This presentation covers Merchant Banking History; Categories; Services provided by them; Methods of placement; underwriting; Issue management & SEBI guidelines.

Hey, Do you want to know something about Debt or Equity? Then just one click on Link is given in PPT and you will get import information on it which will help you. So, Do just One Click on Link.....

This presentation covers Merchant Banking History; Categories; Services provided by them; Methods of placement; underwriting; Issue management & SEBI guidelines.

Hey, Do you want to know something about Debt or Equity? Then just one click on Link is given in PPT and you will get import information on it which will help you. So, Do just One Click on Link.....

This ppt is covering lease finance in detail, covering advantages & disadvantages. Types of lease. Instead of doing hard work rely on smart work. Time you devote on copy pasting. Channelize that time in understanding topic via reading it.

Leasing and hire purchase are both financial arrangements.Sonam704174

Leasing and hire purchase are both financial arrangements for acquiring assets. Leasing involves renting an asset for a specified period, while hire purchase allows the buyer to use the asset during the payment period with ownership transferring after the final installment.

Synthetic Fiber Construction in lab .pptxPavel ( NSTU)

Synthetic fiber production is a fascinating and complex field that blends chemistry, engineering, and environmental science. By understanding these aspects, students can gain a comprehensive view of synthetic fiber production, its impact on society and the environment, and the potential for future innovations. Synthetic fibers play a crucial role in modern society, impacting various aspects of daily life, industry, and the environment. ynthetic fibers are integral to modern life, offering a range of benefits from cost-effectiveness and versatility to innovative applications and performance characteristics. While they pose environmental challenges, ongoing research and development aim to create more sustainable and eco-friendly alternatives. Understanding the importance of synthetic fibers helps in appreciating their role in the economy, industry, and daily life, while also emphasizing the need for sustainable practices and innovation.

Operation “Blue Star” is the only event in the history of Independent India where the state went into war with its own people. Even after about 40 years it is not clear if it was culmination of states anger over people of the region, a political game of power or start of dictatorial chapter in the democratic setup.

The people of Punjab felt alienated from main stream due to denial of their just demands during a long democratic struggle since independence. As it happen all over the word, it led to militant struggle with great loss of lives of military, police and civilian personnel. Killing of Indira Gandhi and massacre of innocent Sikhs in Delhi and other India cities was also associated with this movement.

We all have good and bad thoughts from time to time and situation to situation. We are bombarded daily with spiraling thoughts(both negative and positive) creating all-consuming feel , making us difficult to manage with associated suffering. Good thoughts are like our Mob Signal (Positive thought) amidst noise(negative thought) in the atmosphere. Negative thoughts like noise outweigh positive thoughts. These thoughts often create unwanted confusion, trouble, stress and frustration in our mind as well as chaos in our physical world. Negative thoughts are also known as “distorted thinking”.

How to Make a Field invisible in Odoo 17Celine George

It is possible to hide or invisible some fields in odoo. Commonly using “invisible” attribute in the field definition to invisible the fields. This slide will show how to make a field invisible in odoo 17.

The French Revolution, which began in 1789, was a period of radical social and political upheaval in France. It marked the decline of absolute monarchies, the rise of secular and democratic republics, and the eventual rise of Napoleon Bonaparte. This revolutionary period is crucial in understanding the transition from feudalism to modernity in Europe.

For more information, visit-www.vavaclasses.com

2. MEANING

Mrs.S.Kirubadevi,M.Com., M.Phil., PGDCA.,

Assistant Professor2

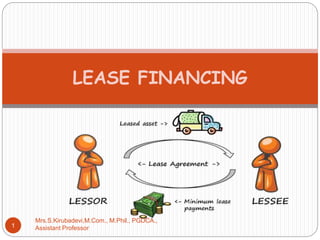

Leasing- financing concept – is an arrangement

between two parties, - (the leasing co. or lessor)

and (the user or lessee), whereby the former

arranges to buy capital equipment for the use of

the latter for an agreed period of time in return

for rent.

The rentals – predetermined – payable at fixed

intervals of time, according to mutual

convenience of both the parties.

However, Lessor remains the owner of the

equipment over the primary period

3. Definition:

Mrs.S.Kirubadevi,M.Com., M.Phil., PGDCA.,

Assistant Professor3

Leasing is a contract , where by

The owner (Lessor) of the Asset(Equipment)

Transfers the possession / right to use the Asset(Equipment)

to another party (Lessee) usually

For an agreed period of time in return for the payment of

rent.

-James C. Van Home

4. Essential Elements of Leasing

Mrs.S.Kirubadevi,M.Com., M.Phil., PGDCA.,

Assistant Professor4

Parties to a Lease Contract: Essentially two parties

Lessor – is the owner of the asset that is being Leased.

Lessee – is the receiver of the services of the asset under a

Lease contract.

