Downloaded 704 times

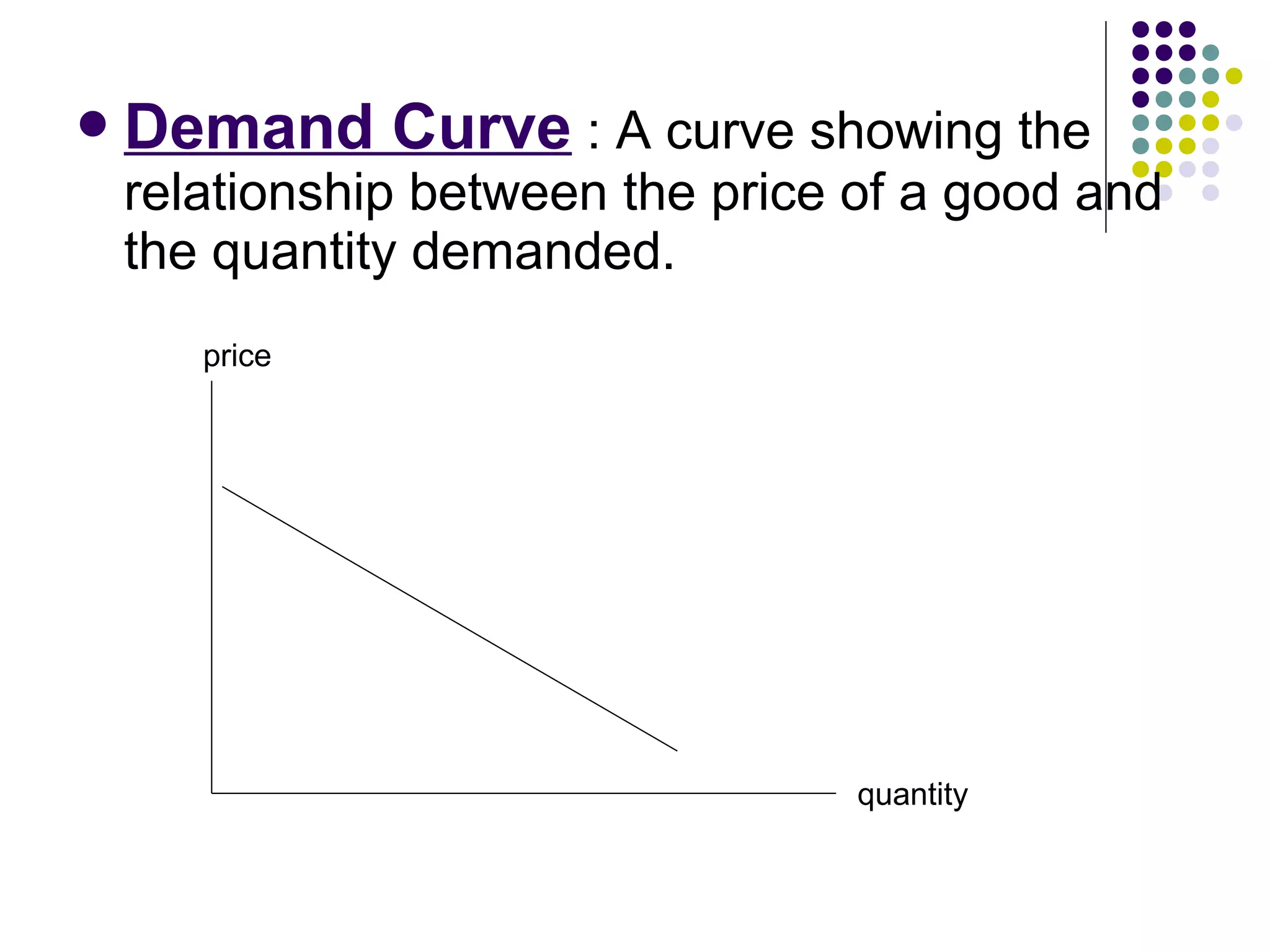

