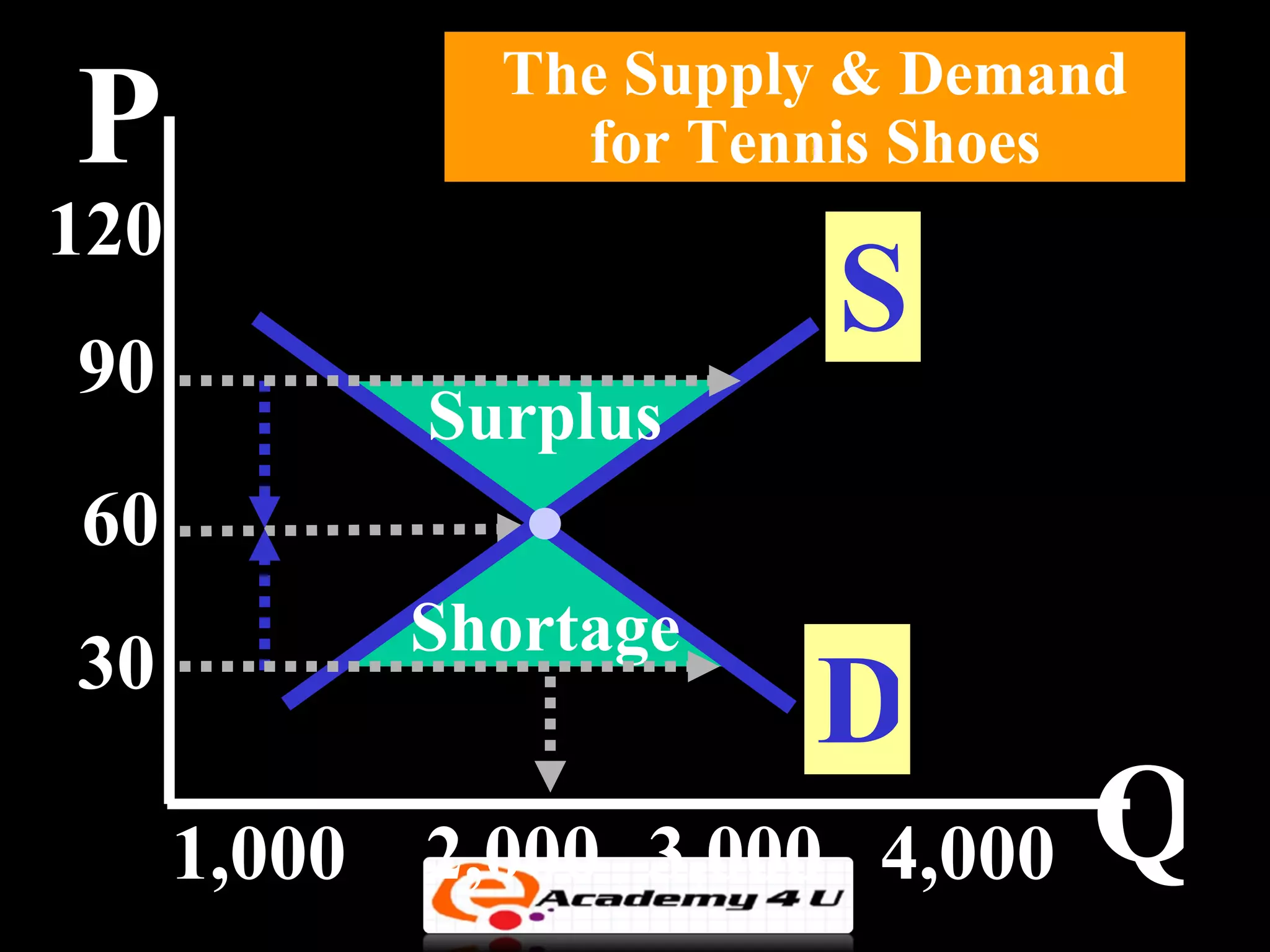

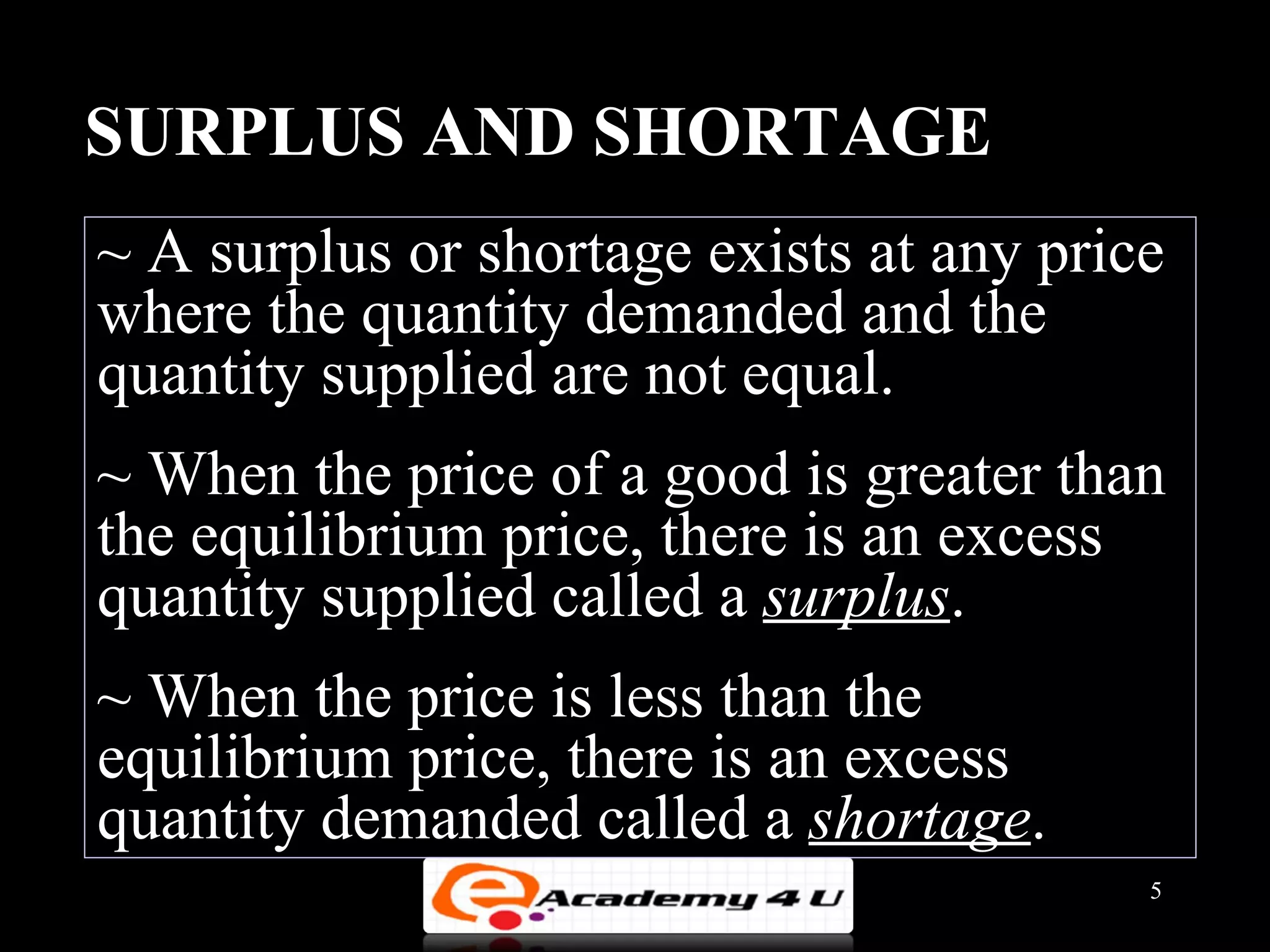

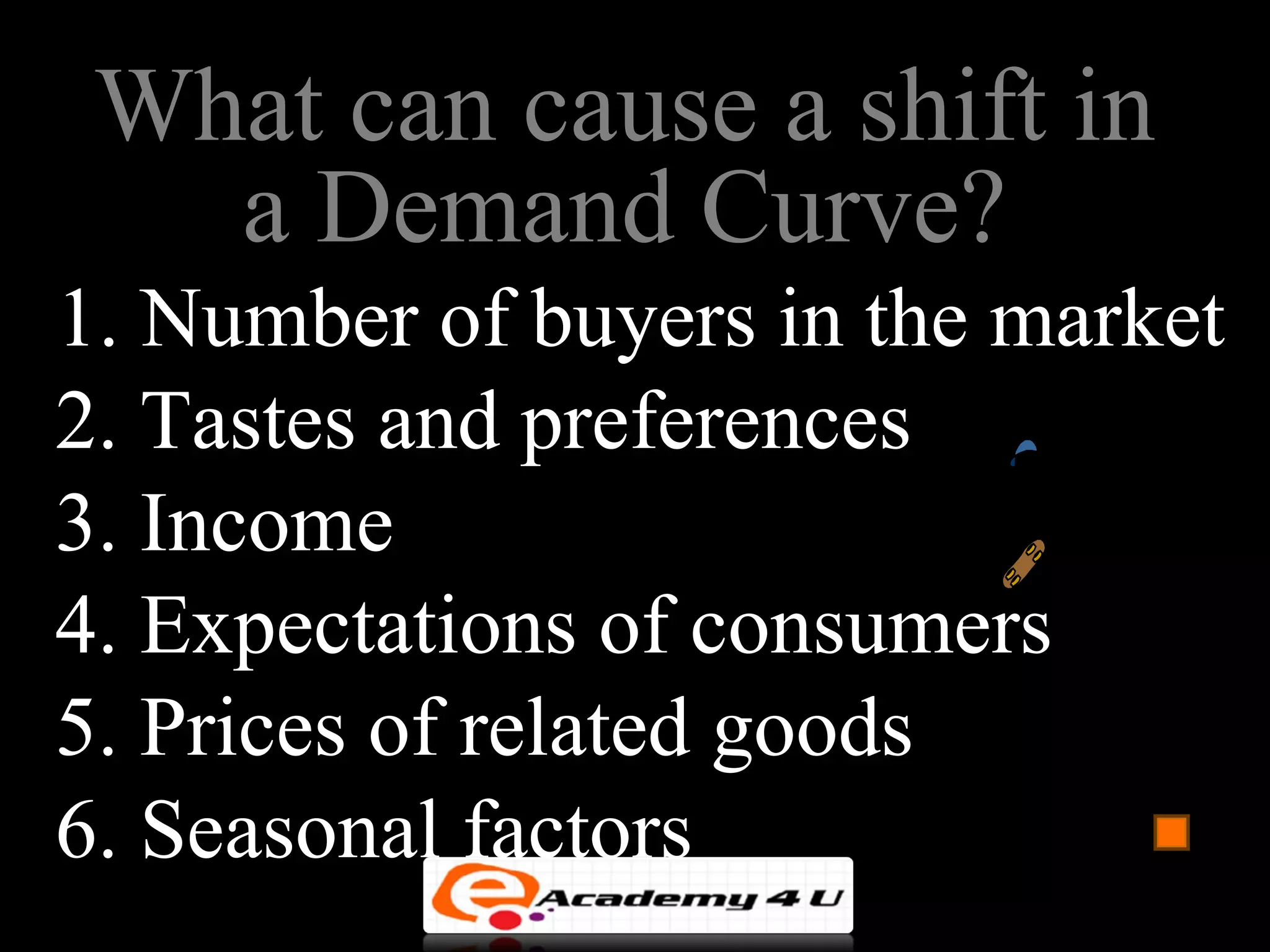

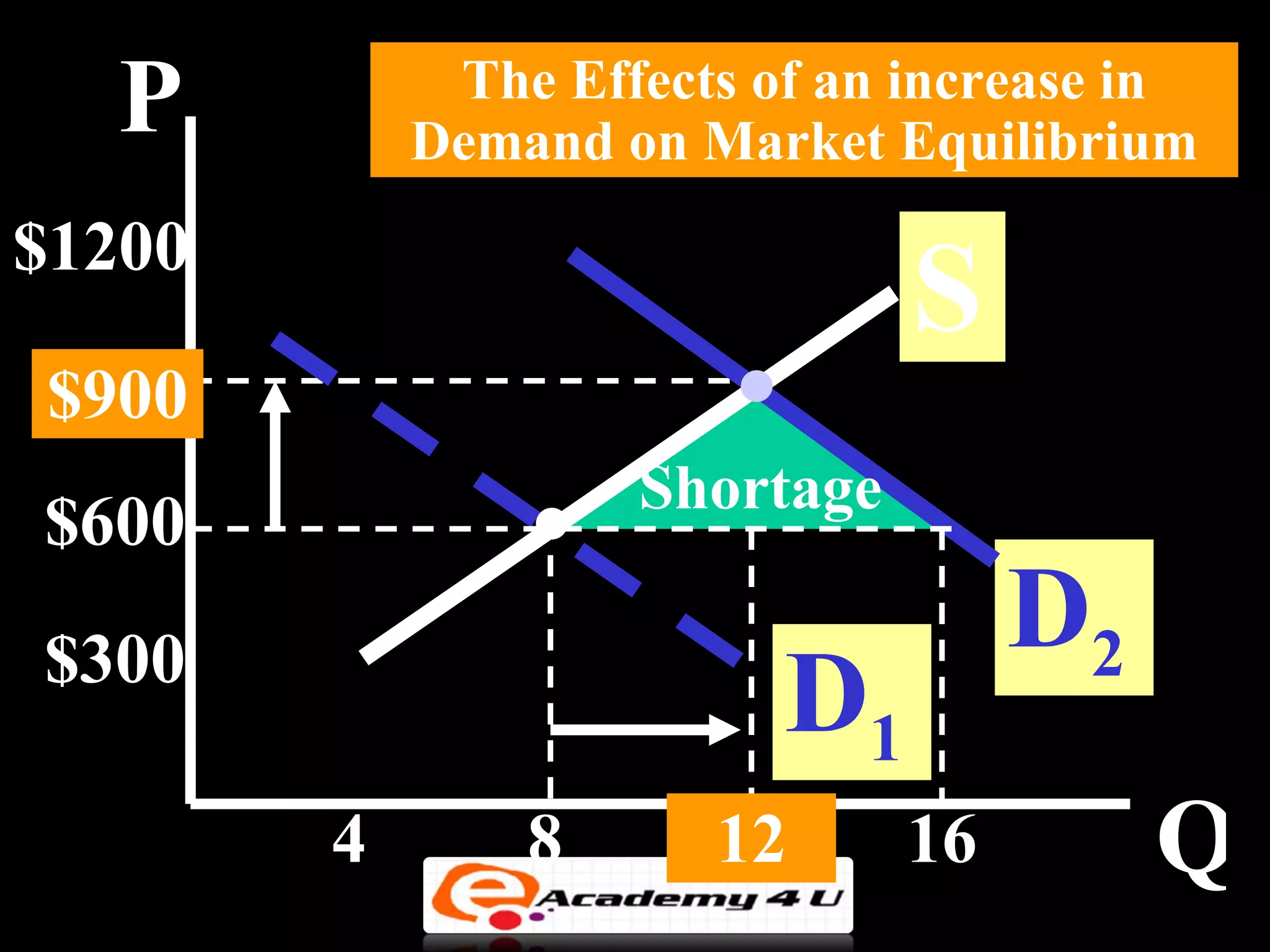

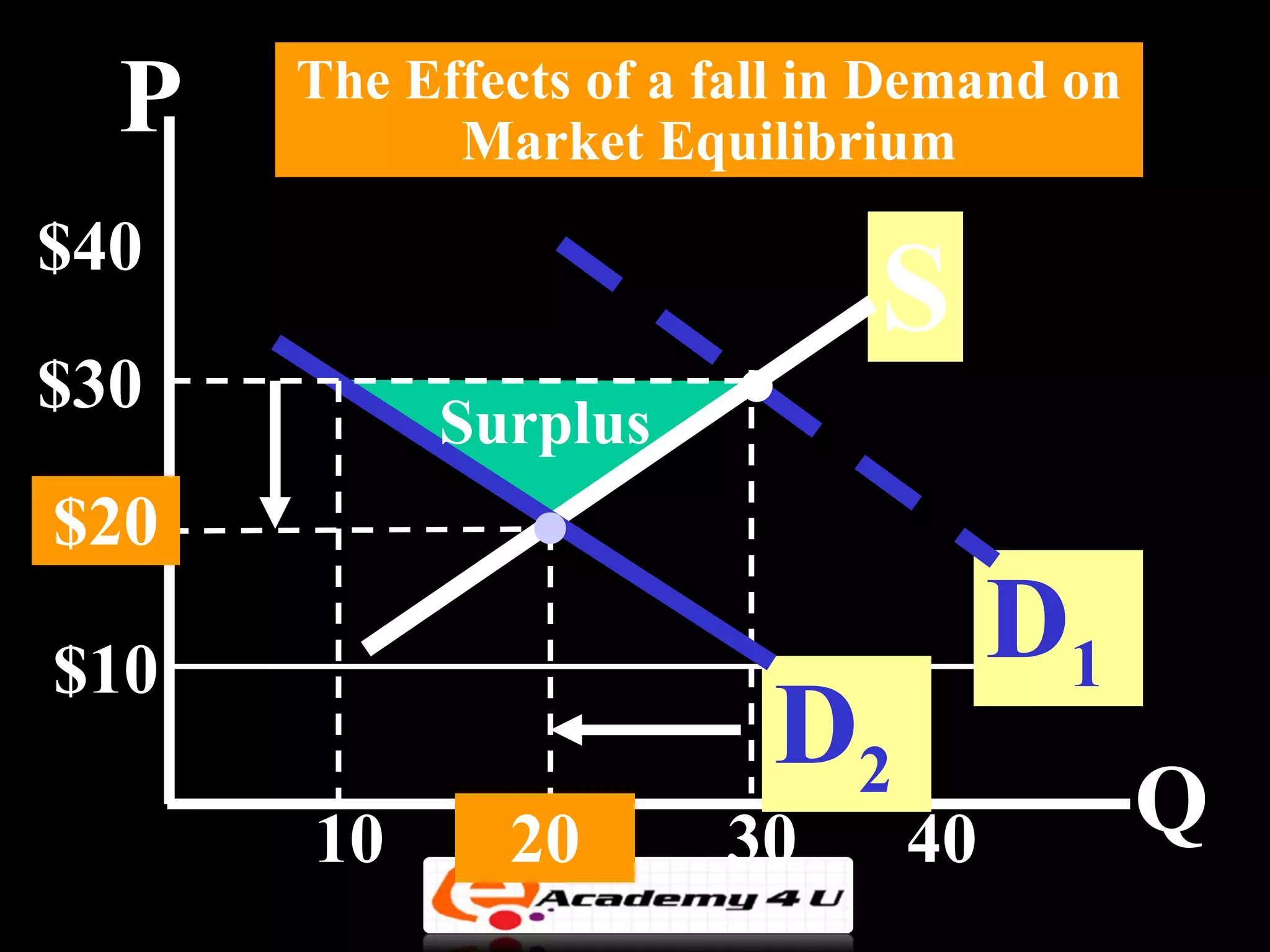

