1. 1QCY2010 Result Update I FMCG

April 23, 2010

GlaxoSmithKline Consumer Healthcare NEUTRAL

CMP Rs 1,561

Performance Highlights Target Price -

GSK Consumer registered a robust Top-line growth of 20.3% yoy to Rs648cr, Investment Period -

significantly above our estimates of a 14% yoy growth to Rs615cr, supported

by higher volumes and price increases. Bottom-line (on a reported basis) Stock Info

registered a growth of 14.6% yoy to Rs97cr, below our expectation of a 22.4% Sector FMCG

yoy growth to Rs103cr, largely due to Margin contraction and 7.7% drop in

Other Income (on account of shift to lower yield Fixed Income products). Post Market Cap (Rs cr) 6,640

the 1QCY2010 results, we have revised our Top-line estimates for GSK

Beta 0.3

Consumer marginally upwards by 1-2% to factor in higher revenue traction in

its new product launches. Due to rich valuations at which the stock is currently 52 WK High / Low 1,590/715

trading, we maintain a Neutral view on the stock.

Avg. Daily Volume 10,383

Robust Top-line; Margins under pressure despite higher Operating leverage: Face Value (Rs) 10

GSK Consumer registered a robust Top-line growth of 20.3% yoy to Rs648cr BSE Sensex 17,694

(Rs539cr) aided by a 13% Volume growth, 5% Value growth (price hikes) and

2% growth through lower Excise Duty. On the Operating front, the company Nifty 5,304

registered Margin contraction of 149bp yoy to 20.5% (22%). The company Reuters Code SMTH.BO

re-invested its savings from the 19bp expansion in Gross Margins (despite

inflationary pressures in milk, sugar and wheat owing to high base yoy) and Bloomberg Code SKB@IN

higher Operating leverage into higher Ad-spends, which increased 62.2%

Shareholding Pattern (%)

yoy. The Bottom-line (on a reported basis) registered a growth of 14.6% yoy to

Rs96cr (Rs84cr) positively driven by Top-line growth and various cost Promoters 43.2

rationalization initiatives undertaken by the company, partially offset by

MF/Banks/Indian FIs 30.1

higher-than-expected Ad-spends to support new launches by the company.

FII/NRIs/OCBs 9.8

Outlook and Valuation: We continue to like GSK Consumer for its sustained 16.9

Indian Public

Volume growth in its Core brands, higher contribution from new Product

launches coupled with potential higher Dividend payout due to high Cash Abs. (%) 3m 1yr 3yr

balance (Rs820cr as on December 2009). However, at the CMP of Rs1,561,

the stock is trading at rich valuations of 20.2x CY2011E EPS of Rs77.2, at a Sensex 4.9 58.9 27.0

significant premium to its historical valuations leaving little room for upside or

negative surprises. Hence, we maintain our Neutral recommendation on the GSKCHL 17.6 109.6 206.1

stock.

Key Financials

Y/E Dec (Rs cr) CY2008 CY2009 CY2010E CY2011E

Net Sales 1,542 1,922 2,279 2,667

% chg 20.6 24.6 18.6 17.0

Net Profit 190 230 274 325

% chg 16.8 21.2 19.0 18.5

OPM (%) 15.4 16.2 16.1 16.4

EPS (Rs) 45.2 55.3 65.1 77.2

P/E (x) 34.6 28.2 24.0 20.2 Anand Shah

P/BV (x) 8.6 7.3 6.1 5.2 Tel: 022 – 4040 3800 Ext: 334

E-mail: anand.shah@angeltrade.com

RoE (%) 27.0 27.9 27.7 27.8

RoCE (%) 27.3 32.4 32.9 33.4

Chitrangda Kapur

EV/Sales (x) 4.0 3.0 2.6 2.1

Tel: 022 – 4040 3800 Ext: 323

EV/EBITDA (x) 25.7 18.5 15.9 12.9 E-mail: chitrangda.kapur@angeltrade.com

Source: Company, Angel Research

1

Please refer to important disclosures at the end of this report Sebi Registration No: INB 010996539