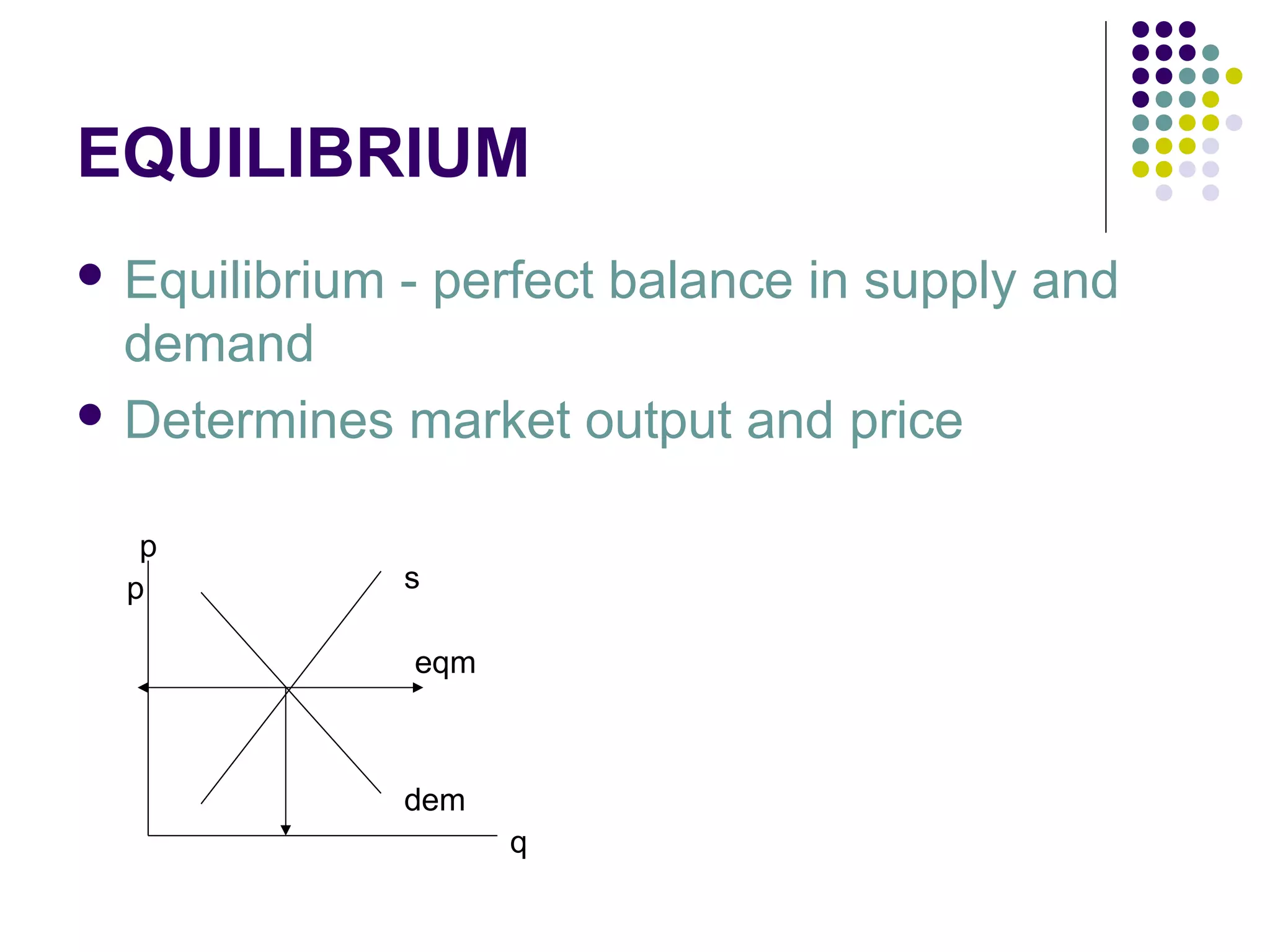

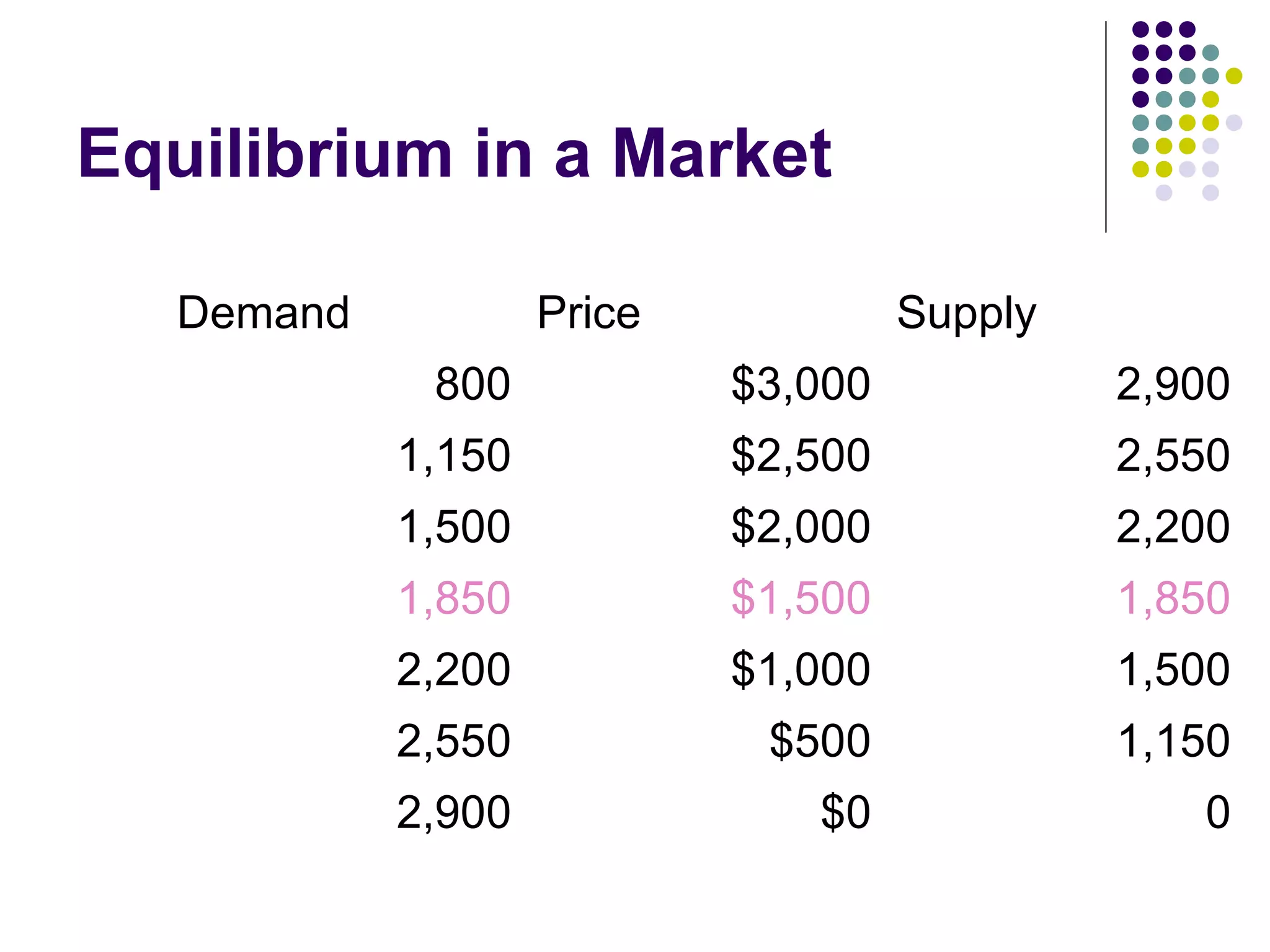

