Downloaded 62 times

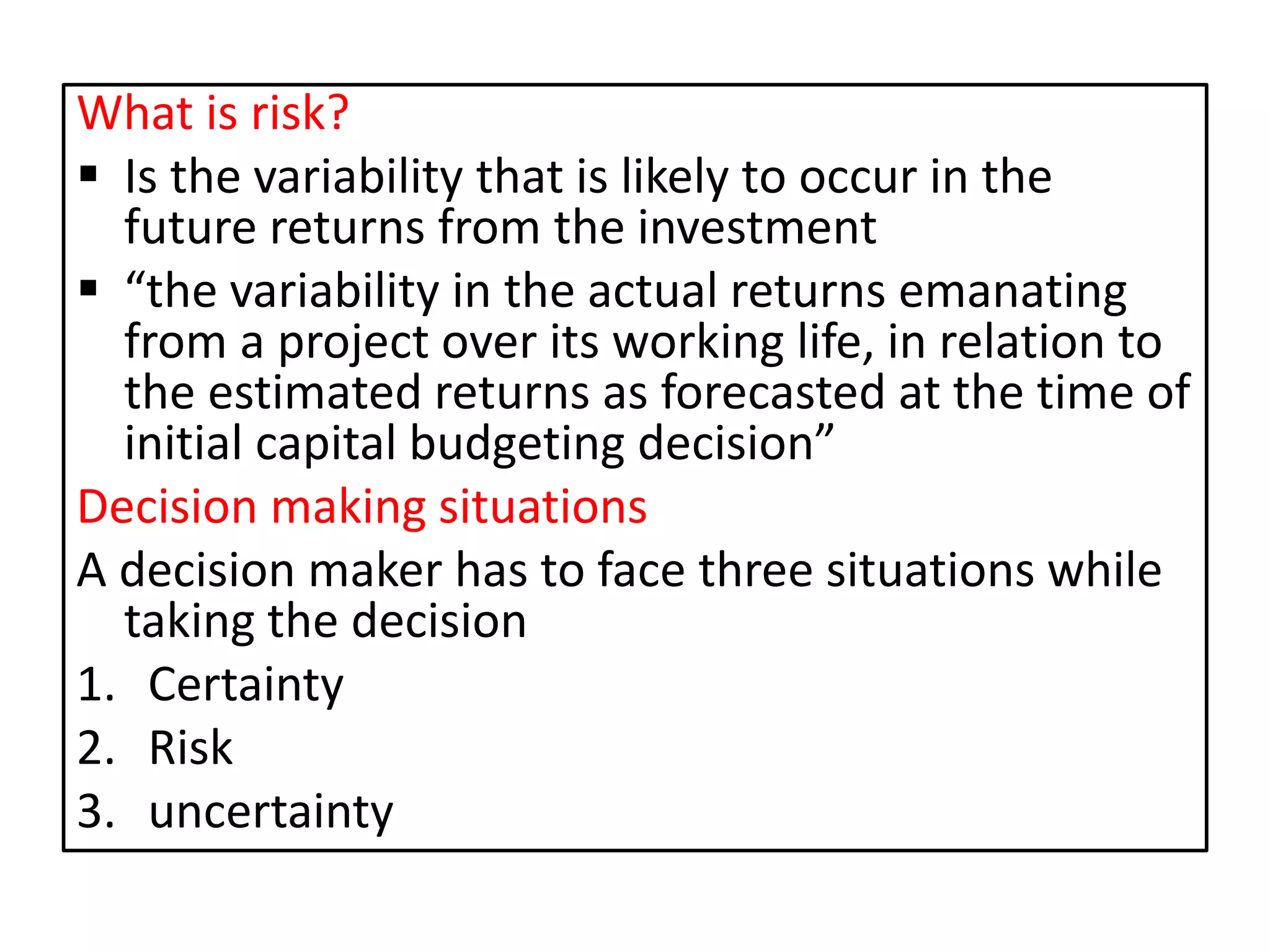

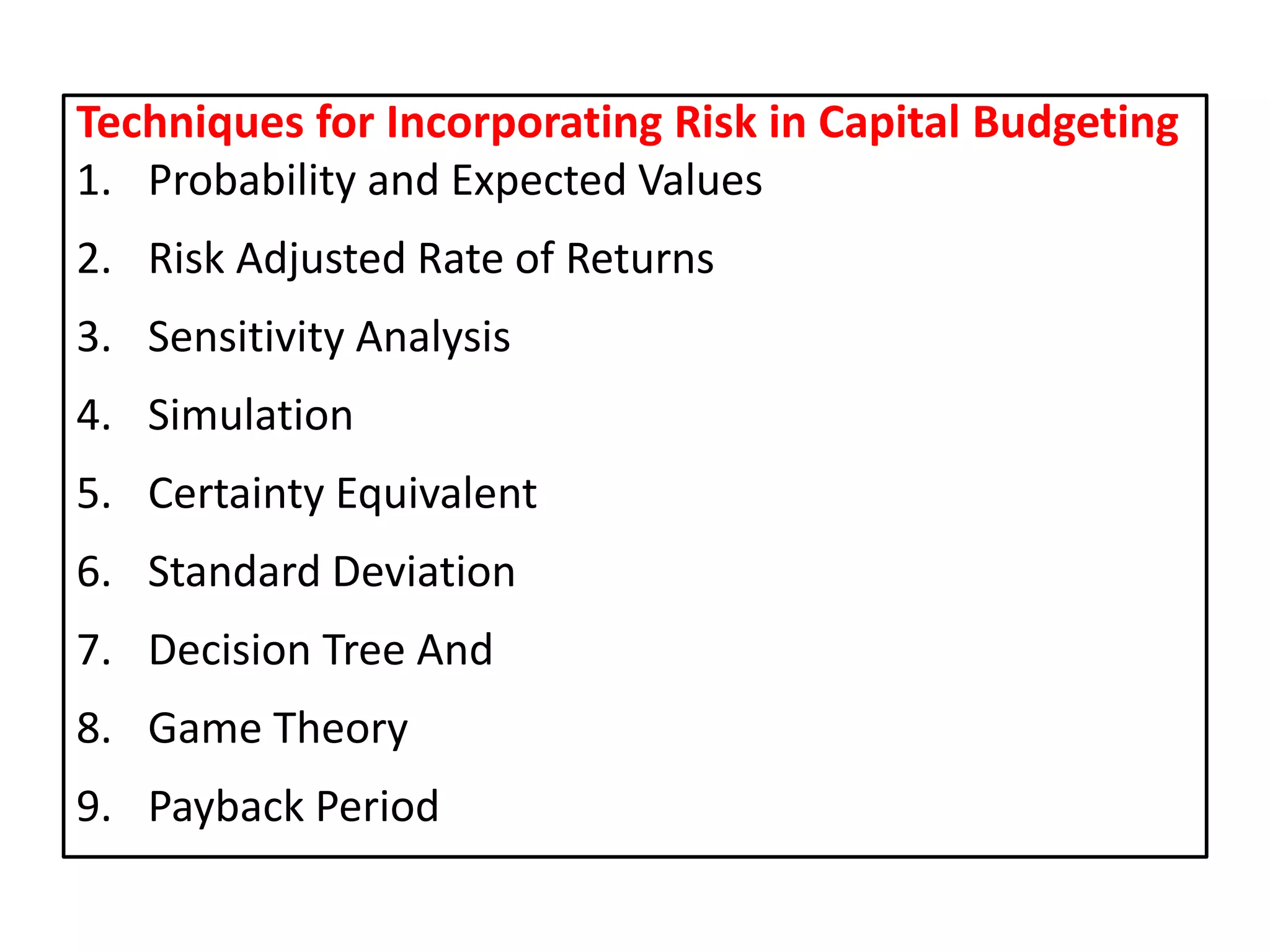

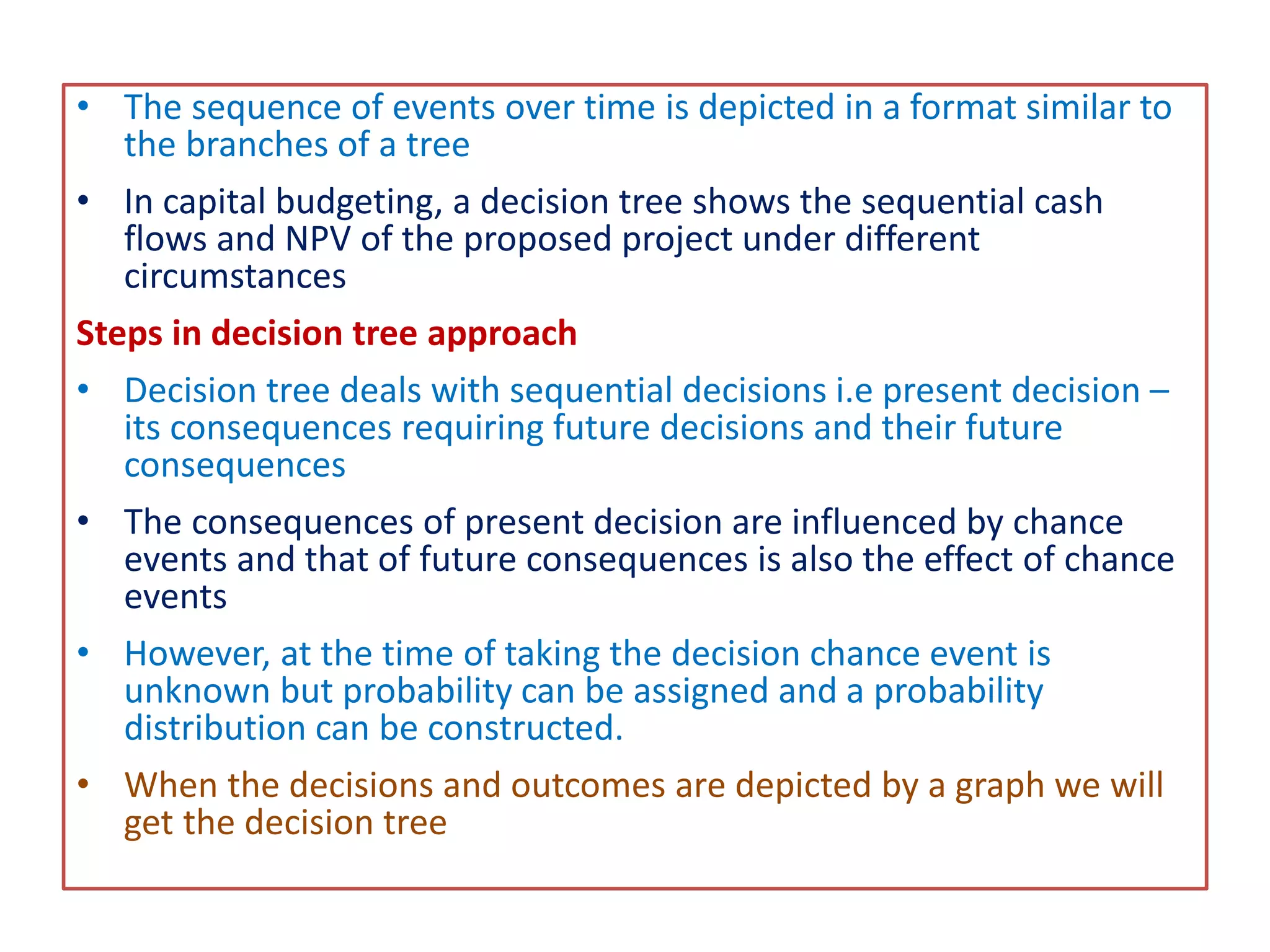

The document discusses the critical role of risk analysis in capital budgeting and decision-making, emphasizing the uncertainty surrounding future cash flows and returns associated with capital expenditures. It outlines various methods for incorporating risk, such as probability distributions, sensitivity analysis, and decision trees, while explaining how different degrees of certainty, risk, and uncertainty affect decision-making. Additionally, it details how to calculate expected net present values (ENPVs) to evaluate investment projects and highlight the trade-offs between risk and profitability.