock Info

21.2x FY2011E EPS and at 17.8x FY2012E EPS. We maintain our Neutral view

Sector Capital Goods

on the stock.

Market Cap (Rs cr) 113,520

Operating margin expansion drives bottom-line growth: BHEL posted a healthy

Beta 0.8

top-line growth of 28.6% yoy to Rs13,559cr (Rs10,540cr) for 4QFY2010, on

the back of strong execution of the healthy order book. For the full year 52 WK High / Low 2,585/1,940

FY2010, the top-line grew by 25.3% yoy to Rs32,880cr (Rs26,234cr).

Avg. Daily Volume 120,599

On the operating front, the company reported a continued expansion in the Face Value (Rs) 10

EBITDA Margin by 225bp to 18.3% (16.1%). This was primarily driven by lower

raw material costs, which reduced by 484bp to 59.2% (64.0%) of net sales, on BSE Sensex 16,863

account of benefits of lower commodity prices. However, other expenses Nifty 5,067

increased sharply by 89.7% yoy, negating the positive impact on the margins.

The rise was primarily led by the ~Rs453cr of provision against pension Reuters Code BHEL.BO

schemes, coupled with changes in the accounting policy related to the provision

Bloomberg Code BHEL@IN

for doubtful debts. Additionally, the employee costs also came in higher than

the earlier guidance of the management. Shareholding Pattern (%)

Consequently, the bottom-line grew by 41.7% yoy to Rs1,910cr (Rs1,348cr) for Promoters 67.7

the quarter. For the full year FY2010, the net profit grew by 37.4% yoy to MF/Banks/Indian FIs 15.2

Rs4,311cr (Rs3,138cr).

FII/NRIs/OCBs 15.3

Outlook and Valuation Indian Public 1.8

The Indian power equipment market is in the midst of a structural change, with Abs. (%) 3m 1yr 3yr

intensifying competition, both from the domestic and the overseas players. Sensex 2.6 18.0 17.1

During FY2010-12E, we expect the company to post a top-line and bottom-line

CAGR of 19.7% and 21.5%, respectively. At the CMP, the stock is quoting at BHEL (1.4) 9.5 70.3

21.2x FY2011E EPS and at 17.8x FY2012E EPS. Given the structural long-term

concerns, we maintain our Neutral view on the stock.

Key Financials

Y/E March (Rs cr) FY2009 FY2010 FY2011E FY2012E

Net Sales 26,212 32,880 40,095 47,111

% chg 35.8 25.4 21.9 17.5

Adj. Net Profit 3,126 4,311 5,359 6,364

% chg 9.3 37.9 24.3 18.8

Operating EBITDA (%) 13.9 16.9 18.1 18.1

EPS (Rs) 63.9 88.1 109.5 130.0

P/E (x) 36.3 26.3 21.2 17.8

P/BV (x) 8.8 7.1 5.7 4.6

RoE (%) 26.4 29.9 30.0 28.6

RoCE (%) 28.9 33.3 31.8 30.4

Puneet Bambha

EV/Sales (x) 3.9 3.2 2.5 2.1

Tel: 022 – 4040 3800 Ext: 347

EV/EBITDA (x) 24.8 18.6 12.8 10.6

E-mail: puneet.bambha@angeltrade.com

Source: Company, Angel Research

1

Please refer to important disclosures at the end of this report Sebi Registration No: INB 010996539

2. BHEL I 4QFY2010 Result Update

Segment-wise Performance

During the quarter, the power division was the key driver, registering a robust 29.6%

yoy top-line growth to Rs11,155cr (Rs8,608cr). On a positive note, the industry

division also picked up pace during the quarter, registering revenue growth of

15.9% yoy to Rs3,149cr (Rs2,716cr). Margins of both the divisions improved during

the quarter, with the power division margin increasing 731bp to 27.4% (20.1%),

and the industry division margin rising 404bp to 25.6% (21.5%).

Exhibit 1: Segment-wise Performance

Y/E March (Rs cr) 4QFY10 4QFY09 % chg FY10 FY09 % chg

Revenue

Power 11,155 8,608 29.6 26,861 21,344 25.8

Industry 3,149 2,716 15.9 7,879 7,250 8.7

Total Revenues 14,304 11,324 26.3 34,740 28,594 21.5

EBIT

Power 3,058 1,731 76.7 6,317 3,862 63.6

Industry 805 584 37.7 1,643 1,215 35.2

Total EBIT 3,863 2,315 66.9 7,960 5,076 56.8

Revenue Mix (%)

Power 78.0 76.0 77.3 74.6

Industry 22.0 24.0 22.7 25.4

EBIT Margin (%)