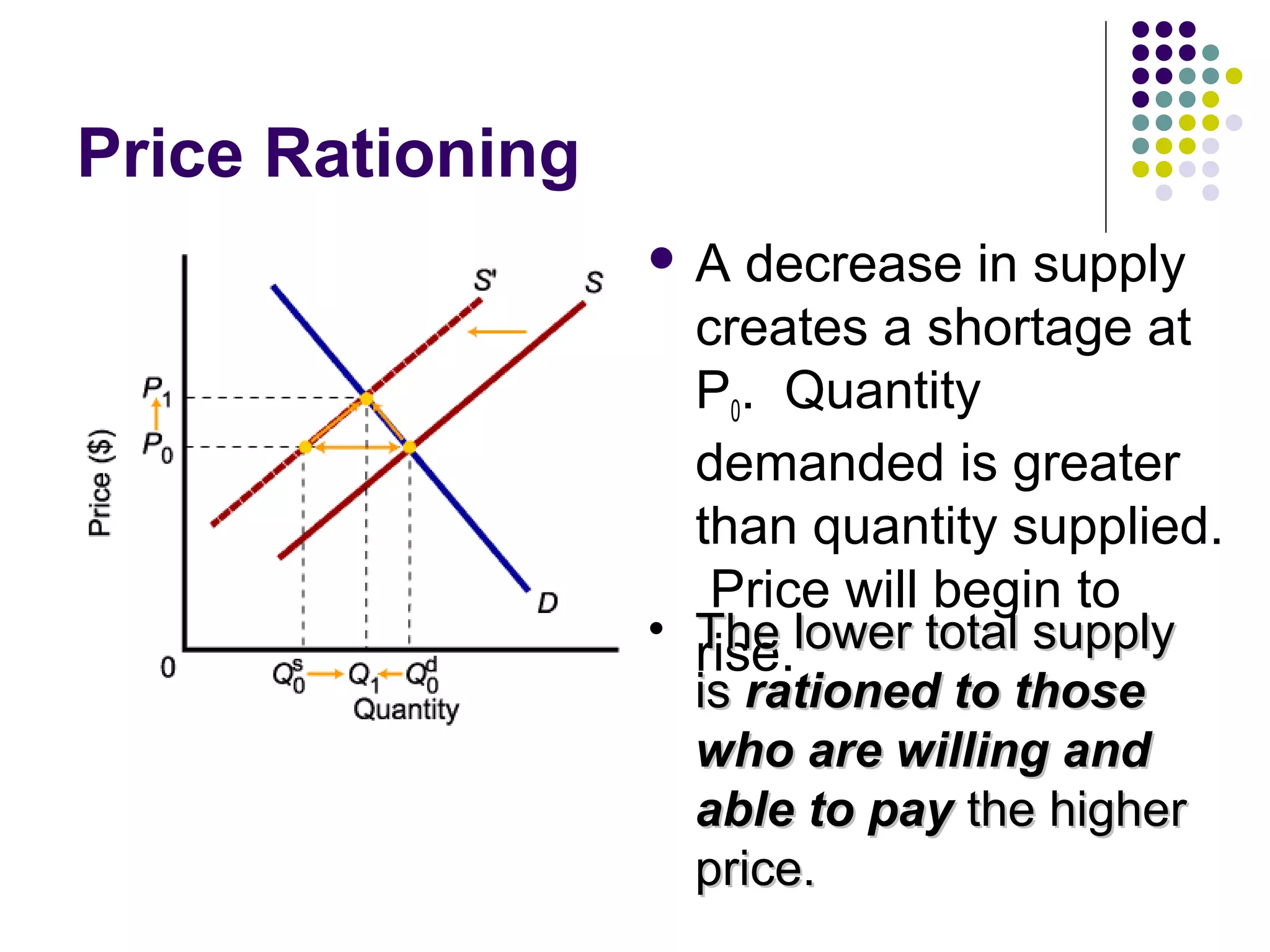

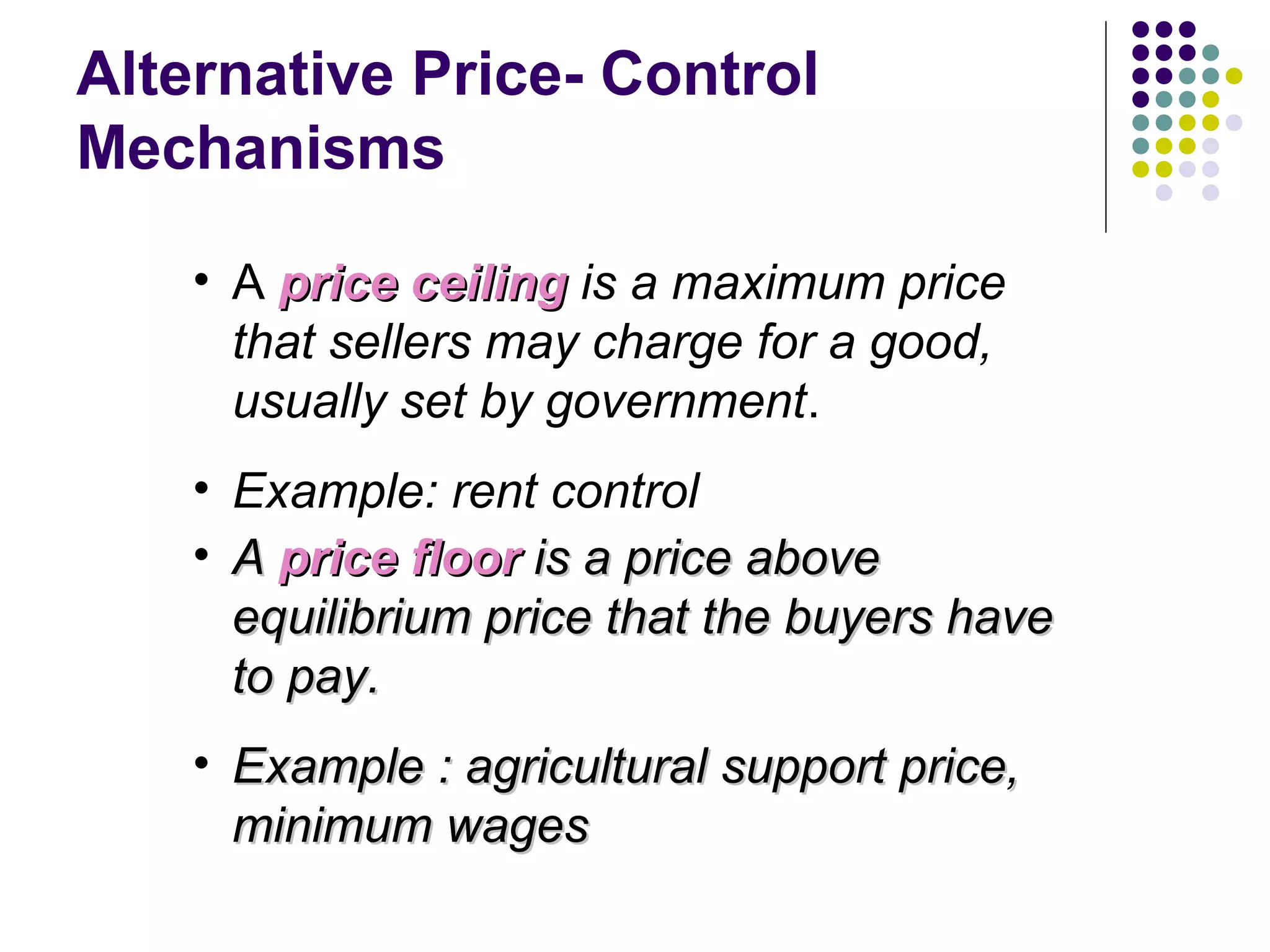