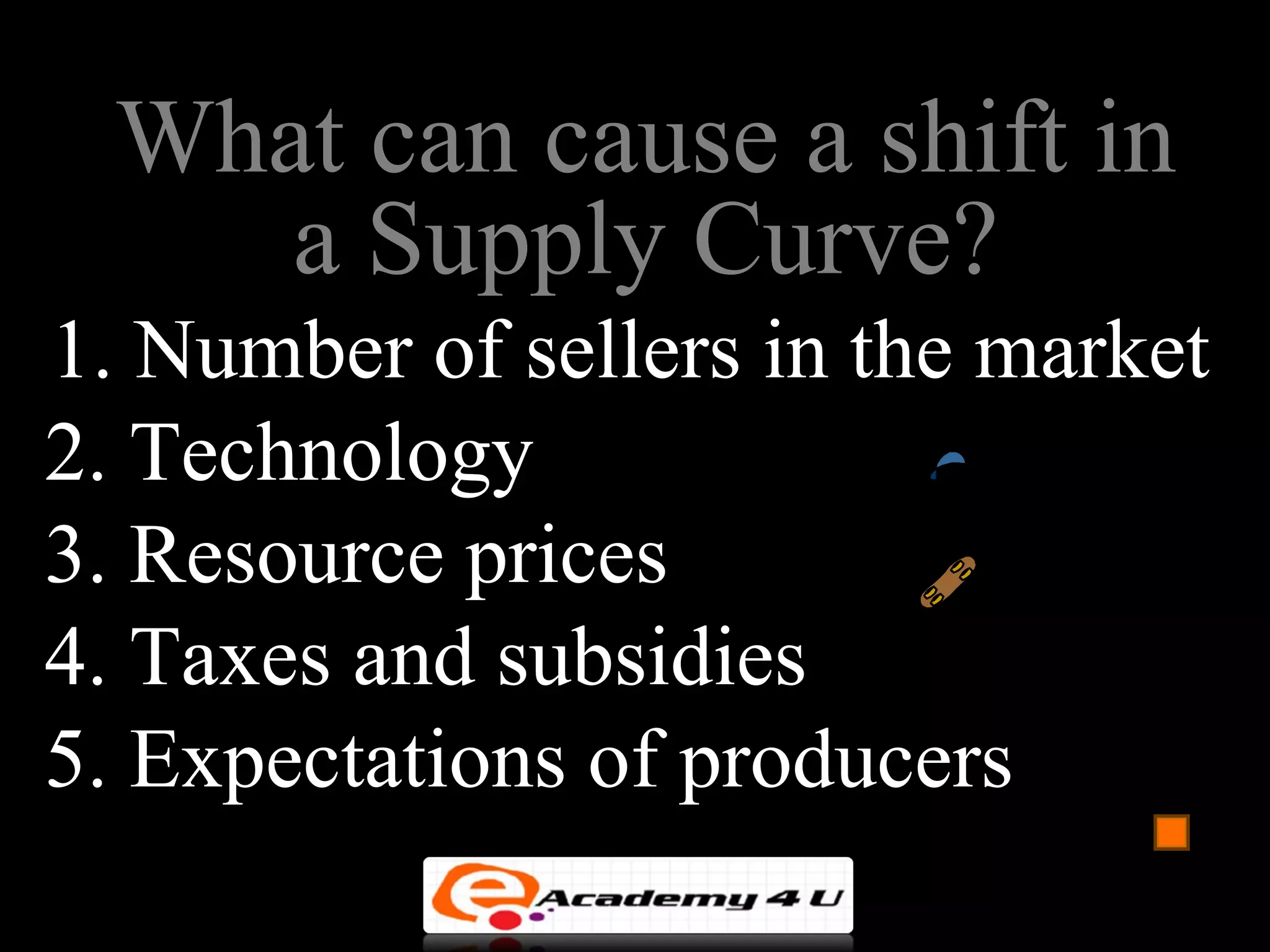

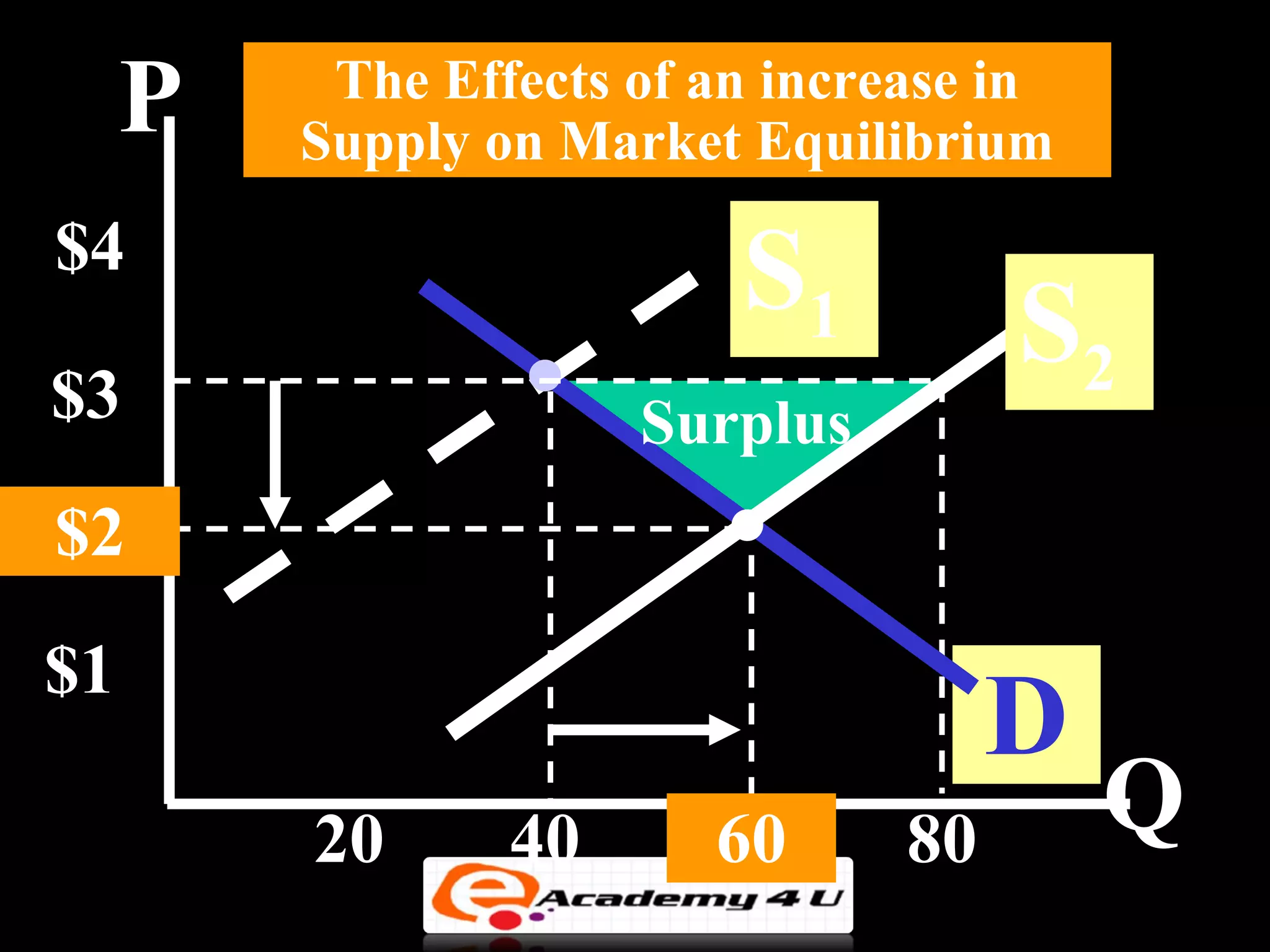

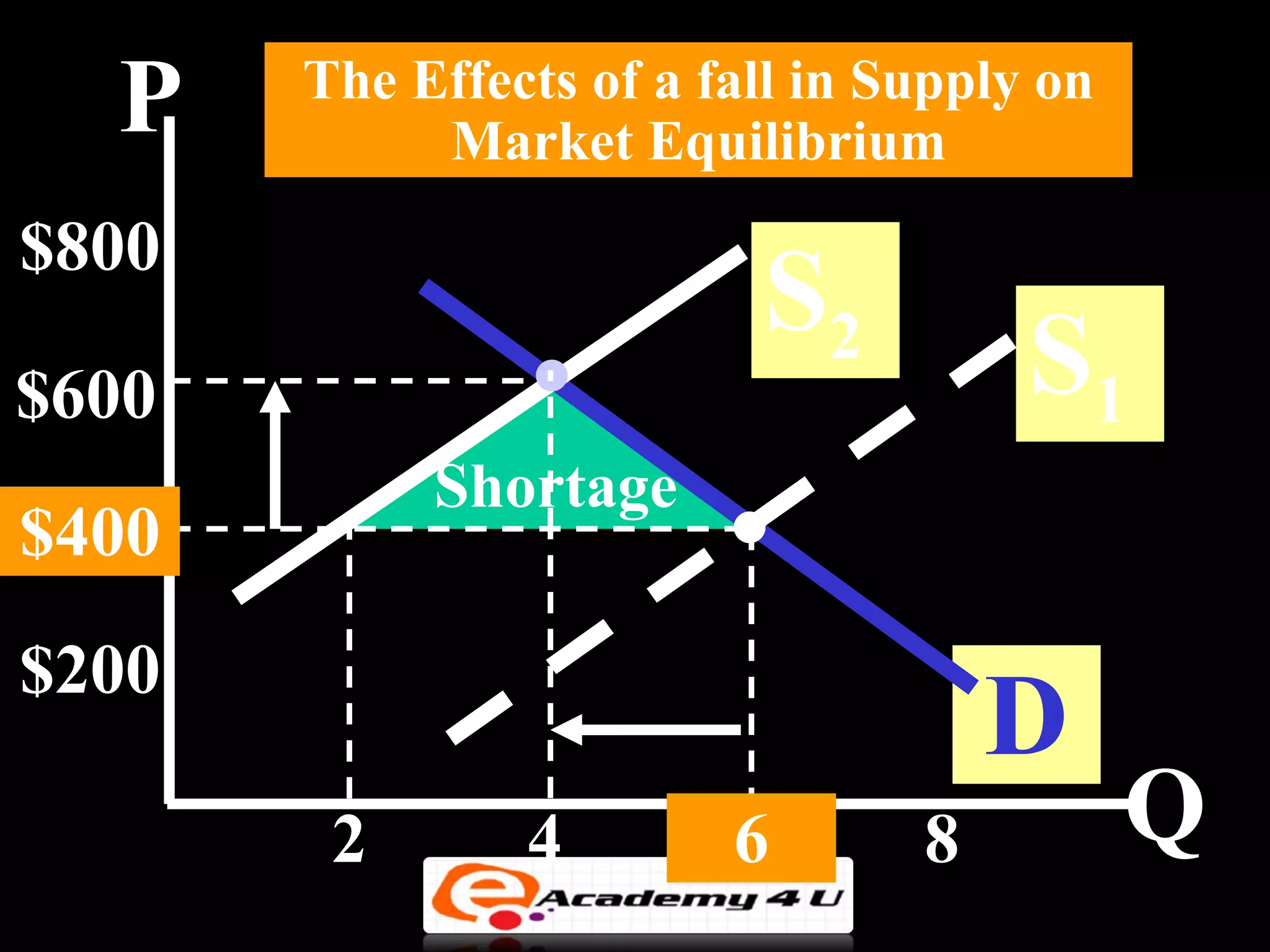

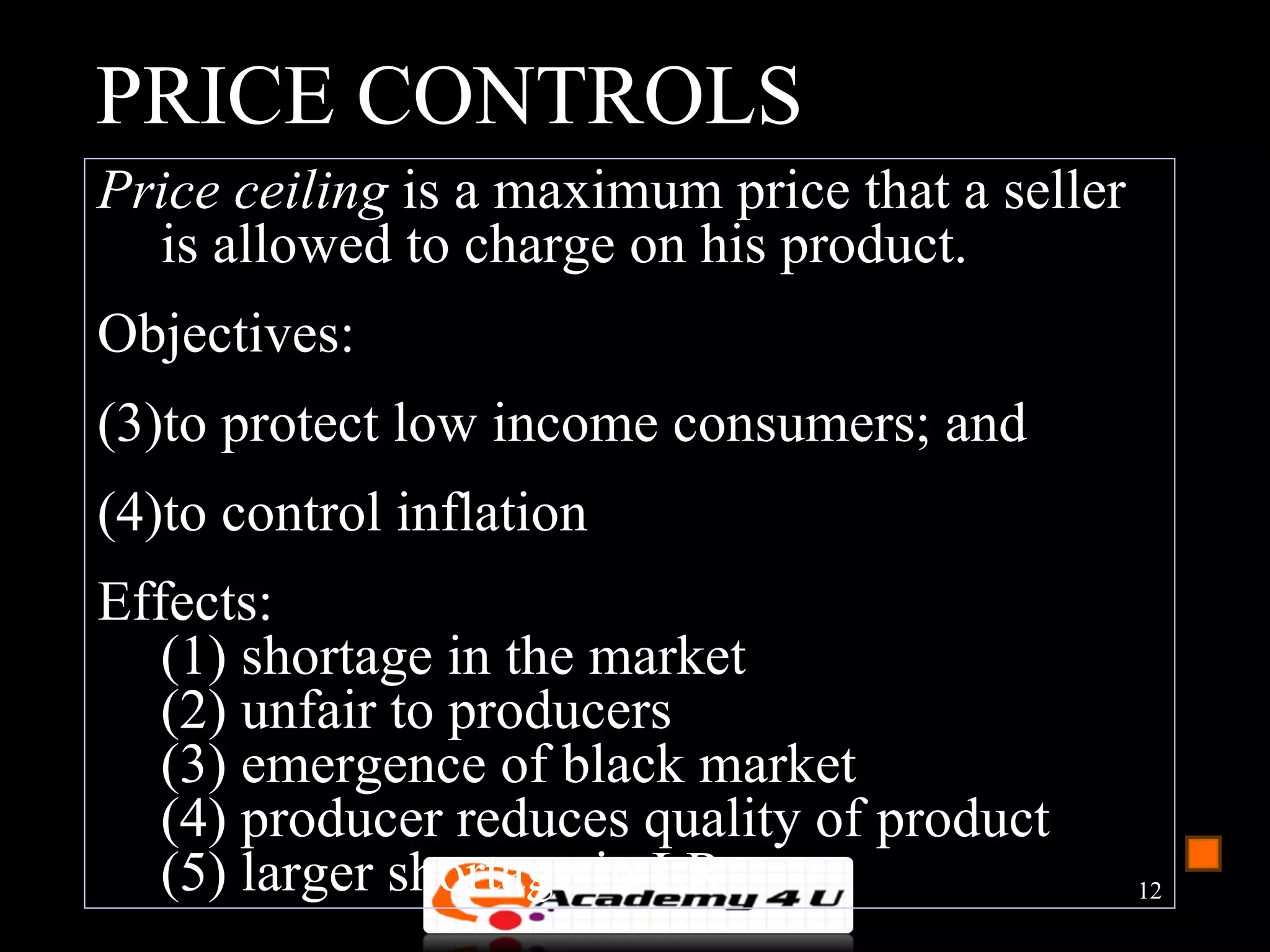

