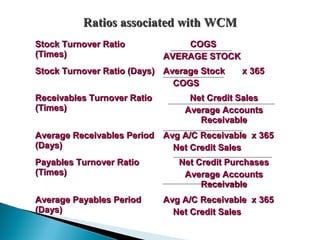

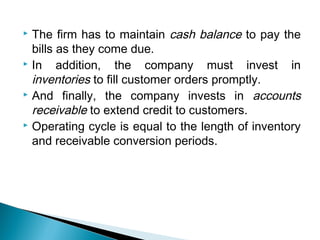

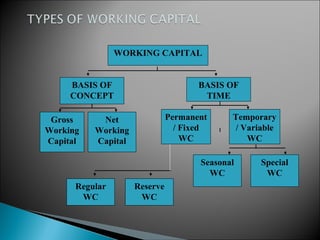

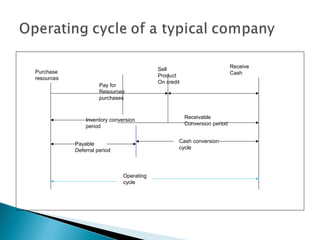

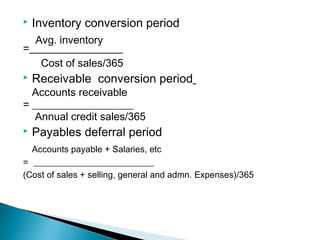

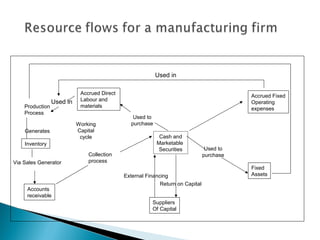

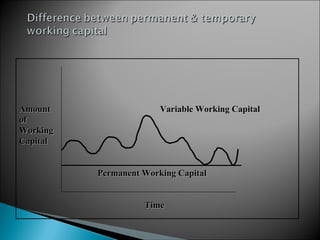

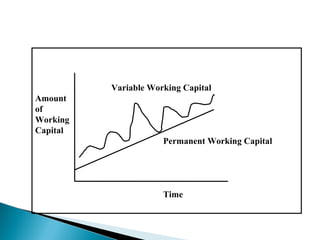

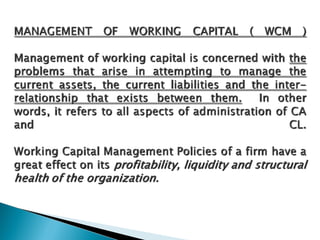

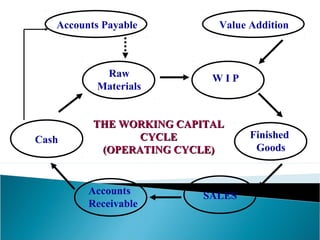

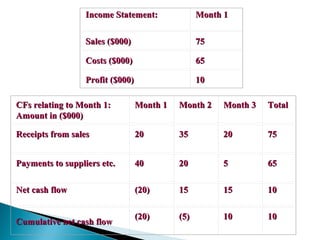

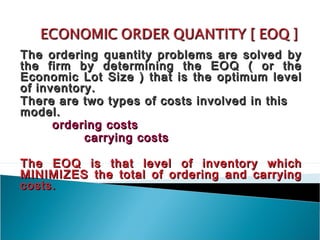

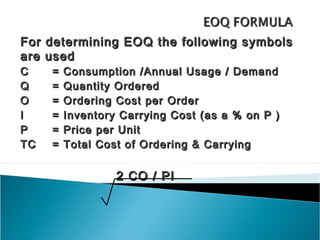

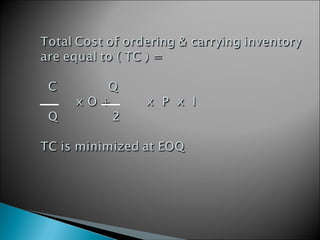

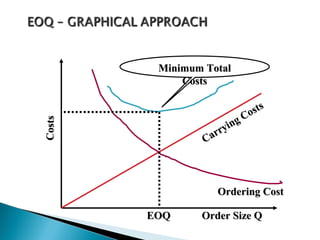

The document discusses the concept of working capital, which refers to a company's short-term assets and liabilities. It presents two definitions of working capital: the balance sheet concept, which is the excess of current assets over current liabilities, and the operating cycle concept, which refers to the time period between purchasing inventory and collecting cash from sales. The document outlines the key components of a company's operating cycle and how managing working capital, including inventory levels, accounts receivable, and accounts payable, can impact cash flows and the business.

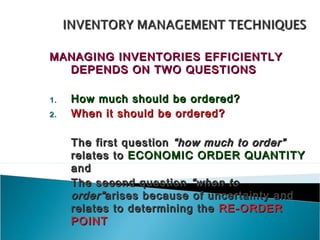

![Classification Basis

ABC Value of items consumed

[Always Better Control ]

VED The importance or

[ Vital, Essential, criticality

Desirable ]

FSN The pace at which the

[ Fast-moving, Slow- material moves

moving, Non-moving ]

HML Unit price of materials

[ High, Medium, Low ]

SDE Procurement Difficulties

[ Scarce, Difficult, Easy ]](https://image.slidesharecdn.com/workingcapital27022013-130306102202-phpapp02/85/Working-capital-66-320.jpg)