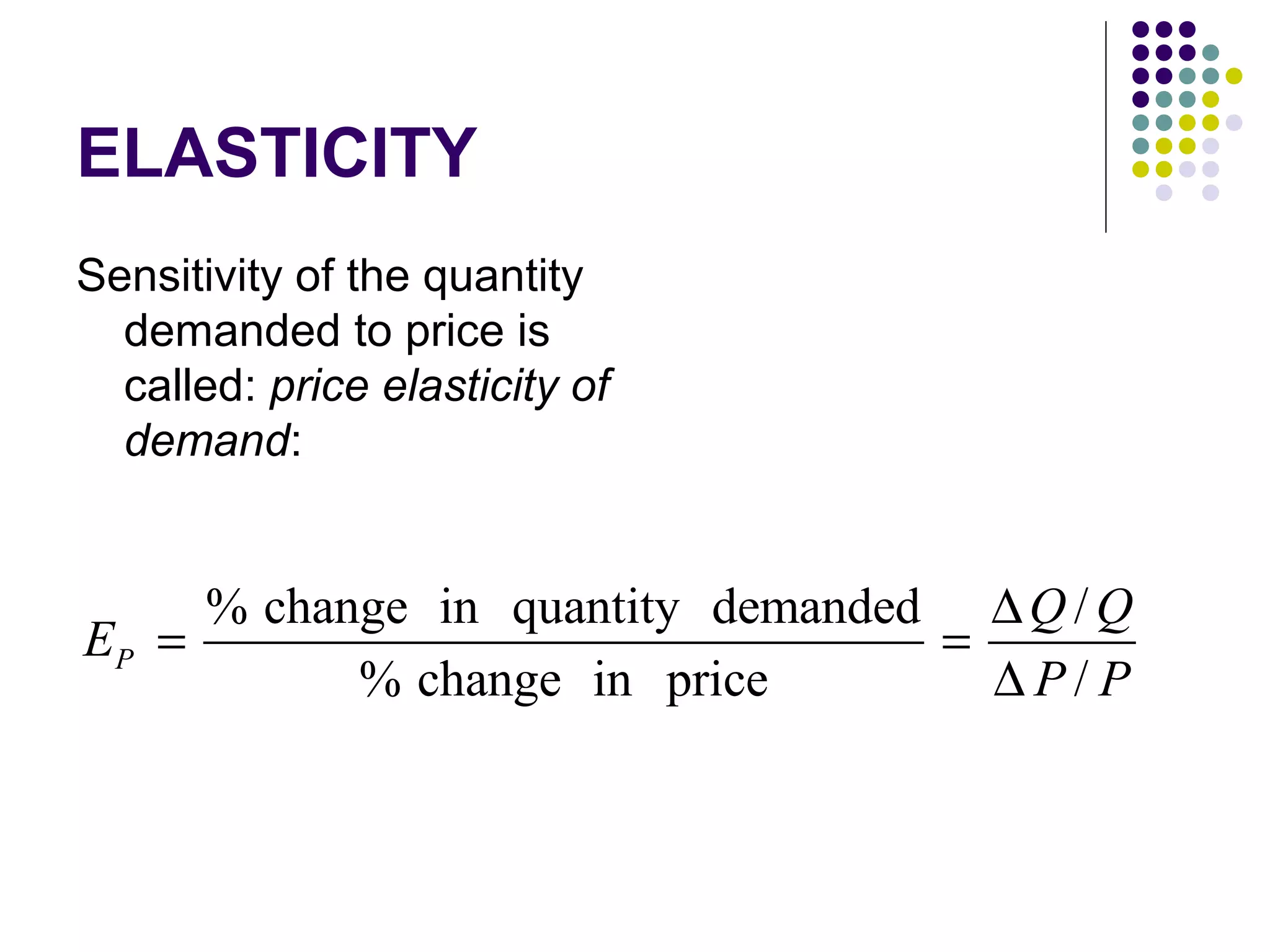