Lessor and Lessee can be Individual or legally recognized party.

The lessor is either the asset’s manufacturer or an independent leasing

company

Lease broker – big ticket Leases use him.

Major Players in Lease Market:

Banks- Indian & Foreign /FIs

subsidiaries of Banks/FIs,

NBFCs

5. Essential Elements of Leasing

Mrs.S.Kirubadevi,M.Com., M.Phil., PGDCA.,

Assistant Professor5

Asset – Subject matter of Leasing contract; Automobiles,

Plant & Machinery, Equipments, Land & building, Factory,

a running business, aircraft, Ships, etc.

Ownership – remains with the Lessor

Use - of the asset is allowed to the Lessee.

Lease Term – Primary /secondary Lease Term.

Lease Rentals – is the consideration for the lease

transaction. So structured to recover the investment cost,

during agreed period.

7. TYPES OF LEASING

Mrs.S.Kirubadevi,M.Com., M.Phil., PGDCA.,

Assistant Professor7

Finance Lease and Operating Lease

Sale & Lease back and Direct Lease

Single Investor Lease and Leveraged Lease

Domestic Lease and International Lease

9. Finance Lease

Mrs.S.Kirubadevi,M.Com., M.Phil., PGDCA.,

Assistant Professor

9

Long-term, non-cancellable lease contracts are known

as financial leases.

To record a lease as a capital lease, the lease must be

noncancelable.

One or more of four criteria must be met:

1. Transfers ownership to the lessee.

2. Contains a bargain-purchase option.

3. Lease term is equal to or greater than 75 percent of the estimated

economic life of the leased property.

4. The present value of the minimum lease payments (excluding

executor costs) equals or exceeds 90 percent of the fair value of the

leased property.

10. Features of Financial Service

Mrs.S.Kirubadevi,M.Com., M.Phil., PGDCA.,

Assistant Professor10

A Financial Lease is structured to include:

The Lessee selects the equipment meeting his requirement

The Lessee negotiates the price, delivery schedule,

installation, warranties, maintenance, etc.

The Lessee informs the above details and Lessor makes the

payment directly to the Seller(manufacturer /distributor).

The equipment is directly delivered to the Lessee by seller.

The Lessee enjoys exclusive and peaceful possession and

use of the equipment.

Enters in to the Lease agreement with Lessor.

The Lessor pays the amount directly to

Seller(Manufacturer/supplier).

11. Operating Lease

Mrs.S.Kirubadevi,M.Com., M.Phil., PGDCA.,

Assistant Professor11

Characteristics of an Operating Lease:

also known as service lease, short-term lease or true

lease.

The Lease term is significantly less than the economic

life of the equipment.

The Lessee enjoys the right to terminate the Lease at

short notice without any significant penalty.

The Lessor usually provides the operating know-how,

suppliers related service, and undertakes the

responsibility of insuring and maintaining (repair and

technical service) the equipment

12. Differentiation Between Operating lease and Financial lease

Mrs.S.Kirubadevi,M.Com., M.Phil., PGDCA.,

Assistant Professor

12

BASIS FinancialLease Operating leasE

Meaning Long-term, non-cancellable lease

contracts are known as financial

leases.

A Lease which is a short term one

and one which does not cover the

useful life on an asset is called an

operating lease.

Form In this type of lease, money is

provide by lessor and the asset is

purchase form outside

The lessor is carrying on business

of leasing and he holds such

assets or is a manufacturer of such

asset leases its asset

Maintenance The lessee undertakes the

maintenance of the asset, paying

insurance premium ect.

In this type of lease, repairs and

maintenance is done by the lessor.

Risk of

Obsolescence

In this types of lease, the lessee

bears the risk obsolescence, so far

as he uses the asset.

In this types of lease, the lessor

bears the risk obsolescence

during the period of the lease.

13. Mrs.S.Kirubadevi,M.Com., M.Phil., PGDCA.,

Assistant Professor13

BASIS FinancialLease Operating leas

Period of

Lease

Period of lease – whole useful

life of asset.

Period of lease – for shot time.

Option to Buy Option to buy for lessee. Period of lease – for shot time.

Accounting

Entries

According to the international

accounting standard-17, an

entery iis made in the balance

sheet of the lessee on both the

side

No entry is made in the balance

sheet of the lassee under this type

of lease, because lease is in the

form of a hired asset

14. Sale and Lease back

Mrs.S.Kirubadevi,M.Com., M.Phil., PGDCA.,

Assistant Professor14

Sale and Lease back:

The owner(Lessee) of the equipment sells it to a Leasing

company (Lessor).

The Lessor, leases the equipment back to the Lessee.

Under this arrangement, the assets are not physically

exchanged but it all happens in records only.

The seller assumes the role of a lessee and the buyer

assumes the role of a lessor.