2. GSK Consumer I 1QCY2010 Result Update

Exhibit 1: 1QCY2010 Performance

Y/E Dec (Rs cr) 1QCY10 1QCY09 % chg CY2009 CY2008 % chg

Net Sales 648.4 539.0 20.3 1,921.5 1,541.8 24.6

RM Cost 256.1 213.9 19.7 710.6 585.9 21.3

(% of Sales) 39.5 39.7 37.0 38.0

Staff Cost 51.6 49.8 3.8 200.7 172.0 16.7

(% of Sales) 8.0 9.2 10.4 11.2

Advertising 98.2 60.6 62.2 302.1 194.0 55.7

(% of Sales) 15.2 11.2 15.7 12.6

Other Exp. 109.4 96.1 13.9 397.3 352.4 12.7

(% of Sales) 16.9 17.8 20.7 22.9

Total Exp. 515.4 420.3 22.6 1,610.7 1,304.2 23.5

Operating Profit 133.1 118.6 12.1 310.8 237.5 30.9

OPM (%) 20.5 22.0 16.2 15.4

Interest 0.6 1.2 (52.5) 4.2 5.3 (22.3)

Depreciation 9.6 10.6 (9.8) 42.0 42.0 0.2

Other Income 23.6 25.5 (7.7) 89.3 95.5 (6.5)

PBT(excl Ext. Items) 146.5 132.4 10.7 354.0 285.7 23.9

Extr Income/(Exp.) - - - -

PBT(incl Ext. Items) 146.5 132.4 10.7 354.0 285.7 23.9

(% of Sales) 22.6 24.6 18.4 18.5

Prov. for Taxation 50.3 48.5 3.8 121.1 97.4 24.3

(% of PBT) 34.4 36.6 34.2 34.1

Reported PAT 96.2 83.9 14.6 232.9 188.3 23.7

PATM (%) 14.8 15.6 12.1 12.2

Equity Shares (cr) 4.2 4.2 4.2 4.2

EPS (Rs) 22.8 19.9 14.6 55.3 44.7 23.7

Source: Company, Angel Research

New launches boost Top-line growth to 20.3% beating estimates: GSK Consumer

posted a robust growth of 20.3% yoy in Top-line to Rs648cr (Rs539cr) beating our

estimates of 14% yoy growth to Rs615cr, led by a 13% Volume growth, 5% Value

growth (price hikes) and 2% growth through lower Excise duty. While its core brands

Horlicks and Boost registered healthy Volume growths of 11% yoy and 21% yoy

respectively, we believe, the higher-than-anticipated growth in Top-line was on

account of improved traction in new launches (Women’s Horlicks, Horlicks Nutribar,

Actibase, Actigrow and Horlicks Foodles).

Re-investment in Ad-spend drags Margins, contract 149bp yoy: GSK Consumer

registered Margin contraction of 149bp yoy to 20.5% (22%) resulting in muted

EBITDA growth of 12.1% yoy to Rs133cr (Rs119cr). The company re-invested 19bp

expansion in Gross Margins (despite inflationary pressures in milk, sugar and wheat

owing to high base yoy) and higher Operating leverage (Staff costs down by 126bp

and overheads down by 99bp yoy) into higher Ad-spends, which increased 62.2%

yoy and 14.5% qoq on account of new product launches (entry into Noodles

Segment). According to management, Liquid Milk price increased by around 15%

yoy and 7-8% qoq, while Powder Milk price increased by around 7% yoy and

4-5% qoq for the quarter. While sugar prices have corrected by around 30% during

the quarter, we believe input cost inflation, particularly agri-commodities, remains a

challenge.

Bottom-line growth at 14.6% yoy, below estimates: Bottom-line for the quarter

registered a growth of 14.6% yoy to Rs96cr (Rs84cr), below our expectation of a

22.4% growth to Rs103cr, largely due to Margin contraction and 7.7% drop in Other

Income (on account of shift to lower yield Fixed Income products).

April 23, 2010 2

3. GSK Consumer I 1QCY2010 Result Update

Outlook and Valuation

Post the 1QCY2010 result we have marginally tweaked our numbers to factor in the

higher-than-anticipated Top-line growth of 20.3% (14%) yoy and the company’s

higher Ad-spend. Our Top-line estimates have been revised upward by 1-2% owing

to increased revenue traction in its new launches. Earnings estimates are revised

upwards by 1.2% to factor in higher Top-line growth and various cost rationalization

initiatives undertaken by the company since CY2009. However, Operating Margins

are likely to be under pressure yoy owing to the company’s heavy brand investments.