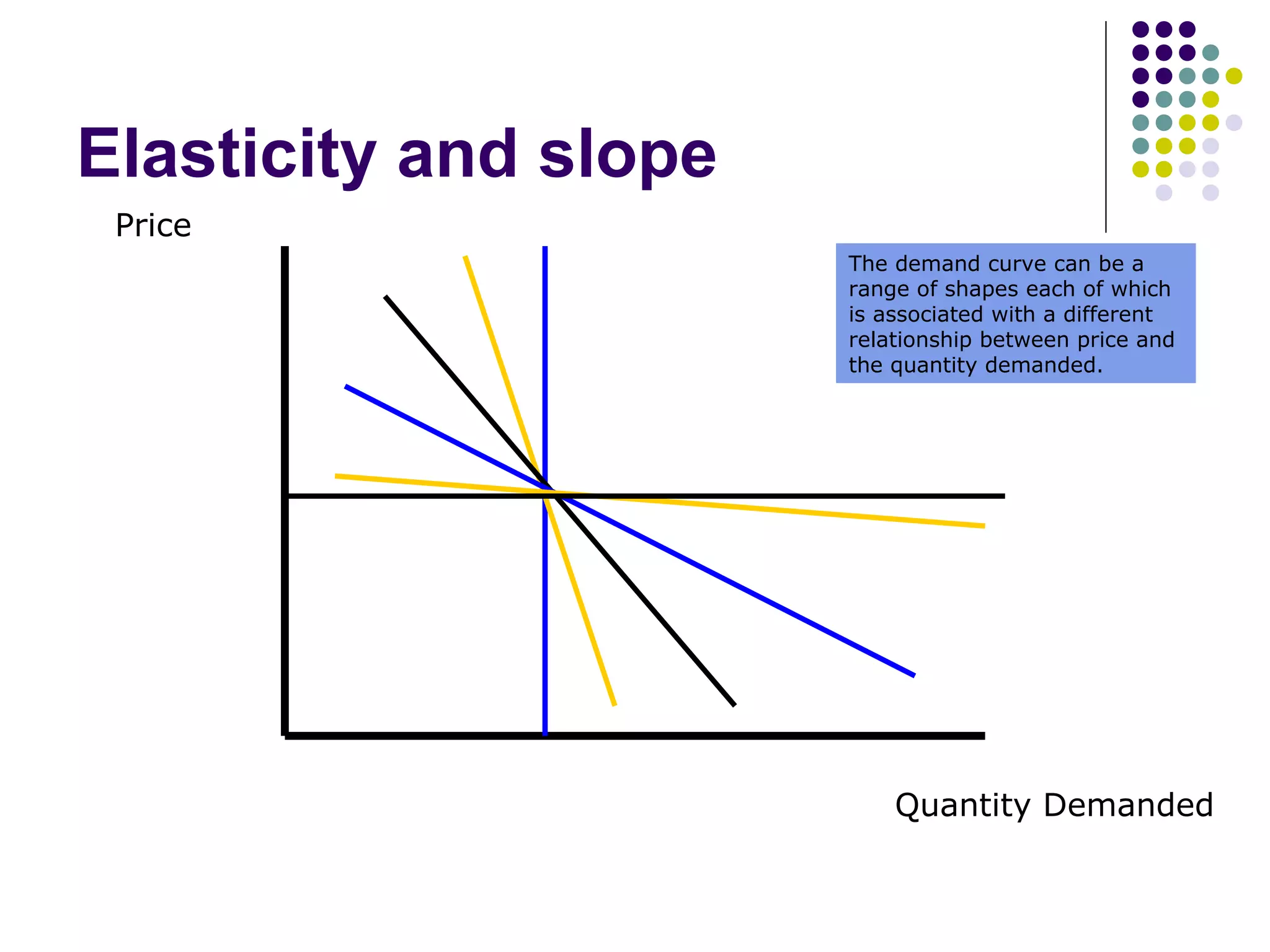

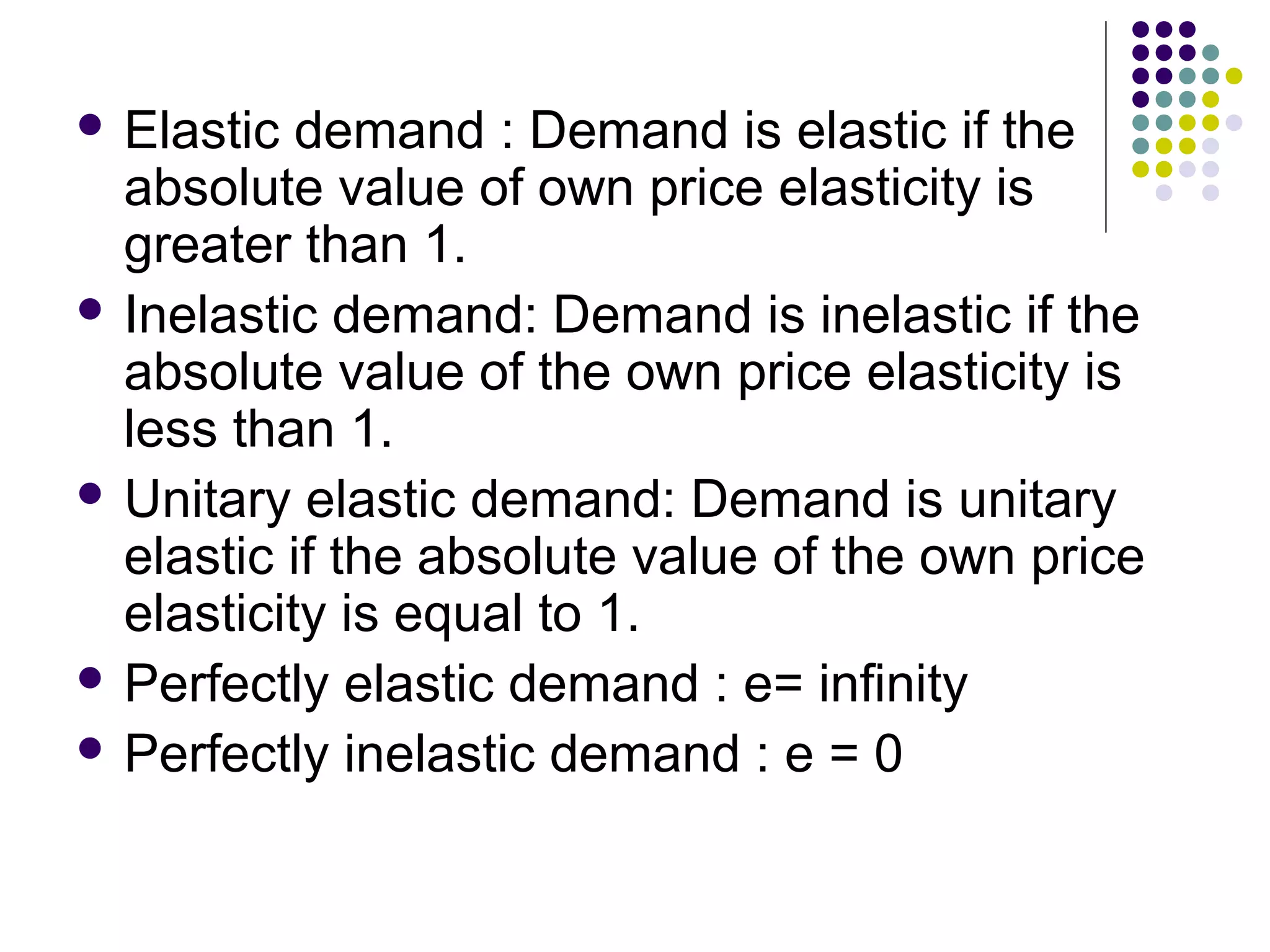