The seller gets the agreed selling price and the buyer gets

the lease rentals.

Two sets of cash flows occur:

The lessee receives cash today from the sale.

The lessee agrees to make periodic lease payments,

thereby retaining the use of the asset.

16. Direct Lease

Mrs.S.Kirubadevi,M.Com., M.Phil., PGDCA.,

Assistant Professor16

Under direct leasing, a firm acquires the right to use an

asset from the manufacturer directly.

The ownership of the asset leased out remains with the

manufacturer itself.

Bipartite Lease – Equipment supplier-cum-Lessor and

Lessee.

Tripartite Lease (Sales-aid-Lease) – Equipment supplier,

Lessor and Lessee.

17. Single Investor Lease

Mrs.S.Kirubadevi,M.Com., M.Phil., PGDCA.,

Assistant Professor17

• Only two parties – Lessor and Lessee.

• Leasing company (Lessor) funds the entire investment,

having appropriate mix of Equity-cum-Debt.

• Finance raised by the Lessor, is without recourse to the

Lessee.

18. Leveraged Lease

Mrs.S.Kirubadevi,M.Com., M.Phil., PGDCA.,

Assistant Professor18

Leveraged Lease:

3 parties to the transaction.

Lessor ( Equity investor)

Lender

Lessee.

The Leasing company (Equity investor)

buys the equipment, through substantial borrowing, and

with full recourse to the Lessee and without recourse to it.

The Lender obtains an assignment of the Lease and a first

mortgage of the equipment.

20. Domestic Lease and International Lease

20

When a lease agreement is made between citizen of same

countries, it is called Domestic lease

When a lease agreement is made between citizen of

different countries, it is called International lease

Mrs.S.Kirubadevi,M.Com., M.Phil., PGDCA.,

Assistant Professor

21. Advantages of Leasing

21

Provides full Finance

Flexible

Saves from Recurring cost of finance

Absence of restrictions

Tax Benefits

Increases the capacity to borrow

Useful in case of fast changing technology

Faster and Cheaper credit

Mrs.S.Kirubadevi,M.Com., M.Phil., PGDCA.,

Assistant Professor

22. Limitations of Leasing

Mrs.S.Kirubadevi,M.Com., M.Phil., PGDCA.,

Assistant Professor22

No Benefit of Residual Value

High cost of leaseing

No benefit of ownership

Not Flexible

Disputes

23. Factors affecting Leasing Decisions

Mrs.S.Kirubadevi,M.Com., M.Phil., PGDCA.,

Assistant Professor23

Availability of cash

Effect on Borrowing Capacity

Shifting the Risk of Obsolescence

Convenient Arrangement

Less Restrictions on Firm

Salvage Value

Tax Benefits

Leas Expenses

24. Institutions In the field of Leaseing

Mrs.S.Kirubadevi,M.Com., M.Phil., PGDCA.,

Assistant Professor24

All India Financial Institutions

Leasing Companies

Banks

Financial Companies

Industrial Groups having Leasing Companies

25. Difficulties Faced by Leasing Companies in India

Mrs.S.Kirubadevi,M.Com., M.Phil., PGDCA.,

Assistant Professor25

Competition

Lack of Trained Employees

Proportion of Debt-Equity not maintained

Lack of Provision for Depreciation

Low Investment of Promoters

Shortage of Funds

Inefficiency of Management

Government Attitude

26. LEASING IN INDIA

Mrs.S.Kirubadevi,M.Com., M.Phil., PGDCA.,

Assistant Professor26

Leasing has grown by leaps and bounds in the eighties but

it is estimated that hardly 1% of the industrial investment in

India is covered by the lease finance, as against 40% in

USA and 30% in UK and 10% in Japan.

27. DIFFERENCE BETWEEN LEASE FINANCING

AND HIRE PURCHASE

BASIS LEASE FINANCING HIRE PURCHASE

Meaning A lease transaction is a

commercial arrangement,

whereby an equipment

owner or manufacturer conveys

to the equipment user the right

to use the

equipment in return for a rental.

Hire purchase is a type of

instalment credit under which

the hire purchaser agrees to

take the goods on hire at a

stated rental, which is inclusive

of the repayment of principal as

well as interest, with an option to

purchase.

Option to

user

No option is provided to the

lessee (user) to purchase the

goods.

Option is provided to the hirer

(user).

Nature of

expenditur

e

Lease rentals paid by the

lessee are entirely revenue

expenditure of the lessee.

Only interest element included

in the HP instalments is revenue

expenditure by nature.

Componen

ts

Lease rentals comprise of 2

elements (1) finance charge

and (2) capital

HP instalments comprise of 3

elements (1) normal trading

profit (2) finance

Mrs.S.Kirubadevi,M.Com., M.Phil., PGDCA.,

Assistant Professor27