Downloaded 6,593 times

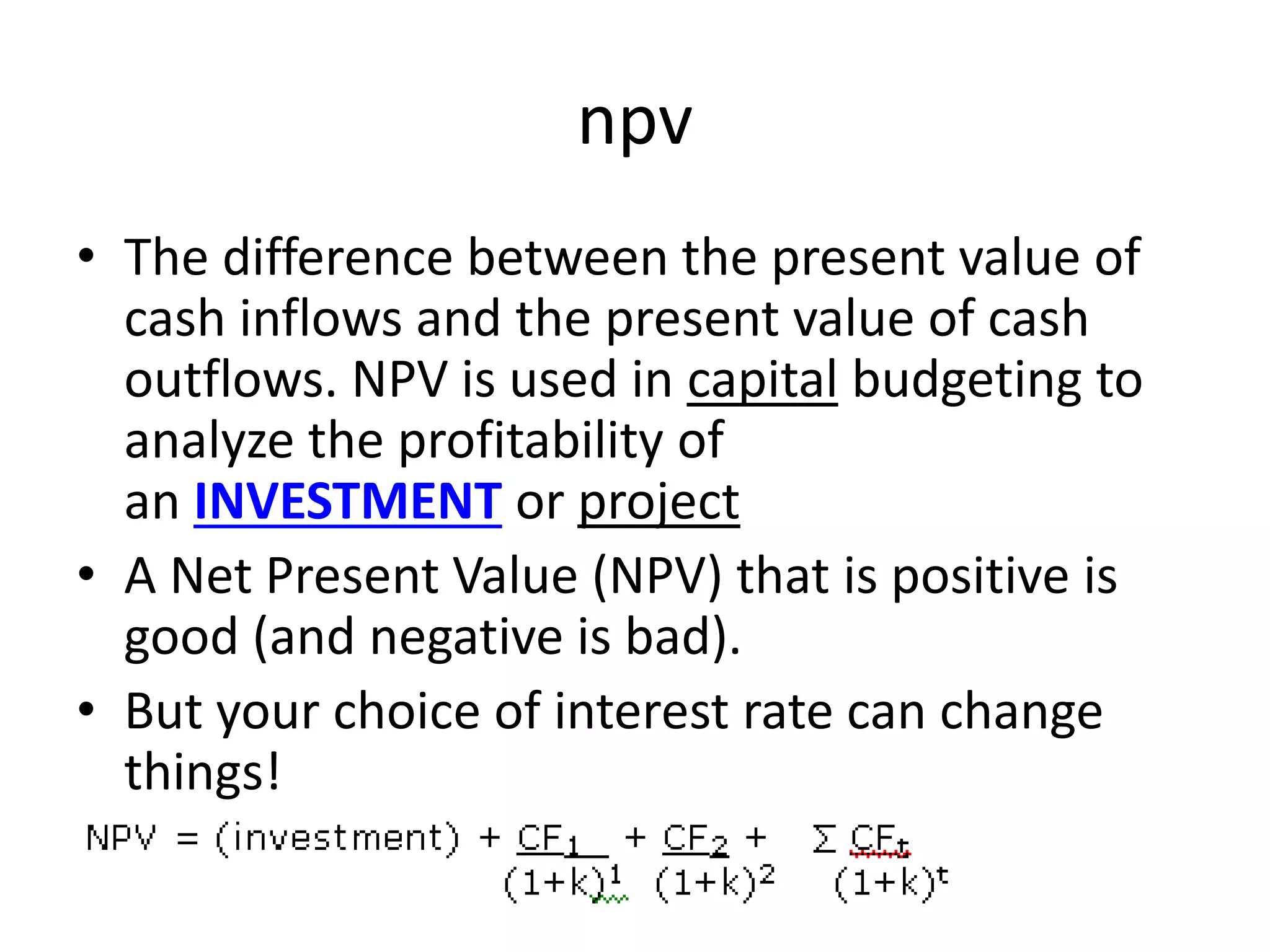

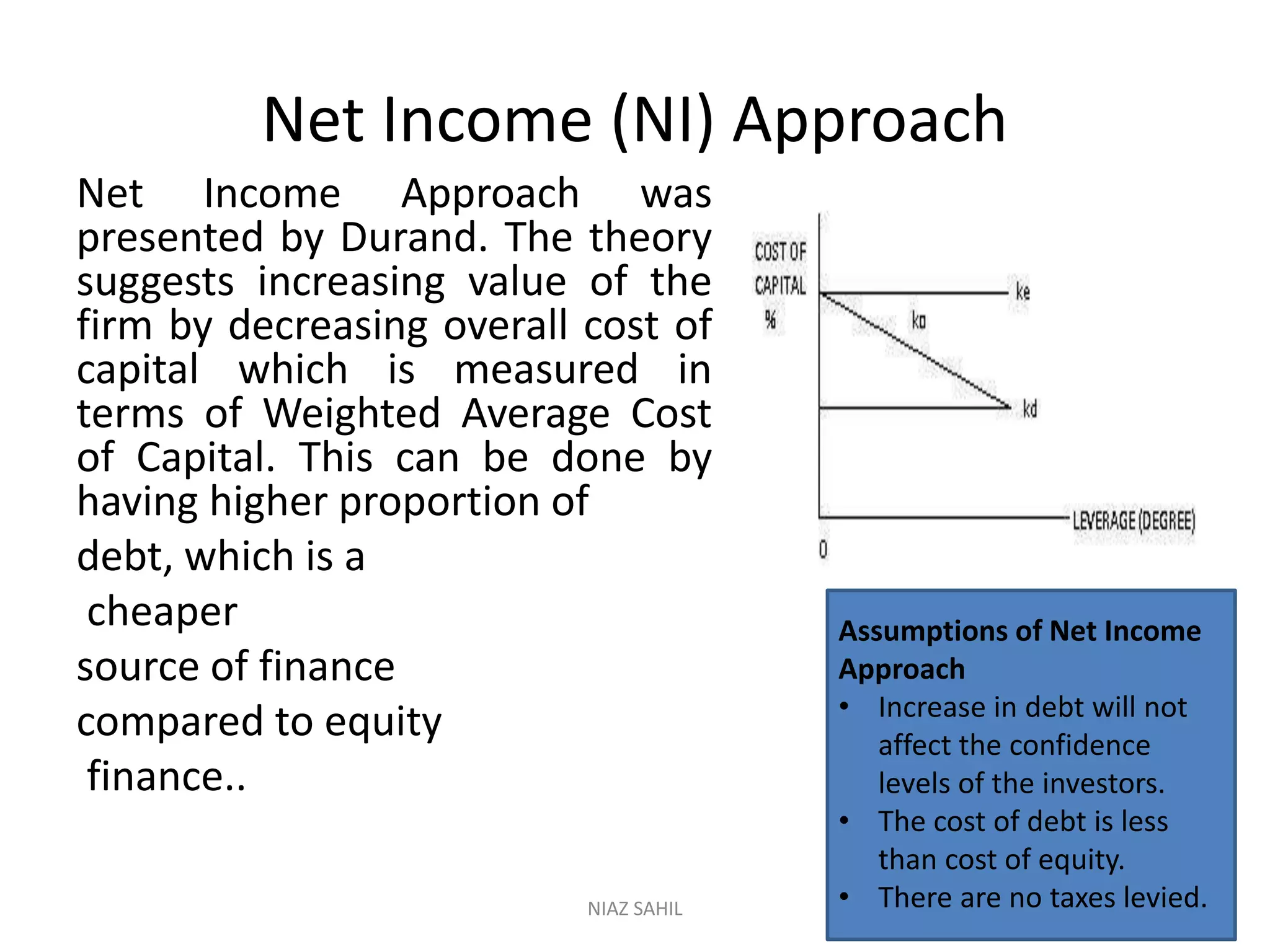

Financial management involves planning and controlling a company's finances to achieve its objectives. It is concerned with raising financial resources and using them effectively. The scope of financial management includes anticipating financial needs, acquiring funds from various sources, allocating funds to purchase assets, appropriating profits, and assessing all financial activities. Capital budgeting is the process of evaluating long-term investments and determining which investments are worth pursuing. There are various techniques used in capital budgeting such as payback period, net present value, internal rate of return, and profitability index. Working capital management involves managing current assets like inventory, accounts receivable, and cash as well as current liabilities to ensure the company can continue operating and meet short-term obligations.