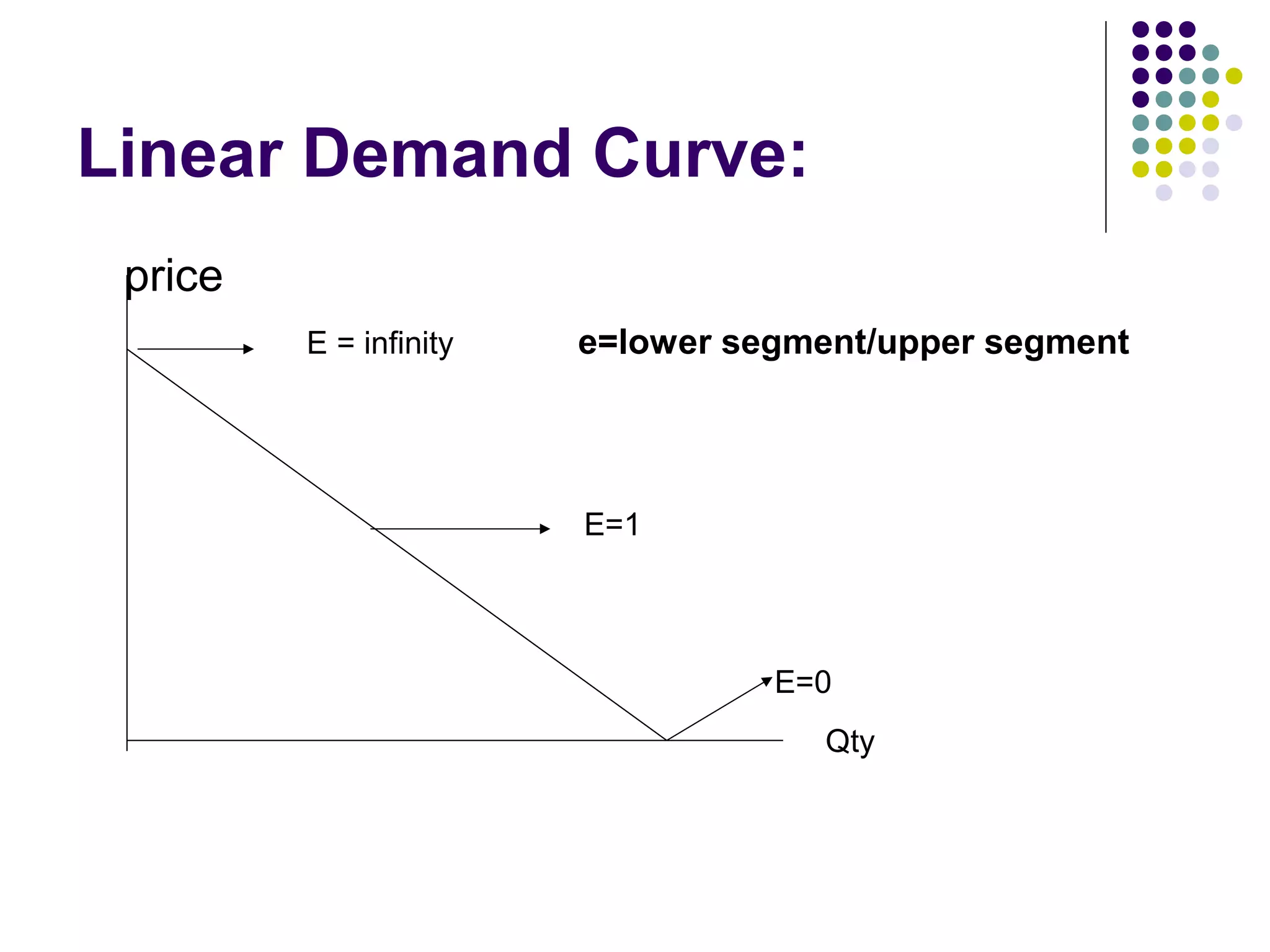

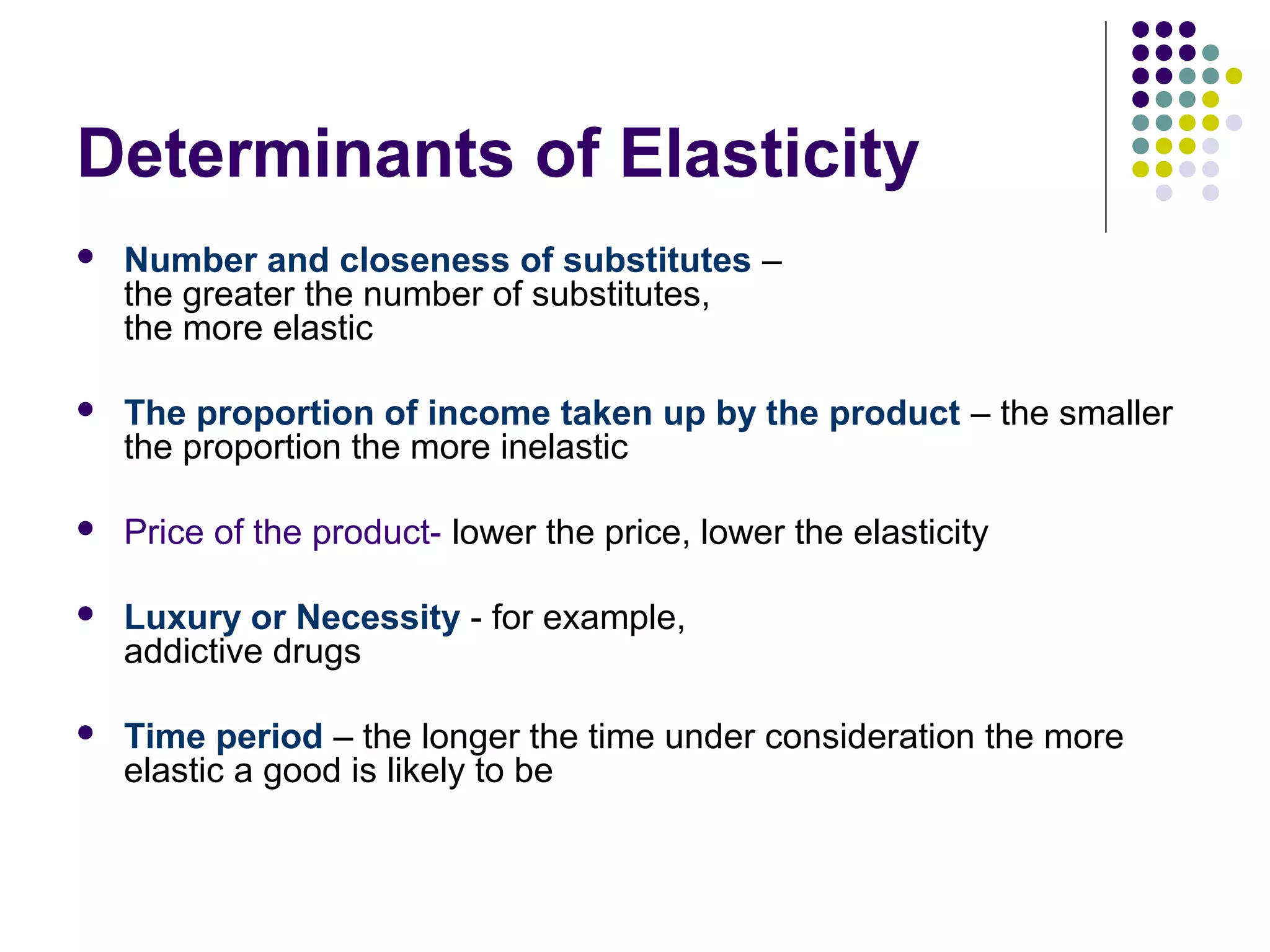

