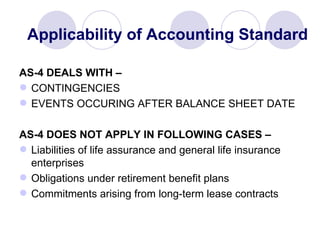

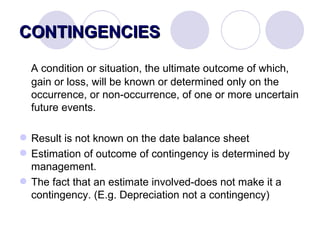

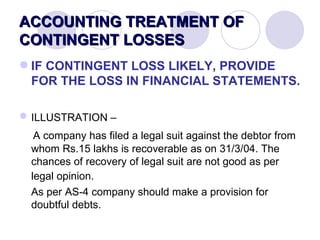

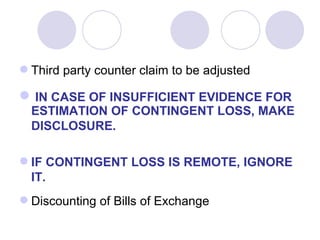

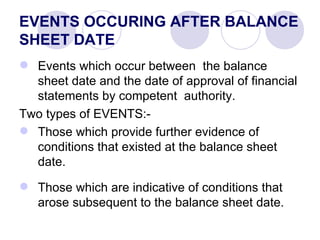

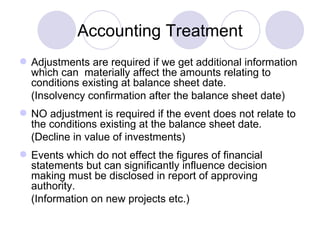

This document summarizes Accounting Standard 4 regarding contingencies and events occurring after the balance sheet date. It outlines that AS-4 does not apply to certain insurance and retirement obligations or long-term lease commitments. It defines contingencies as uncertain future events whose outcomes depend on circumstances. Contingent losses should be provided for if likely, and disclosed if evidence is insufficient for estimation but not remote. Events after the balance sheet date are adjusted for if they provide evidence of prior conditions, and disclosed if they materially affect financial position.