Power 27.4 20.1 23.5 18.1

Industry 25.6 21.5 20.8 16.8

Source: Company, Angel Research

Exhibit 2: 4QFY210 Performance

Y/E March (Rs cr) 4QFY10 4QFY09 % chg FY10 FY09 % chg

Net Sales 13,559 10,540 28.6 32,880 26,234 25.3

Raw Material 8,027 6,751 18.9 19,307 15,969 20.9

(% of Net Sales) 59.2 64.0 58.7 60.9

Employee Cost 1,743 1,408 23.9 5,153 4,113 25.3

(% of Net Sales) 12.9 13.4 15.7 15.7

Other Expenses 1,301 686 89.7 2,854 2,351 21.4

(% of Net Sales) 9.6 6.5 8.7 9.0

Total Expenditure 11,072 8,844 25.2 27,315 22,433 21.8

EBITDA 2,487 1,696 46.6 5,566 3,801 46.4

EBITDA (%) 18.3 16.1 16.9 14.5

Interest 18 8 119.8 34 31 9.1

Depreciation 165 101 63.4 458 334 37.0

Other Income 594 507 17.0 1,516 1,413 7.4

Profit before Tax 2,898 2,095 38.4 6,591 4,849 35.9

(% of Net Sales) 21.4 19.9 20.0 18.5

Total Tax 989 747 32.4 2,280 1,711 33.3

(% of PBT) 34.1 35.7 34.6 35.3

Reported PAT 1,910 1,348 41.7 4,311 3,138 37.4

(% of Net Sales) 14.1 12.8 13.1 12.0

Source: Company, Angel Research

May 28, 2010 2

3. BHEL I 4QFY2010 Result Update

Order Flows

The order inflows for 4QFY2010 grew by 45.1% yoy to Rs22,614cr (Rs15,580cr).

For the full year FY2010, the order inflows were flat at Rs59,031cr (Rs59,687cr). The

company expects order booking to maintain its momentum during the current

financial year as well, and has guided for inflows of Rs59,000-60,000cr. The order

backlog for the quarter increased 22.9% yoy and 7.3% qoq to Rs1,43,800cr.

Exhibit 3: Quarterly Order Inflow

25,000

22,614

20,000

15,580 16,000

14,500 14,500 15,107

15,000

(Rs cr)

12,400

10,000

8,017

5,000

0

Q109 Q209 Q309 Q409 Q110 Q210 Q310 Q410

Source: Company, Angel Research

Exhibit 4: Quarterly Order Backlog

160,000

143,800

140,000 134,000

124,403 125,800

113,584 117,000

120,000

104,000

100,000 95,000

(Rs cr)

80,000

60,000

40,000

20,000

0

Q109 Q209 Q309 Q409 Q110 Q210 Q310 Q410

Source: Company, Angel Research

May 28, 2010 3

4. BHEL I 4QFY2010 Result Update

Outlook and Valuation

The Indian power equipment market is in the midst of a structural change, with

intensifying competition, both from the domestic and the overseas players. During

FY2010-12E, we expect the company to post a top-line and bottom-line CAGR of

19.7% and 21.5%, respectively. At the CMP of Rs2,319, the stock is quoting at 21.2x

FY2011E EPS and at 17.8x FY2012E EPS. Given the structural long-term concerns,

we maintain our Neutral view on the stock.

Exhibit 5: 12-month Forward Rolling P/E Band

4,500

4,000 36x

3,500

28x

Sh are Price (Rs)

3,000

2,500

20x

2,000

1,500

12x

1,000

500

0

Apr-01

Oct-01

Apr-02

Oct-02

Apr-03

Oct-03

Apr-04

Oct-04

Apr-05

Oct-05

Apr-06

Oct-06

Apr-07

Oct-07

Apr-08

Oct-08

Apr-09

Oct-09

Apr-10

Source: C-line, Angel Research

Exhibit 6: BHEL - Premium/Discount to Sensex P/E

100%

80%

60%

40%

20%

0%

-20%

-40%

Oct-04

Oct-05

Oct-06

Oct-07

Oct-08

Oct-09

Apr-04

Apr-05

Apr-06

Apr-07

Apr-08

Apr-09

Apr-10

Source: C-line, Angel Research

May 28, 2010 4

8. BHEL I 4QFY2010 Result Update

Research Team Tel: 022- 4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment decision. Nothing in this

document should be construed as investment or financial advice. Each recipient of this document should make such investigations as they deem necessary to

arrive at an independent evaluation of an investment in the securities of the companies referred to in this document (including the merits and risks involved),

and should consult their own advisors to determine the merits and risks of such an investment.

Angel Securities Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make investment decisions that are

inconsistent with or contradictory to the recommendations expressed herein. The views contained in this document are those of the analyst, and the company

may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and trading volume, as

opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources believed to be true,

and are for general guidance only. Angel Securities Limited has not independently verified all the information contained within this document. Accordingly,

we cannot testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Securities Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory, compliance, or

other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced, redistributed or passed on,

directly or indirectly.

Angel Securities Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or other advisory services

in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in the past.

Neither Angel Securities Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in connection with the

use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section).

Disclosure of Interest Statement BHEL

1. Analyst ownership of the stock No

2. Angel and its Group companies ownership of the stock Yes

3. Angel and its Group companies’ Directors ownership of the stock No

4. Broking relationship with company covered No

Note: We have not considered any Exposure below Rs 1 lakh for Angel and its Group companies.

Address: Acme Plaza, ‘A’ Wing, 3rd Floor, M.V. Road, Opp. Sangam Cinema, Andheri (E), Mumbai - 400 059.

Tel : (022) 3952 4568 / 4040 3800

Angel Broking Ltd: BSE Sebi Regn No : INB 010996539 / CDSL Regn No: IN - DP - CDSL - 234 - 2004 / PMS Regn Code: PM/INP000001546 Angel Securities Ltd:BSE: INB010994639/INF010994639 NSE:

INB230994635/INF230994635 Membership numbers: BSE 028/NSE:09946

Angel Capital & Debt Market Ltd: INB 231279838 / NSE FNO: INF 231279838 / NSE Member code -12798 Angel Commodities Broking (P) Ltd: MCX Member ID: 12685 / FMC Regn No: MCX / TCM /

CORP / 0037 NCDEX : Member ID 00220 / FMC Regn No: NCDEX / TCM / CORP / 0302

May 28, 2010 8