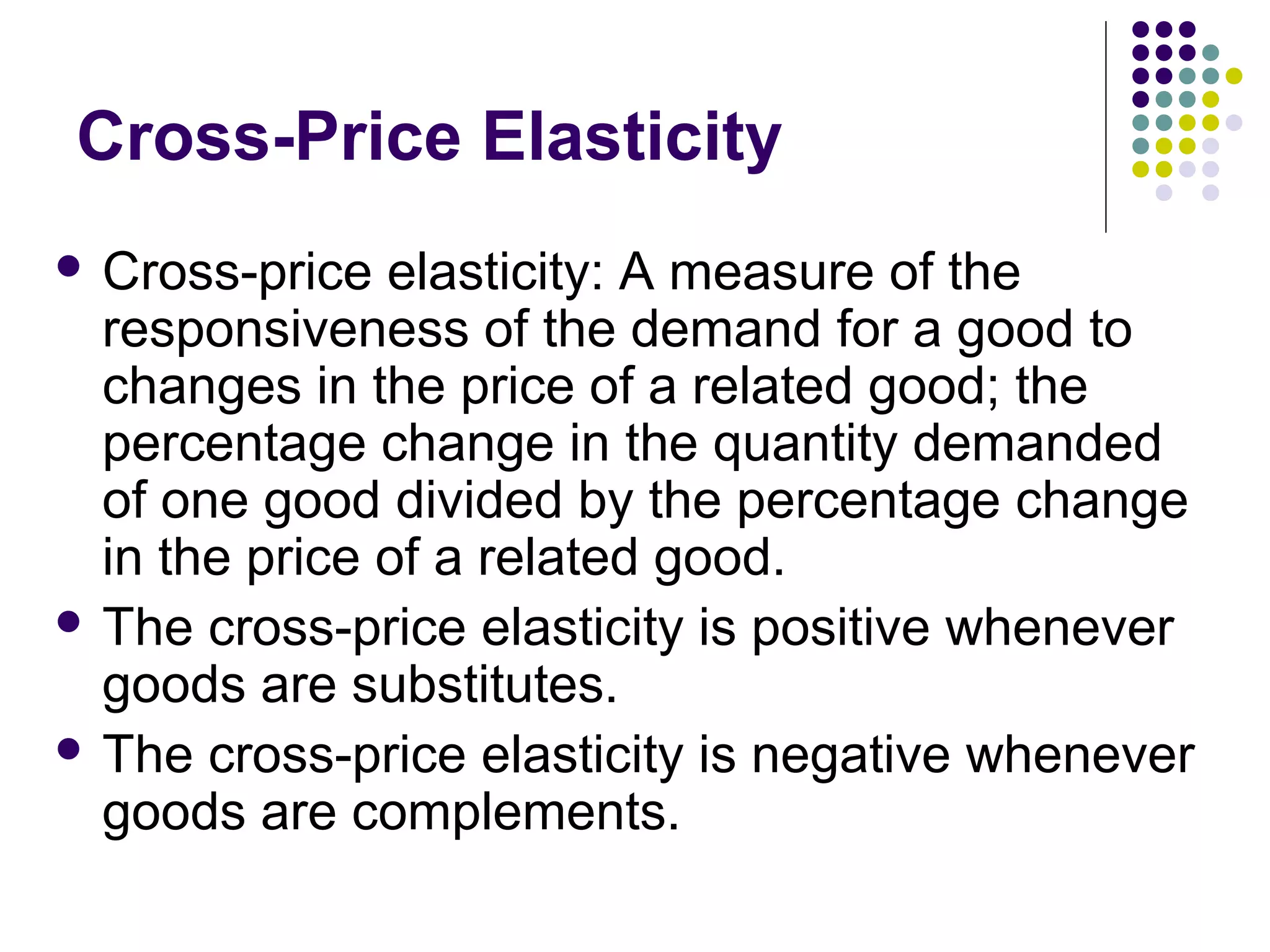

