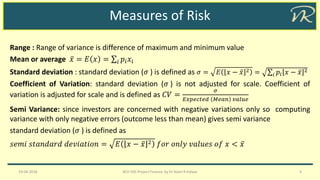

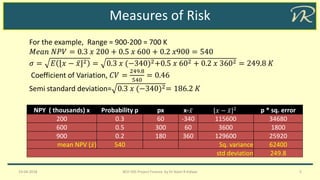

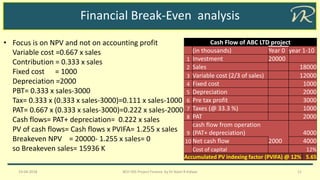

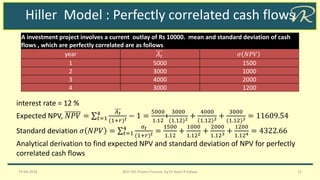

The document discusses various techniques for risk analysis in project finance, including sensitivity analysis, scenario analysis, break-even analysis, and simulation analysis. It defines key risk analysis terms and provides examples of calculating expected net present value and standard deviation of NPV using the Hiller model under both uncorrelated and perfectly correlated cash flows. Simulation analysis involves modeling the relationship between variable factors and NPV, specifying probability distributions, running simulations to obtain multiple NPV outcomes, and analyzing the results. Project selection under risk may involve judgmental evaluation, payback period requirements, or risk-adjusted discount rates.