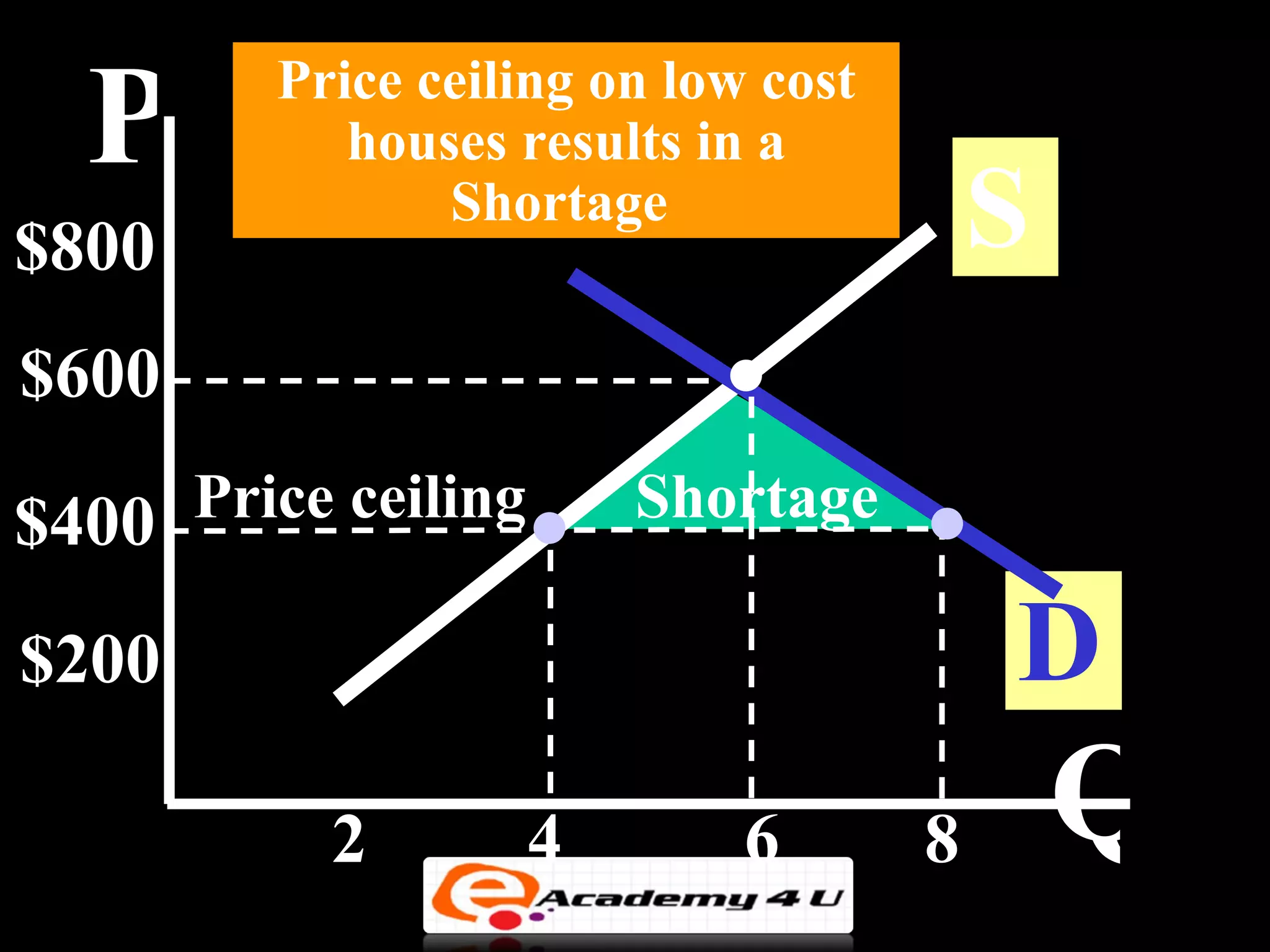

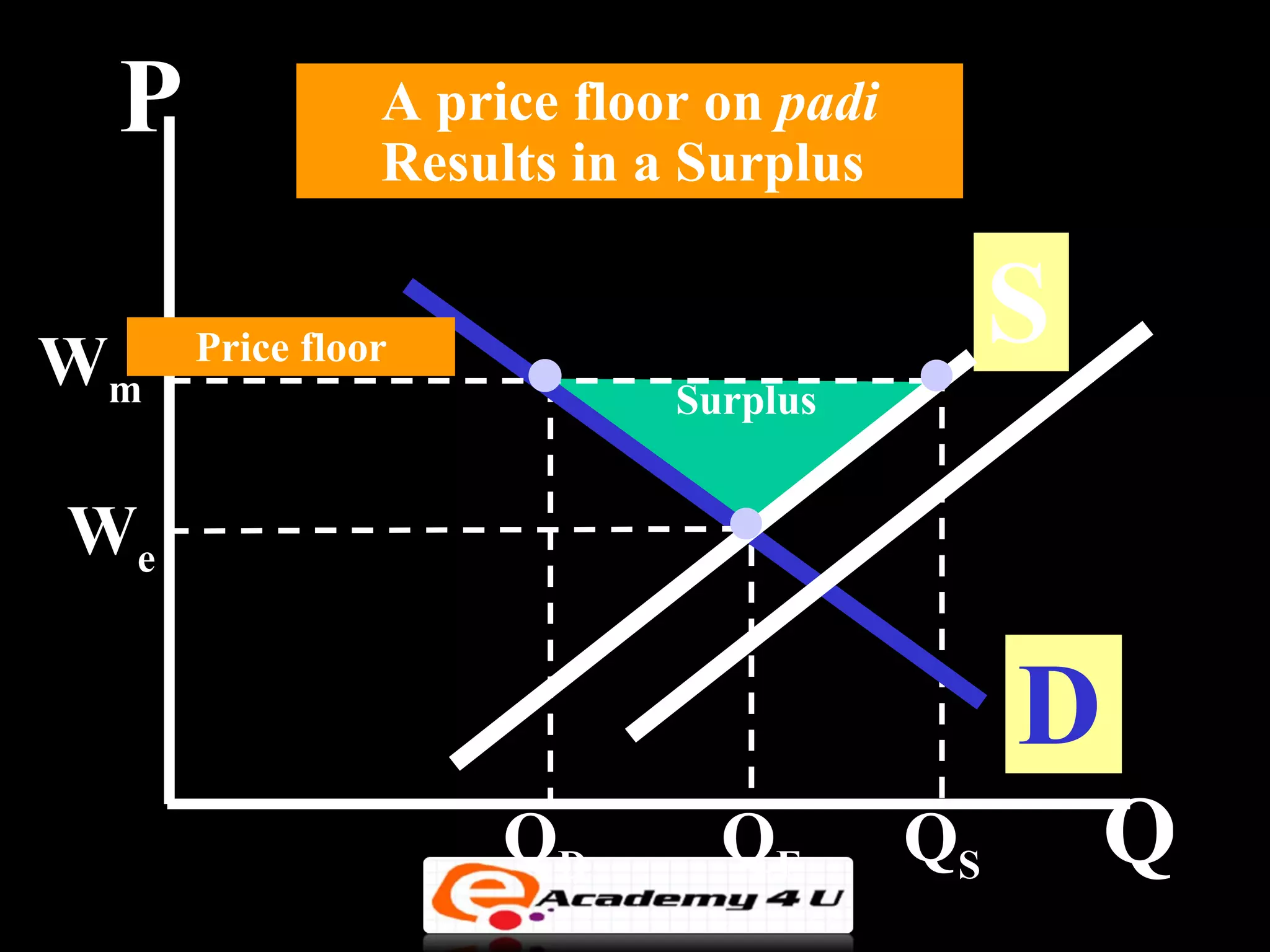

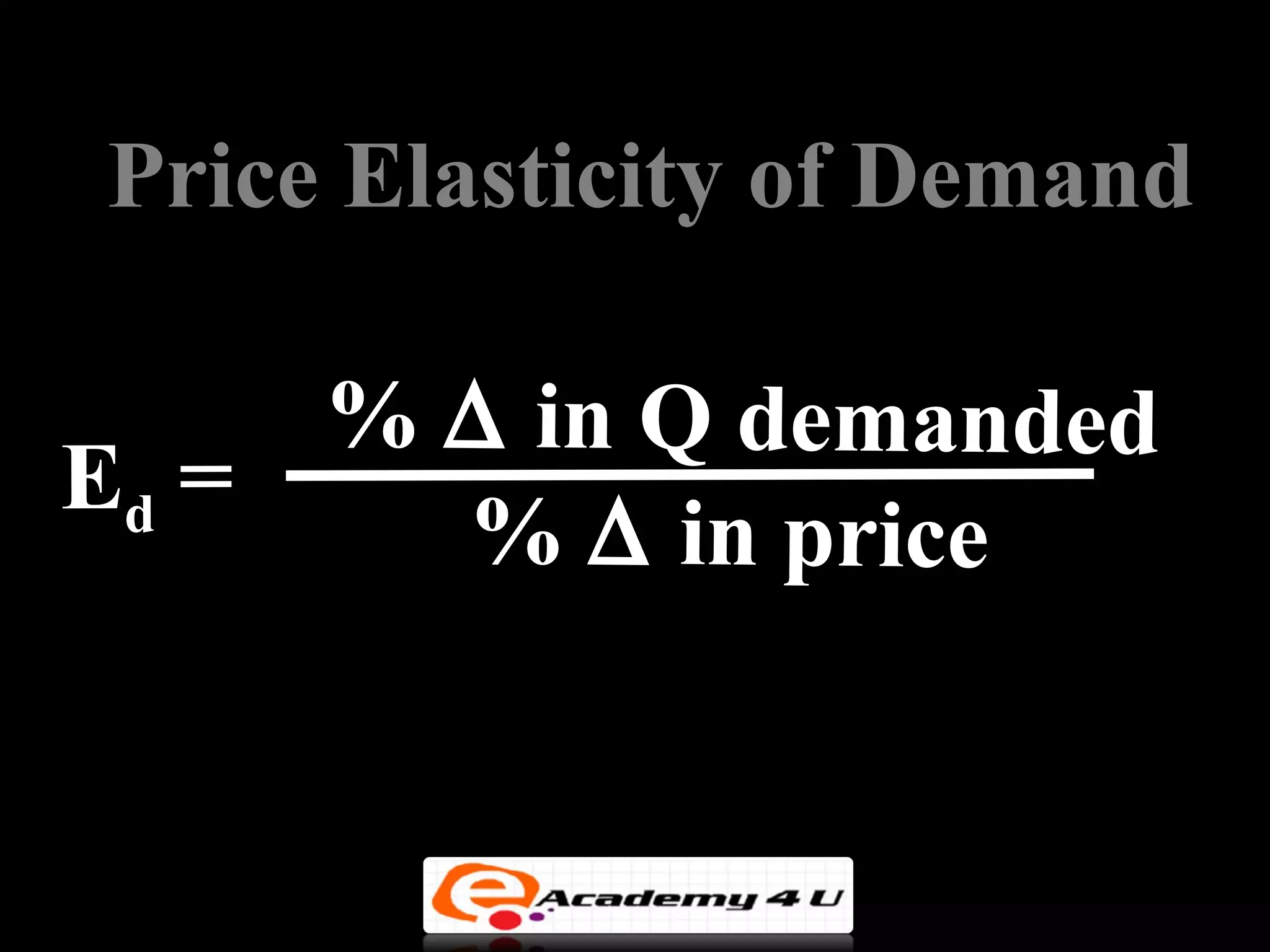

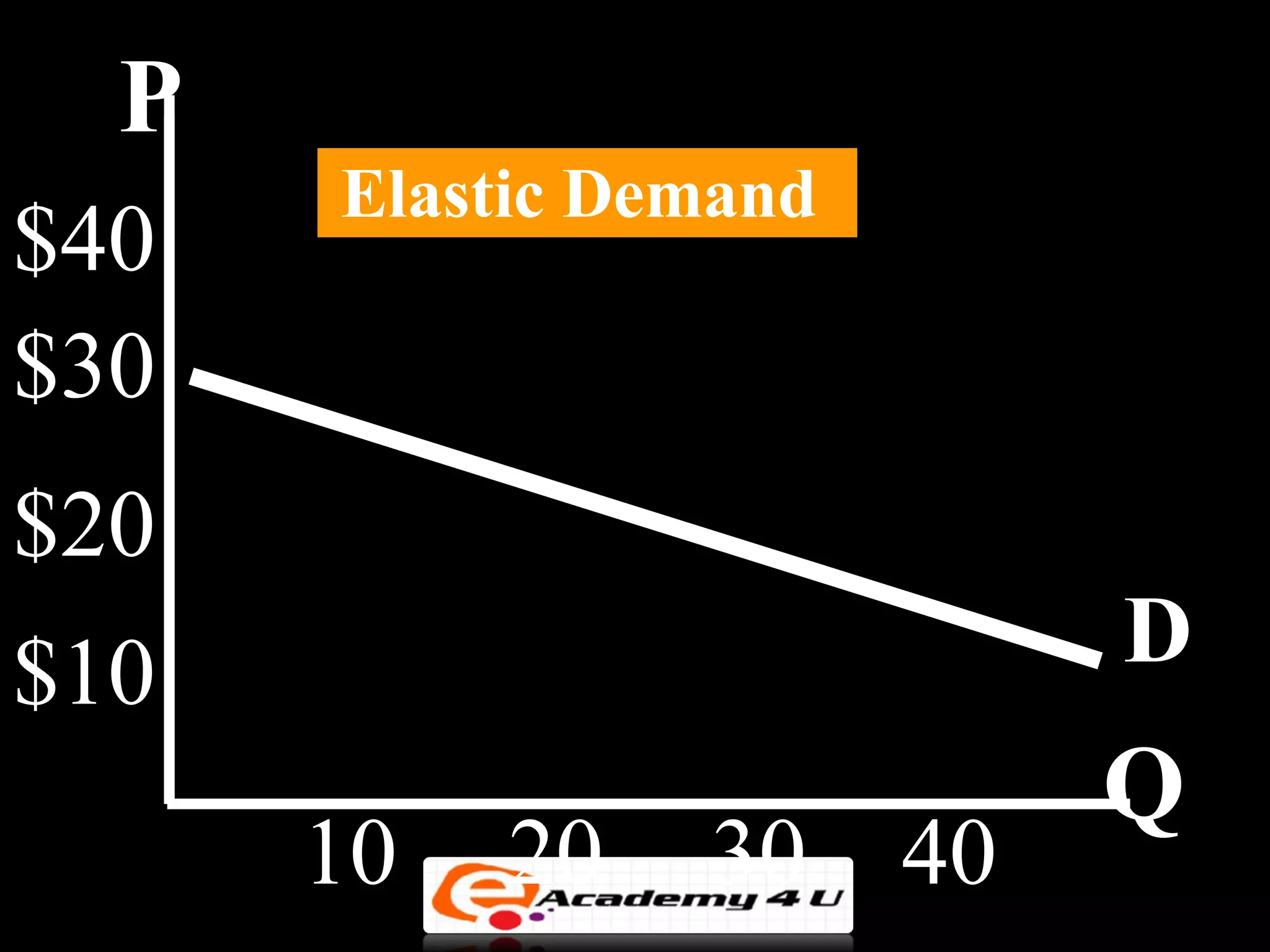

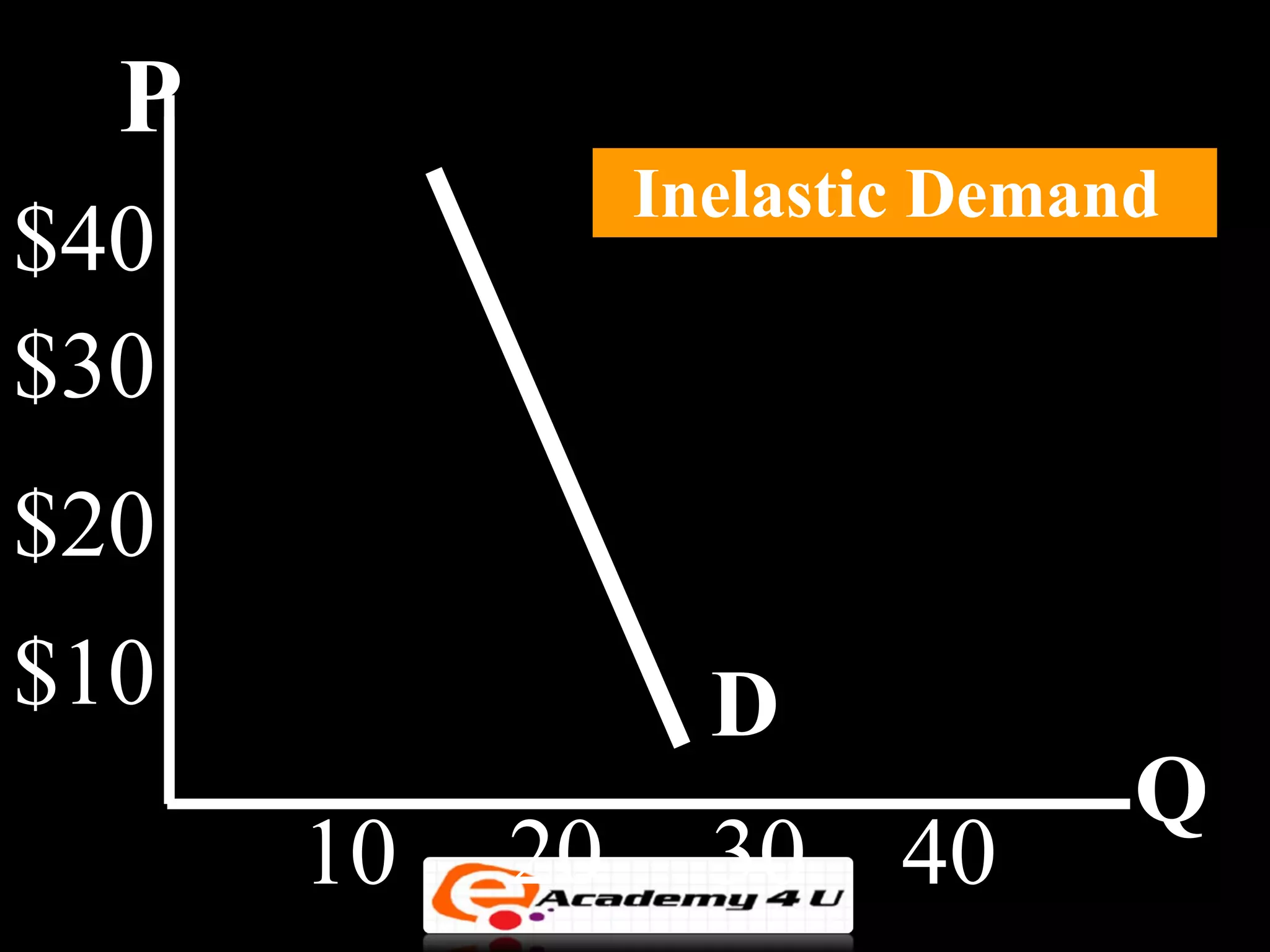

