Download to read offline

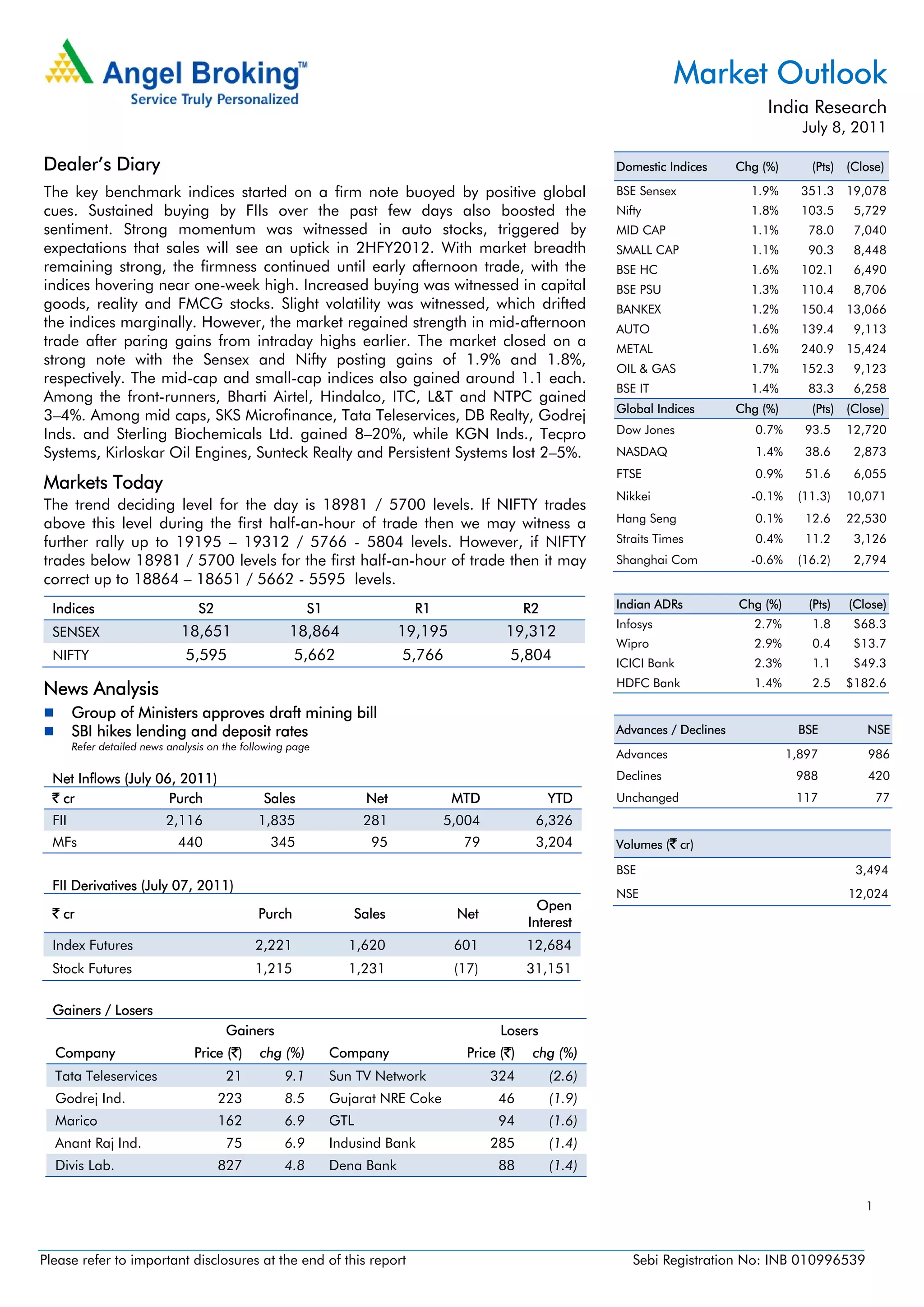

The key Indian indices gained around 1.8-1.9% boosted by positive global cues and sustained buying by foreign institutional investors. Auto and capital goods stocks witnessed strong buying, while mid and small cap indices also rose about 1.1% each. The market closed at one-week highs led by gains in Bharti Airtel, Hindalco, ITC and L&T.