Exhibit 2: Revision in Estimates

Old Estimate New Estimate % chg

(Rs cr) CY10E CY11E CY10E CY11E CY10E CY11E

Revenue 2,254 2,611 2,279 2,667 1.1 2.2

OPM (%) 15.9 16.3 16.1 16.4 17bp 9bp

EPS 64.4 76.3 65.1 77.2 1.2 1.2

Source: Angel Research

We continue to like GSK Consumer for its sustained Volume growth in its Core

brands, higher contribution from new Product launches and potential higher

Dividend payout due to high Cash balance (Rs820cr as on December 2009).

However, at the CMP of Rs1,561, the stock is trading at rich valuations of 20.2x

CY2011E EPS of Rs77.2, at a significant premium to its historical valuations leaving

little room for upside or negative surprises. Hence, we maintain our Neutral view on

the stock.

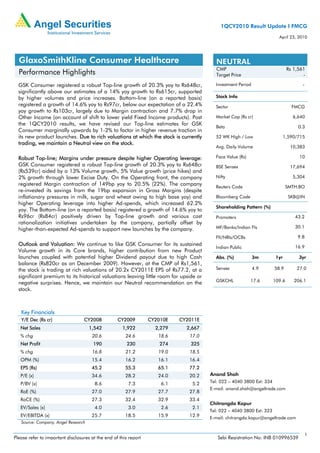

Exhibit 3: 1-year forward P/E band

1,800 12x 15x 18x 21x

1,600

1,400

1,200

Share Price (Rs)

1,000

800

600

400

200

-

Dec-05

Dec-06

Dec-07

Dec-08

Dec-09

Apr-05

Apr-06

Apr-07

Apr-08

Apr-09

Apr-10

Oct-05

Oct-06

Oct-07

Oct-08

Oct-09

Aug-05

Feb-06

Aug-06

Feb-07

Aug-07

Feb-08

Aug-08

Feb-09

Aug-09

Feb-10

Jun-05

Jun-06

Jun-07

Jun-08

Jun-09

Source: Bloomberg, Angel Research

April 23, 2010 3

8. GSK Consumer I 1QCY2010 Result Update

Research Team Tel: 4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment decision. Nothing in this

document should be construed as investment or financial advice. Each recipient of this document should make such investigations as they deem necessary to

arrive at an independent evaluation of an investment in the securities of the companies referred to in this document (including the merits and risks involved),

and should consult their own advisors to determine the merits and risks of such an investment.

Angel Securities Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make investment decisions that are

inconsistent with or contradictory to the recommendations expressed herein. The views contained in this document are those of the analyst, and the company

may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and trading volume, as

opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable source believed to be true,

and is for general guidance only. Angel Securities Limited has not independently verified all the information contained within this document. Accordingly, we

cannot testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While Angel

Securities Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory, compliance, or other

reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced, redistributed or passed on,

directly or indirectly.

Angel Securities Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or other advisory services

in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in the past.

Neither Angel Securities Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in connection with the

use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section).

Disclosure of Interest Statement GSKCHL

1. Analyst ownership of the stock No

2. Angel and its Group companies ownership of the stock No

3. Angel and its Group companies’ Directors ownership of the stock No

4. Broking relationship with company covered No

Note: We have not considered any Exposure below Rs 1 lakh for Angel and its Group companies.

Address: Acme Plaza, ‘A’ Wing, 3rd Floor, M.V. Road, Opp. Sangam Cinema, Andheri (E), Mumbai - 400 059.

Tel : (022) 3952 4568 / 4040 3800

Angel Broking Ltd: BSE Sebi Regn No : INB 010996539 / CDSL Regn No: IN - DP - CDSL - 234 - 2004 / PMS Regn Code: PM/INP000001546 Angel Securities Ltd:BSE: INB010994639/INF010994639 NSE:

INB230994635/INF230994635 Membership numbers: BSE 028/NSE:09946

Angel Capital & Debt Market Ltd: INB 231279838 / NSE FNO: INF 231279838 / NSE Member code -12798 Angel Commodities Broking (P) Ltd: MCX Member ID: 12685 / FMC Regn No: MCX / TCM /

CORP / 0037 NCDEX : Member ID 00220 / FMC Regn No: NCDEX / TCM / CORP / 0302

April 23, 2010 8