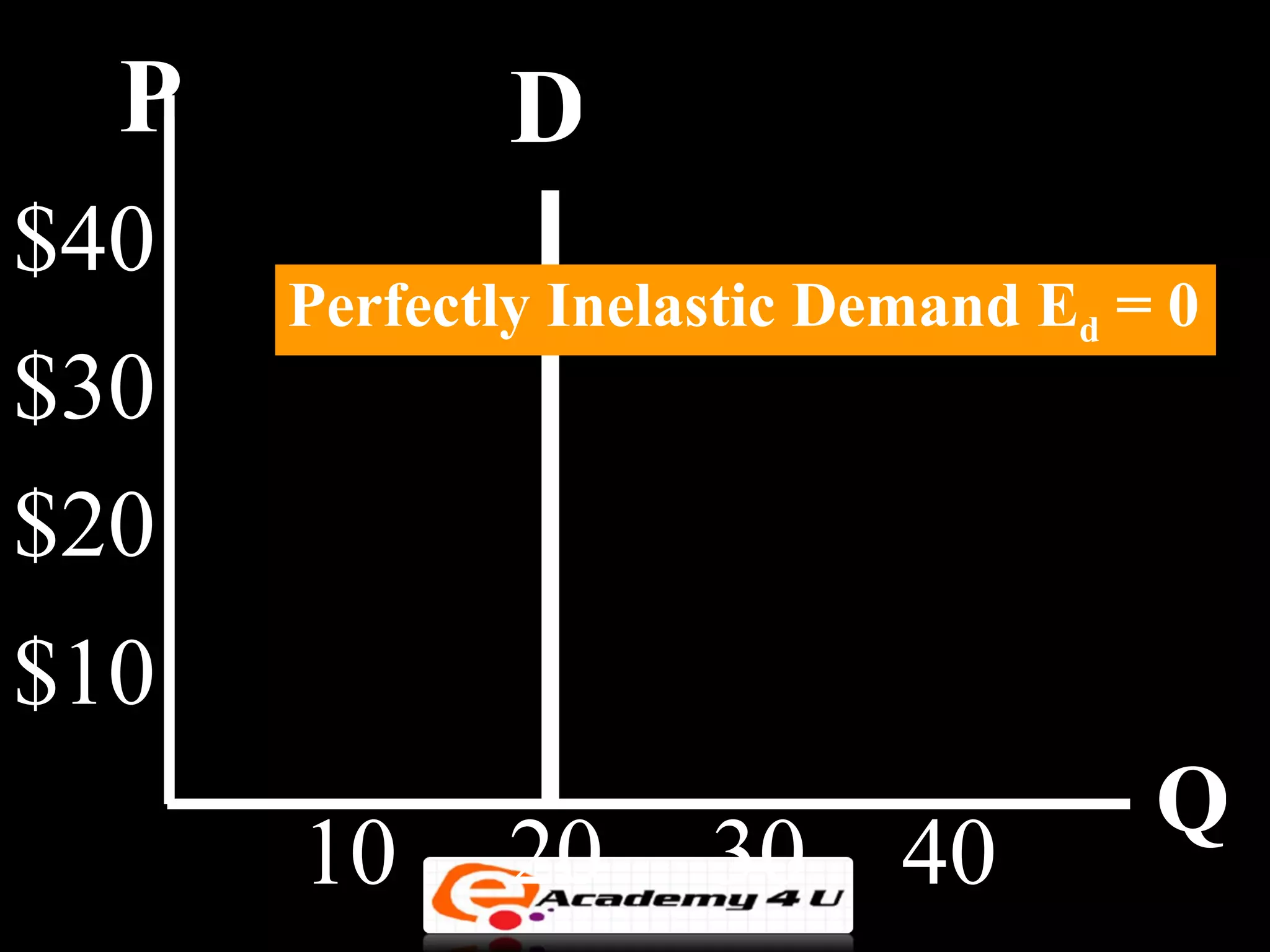

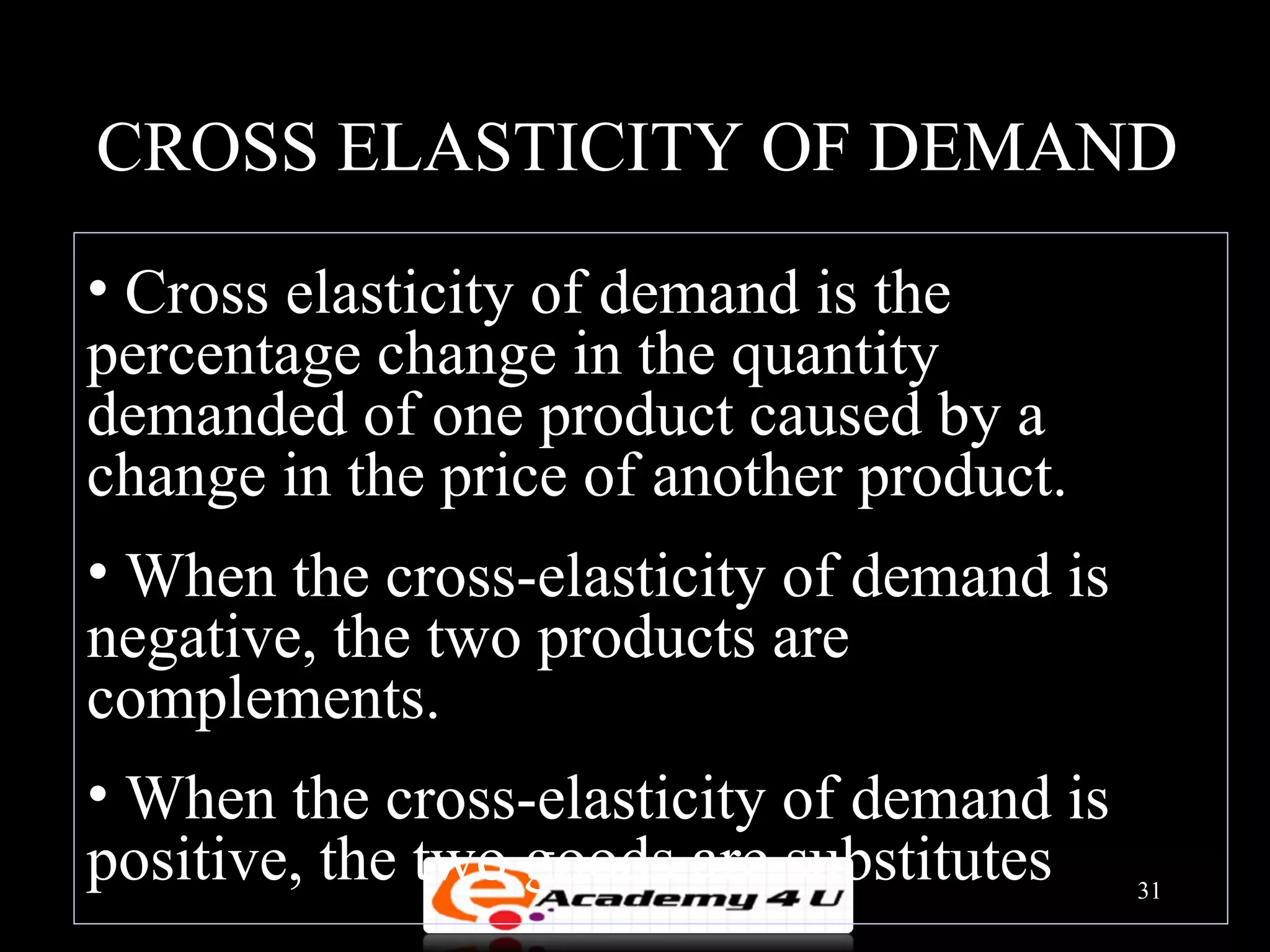

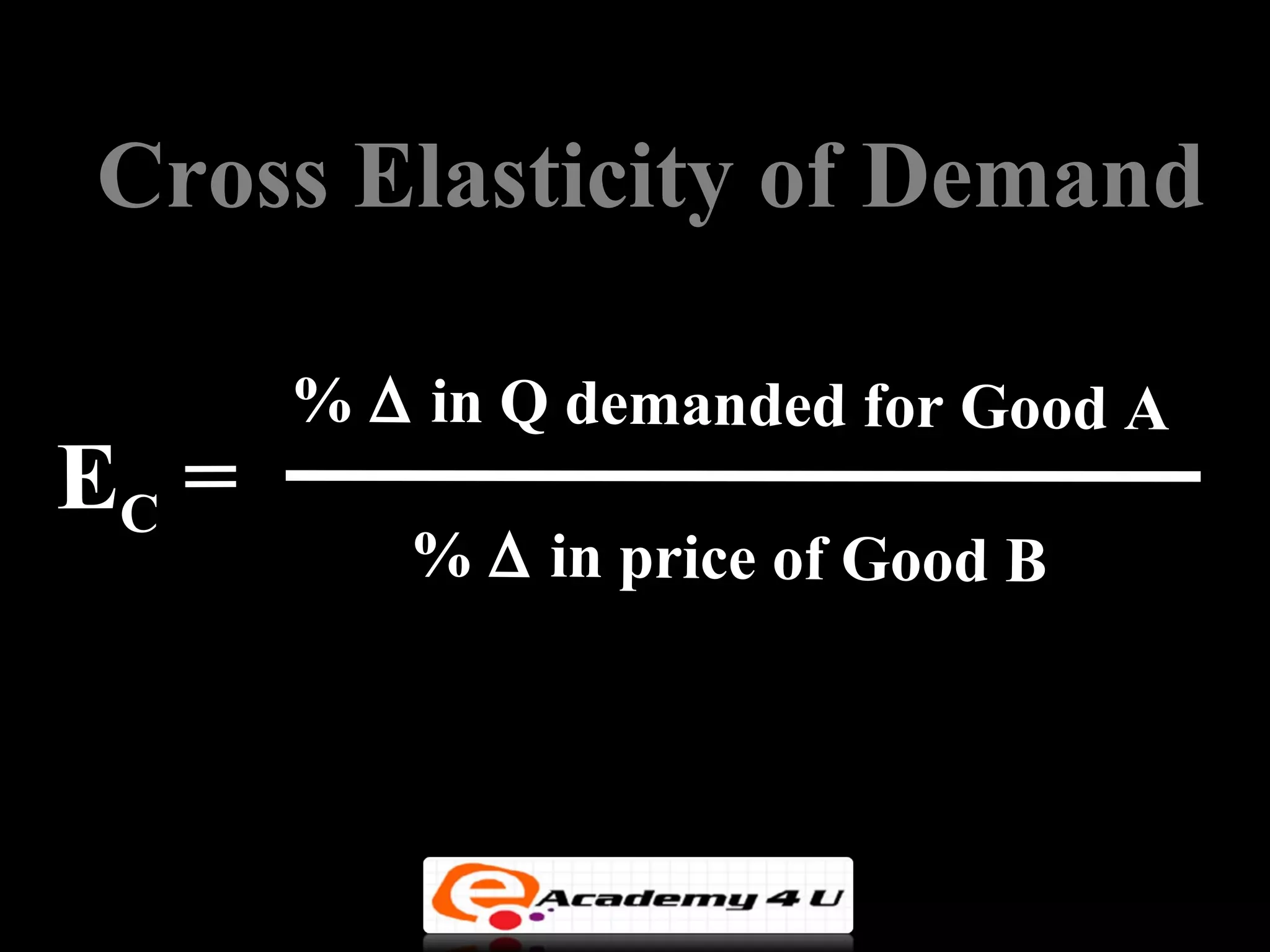

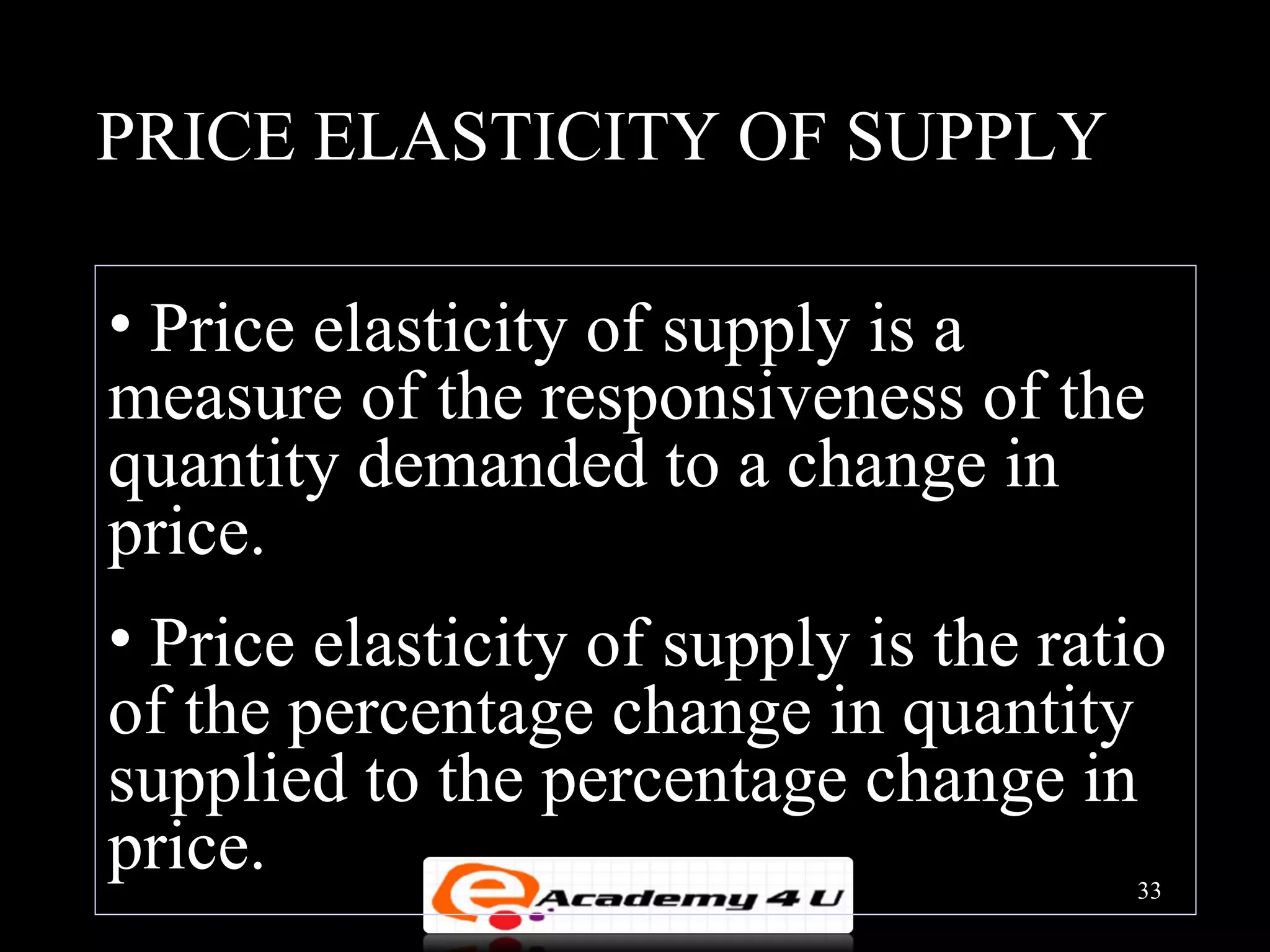

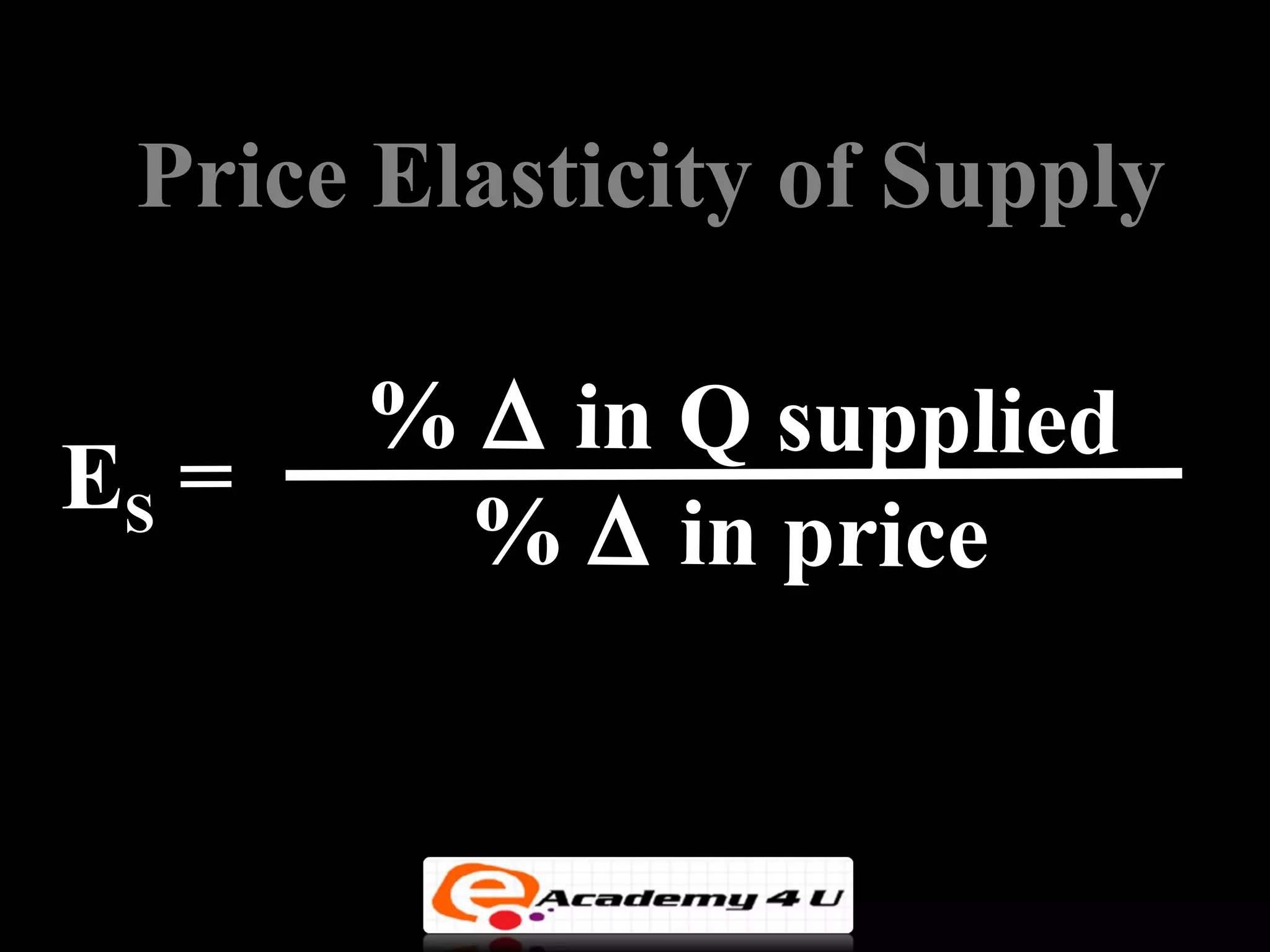

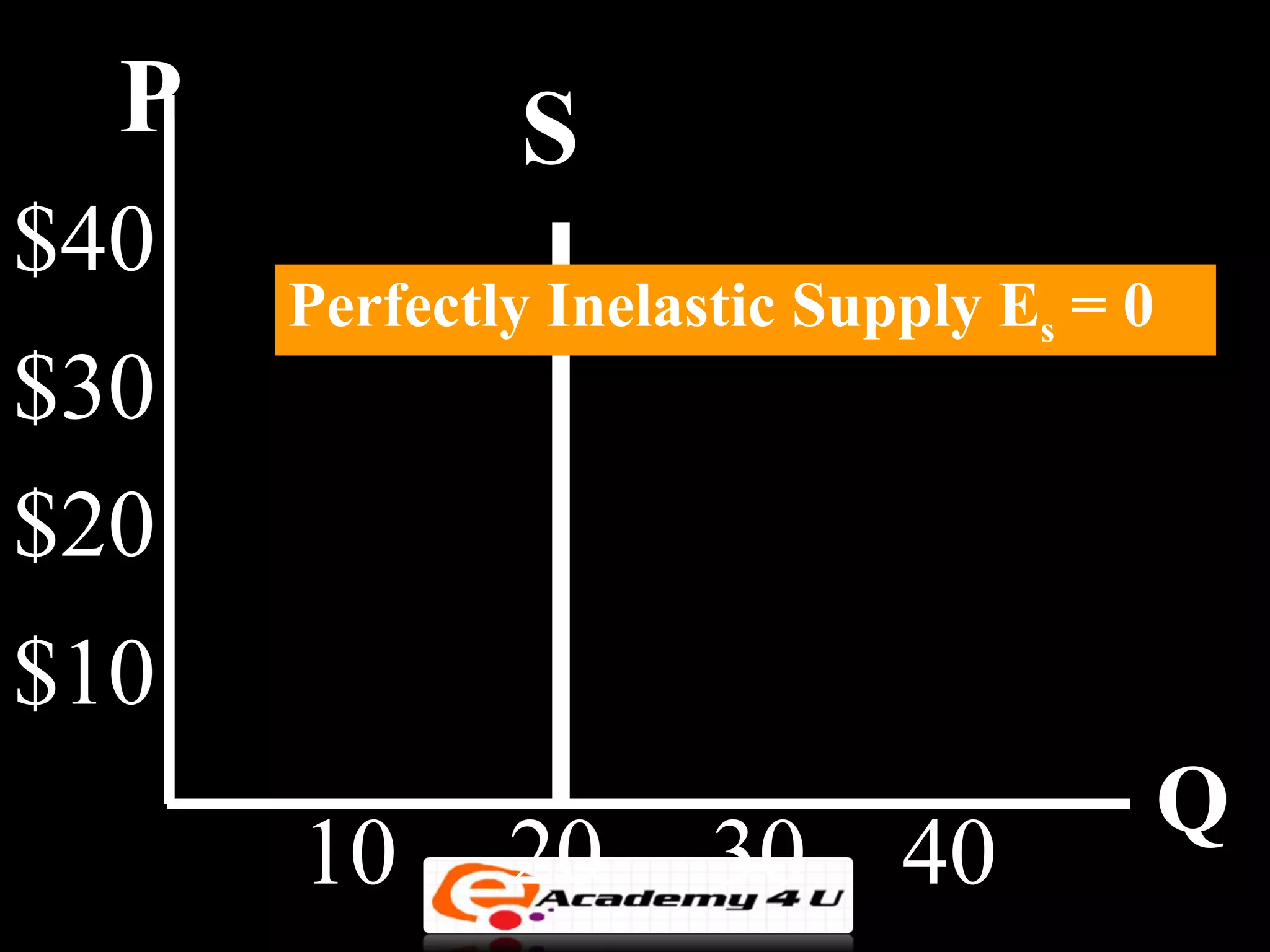

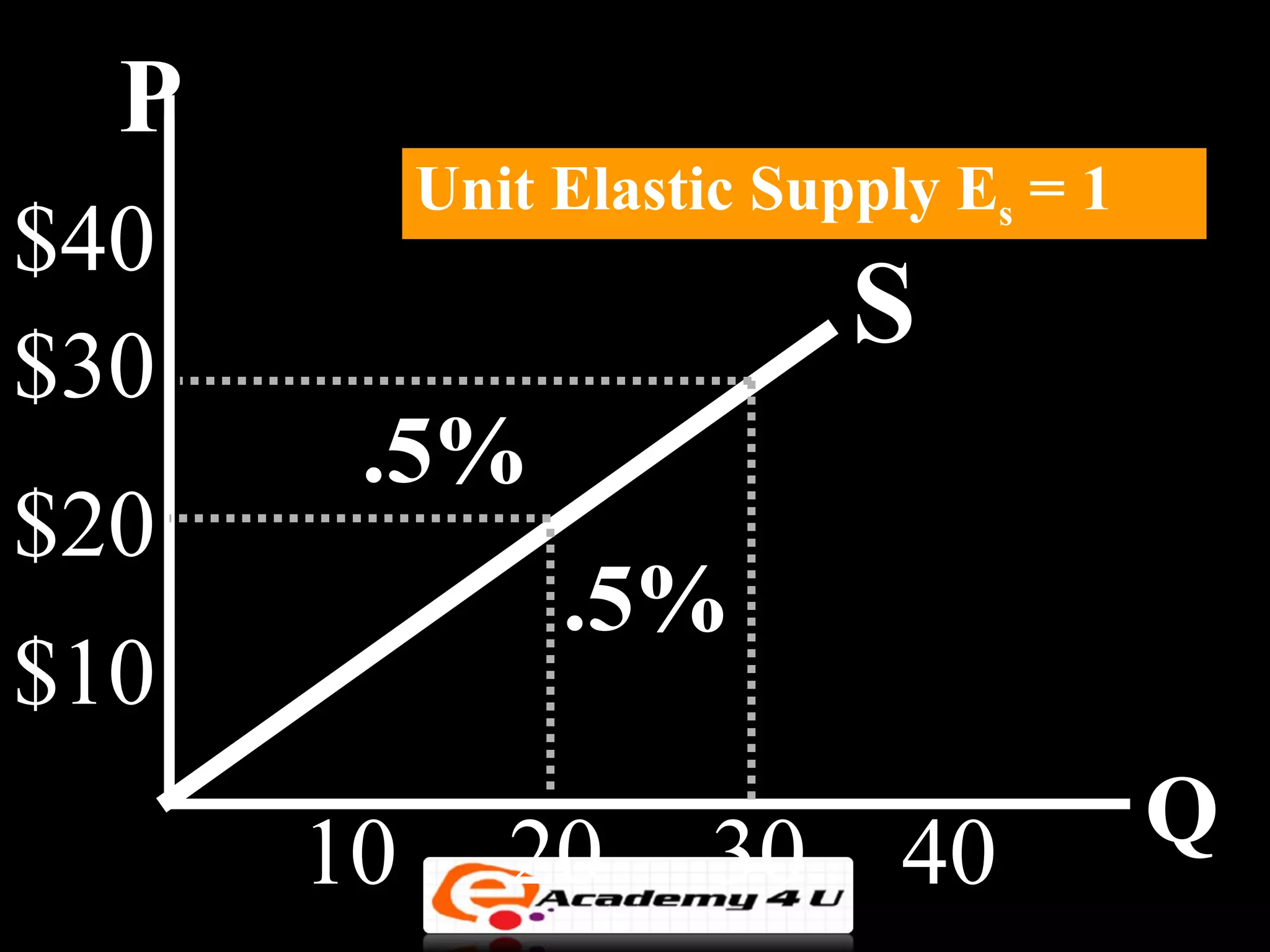

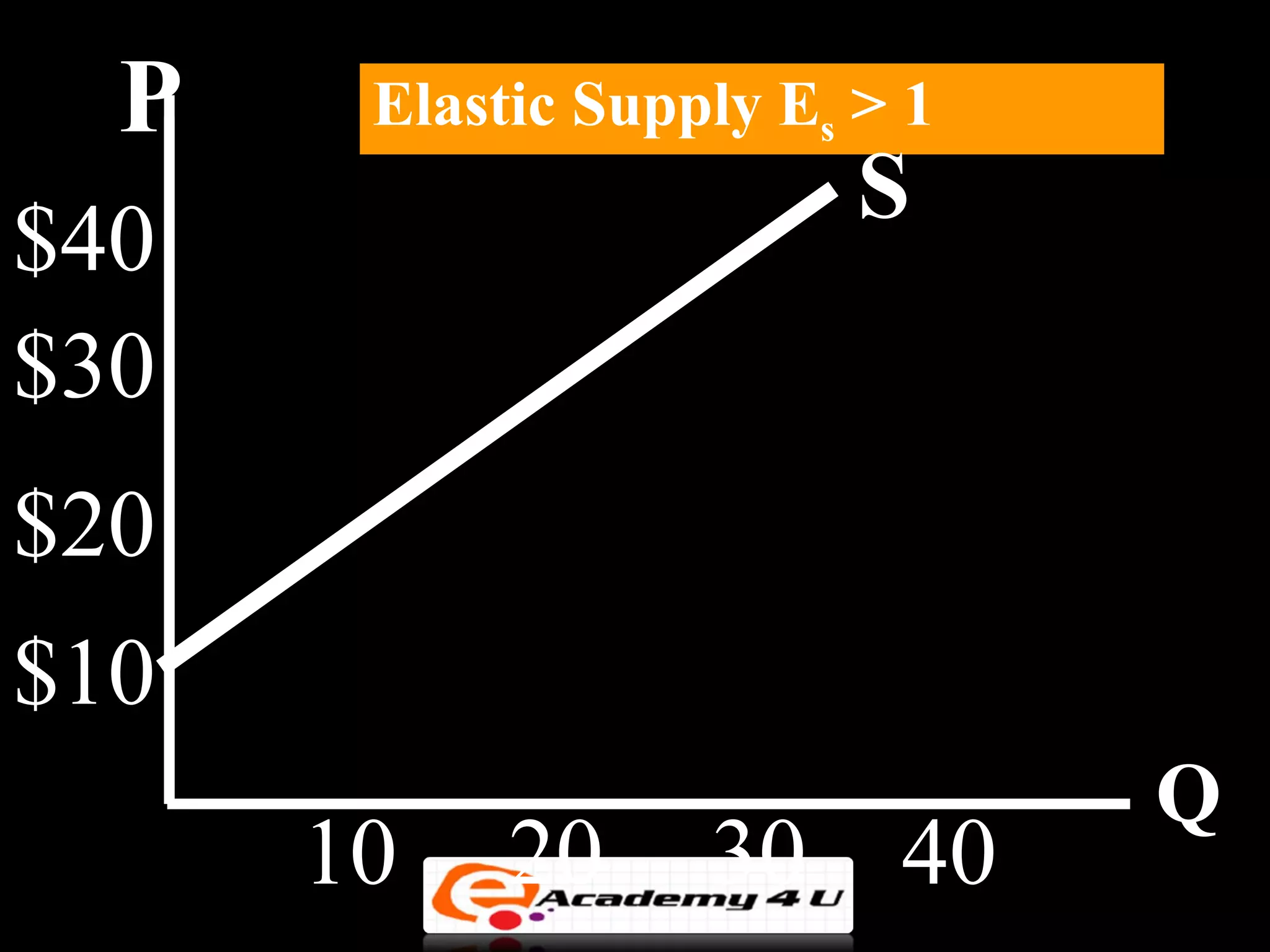

The document discusses key concepts in supply and demand including: 1. Market equilibrium is reached at the price where quantity demanded equals quantity supplied. 2. Surpluses and shortages occur when quantities demanded and supplied are not equal. 3. Demand and supply curves can shift due to various factors, impacting equilibrium price and quantity. 4. Price controls like price floors and ceilings can cause surpluses or shortages and unintended consequences. 5. Elasticity measures responsiveness of quantity to price changes and depends on availability of substitutes, budget share spent, and other factors.