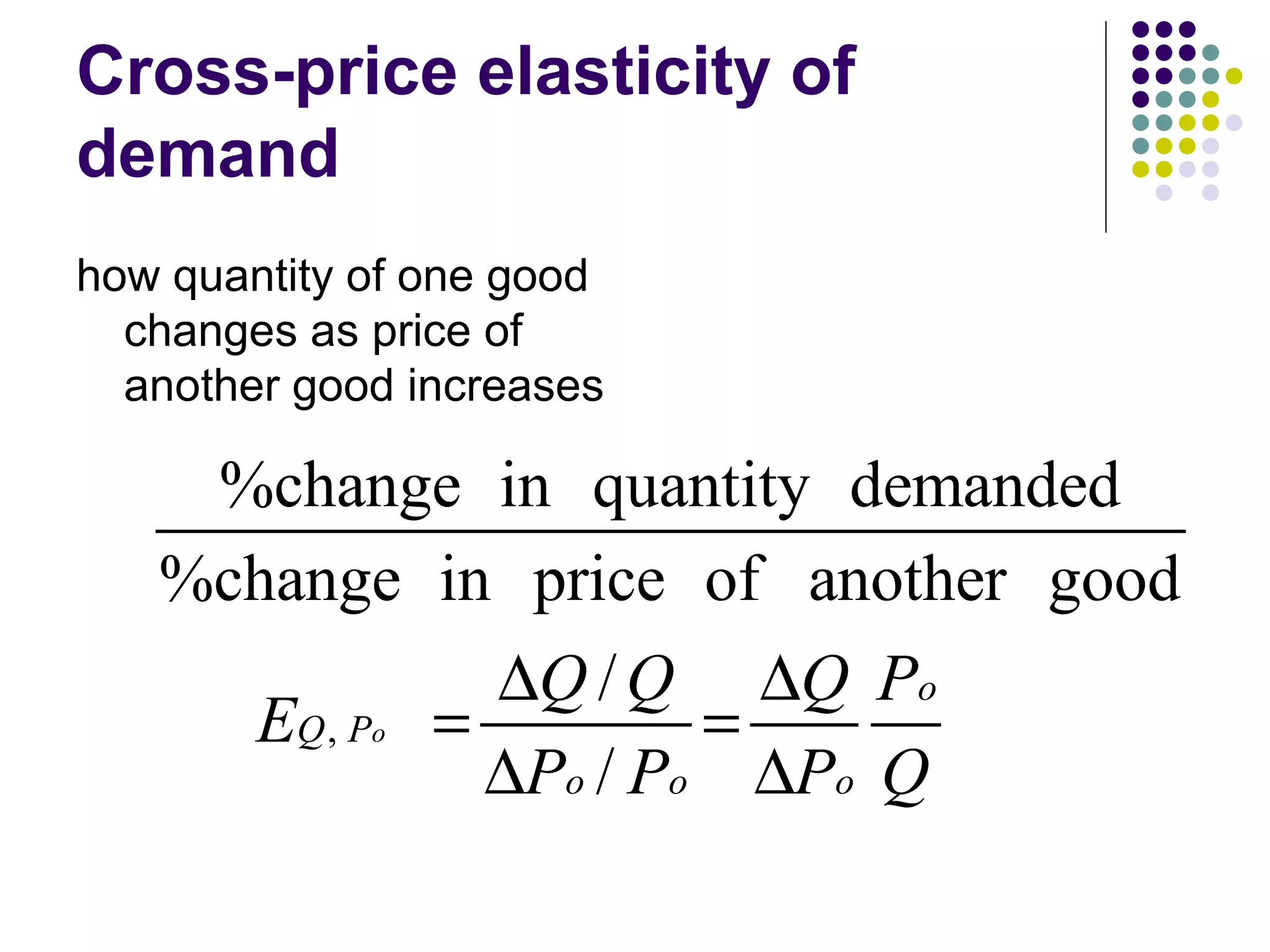

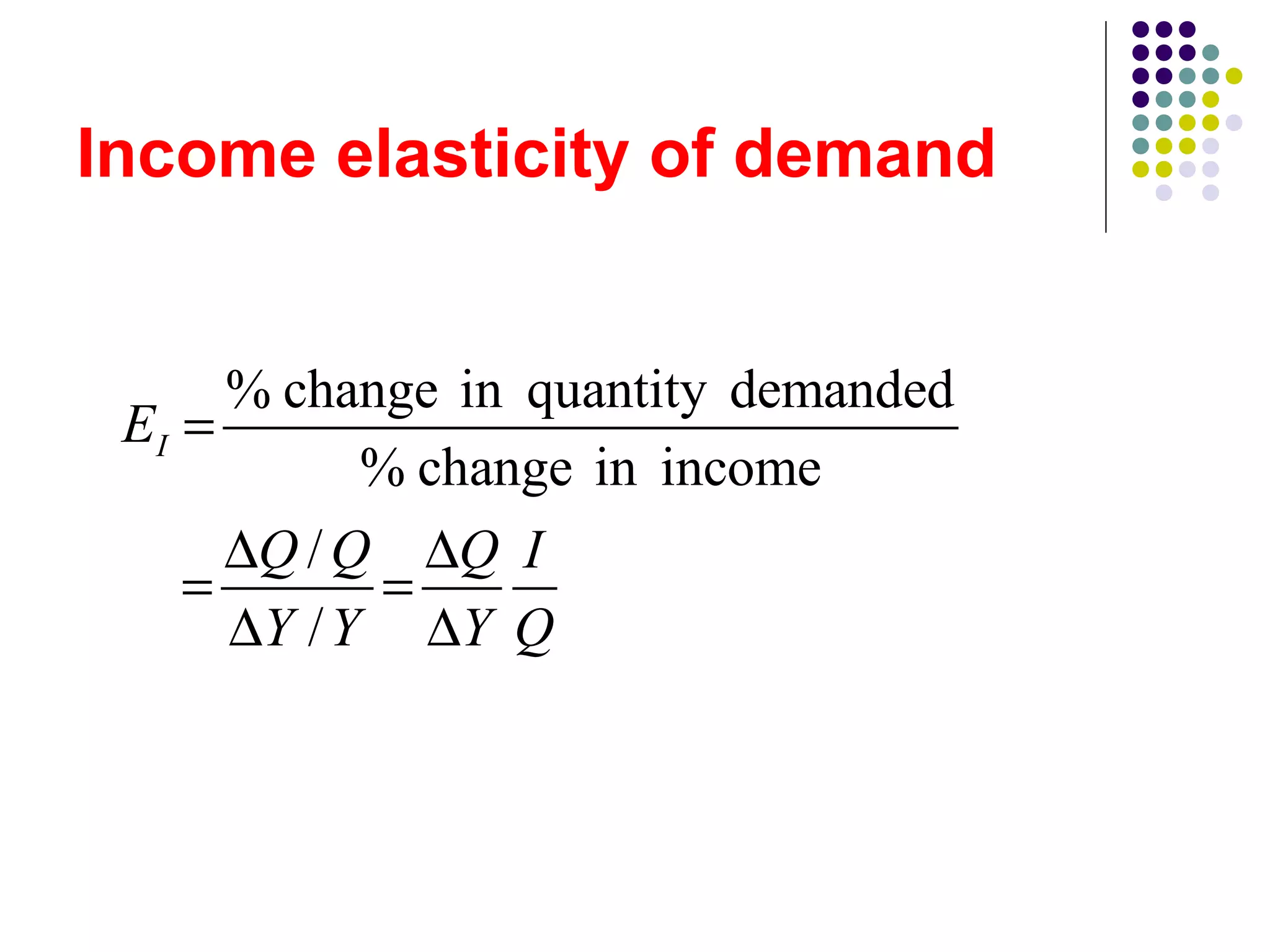

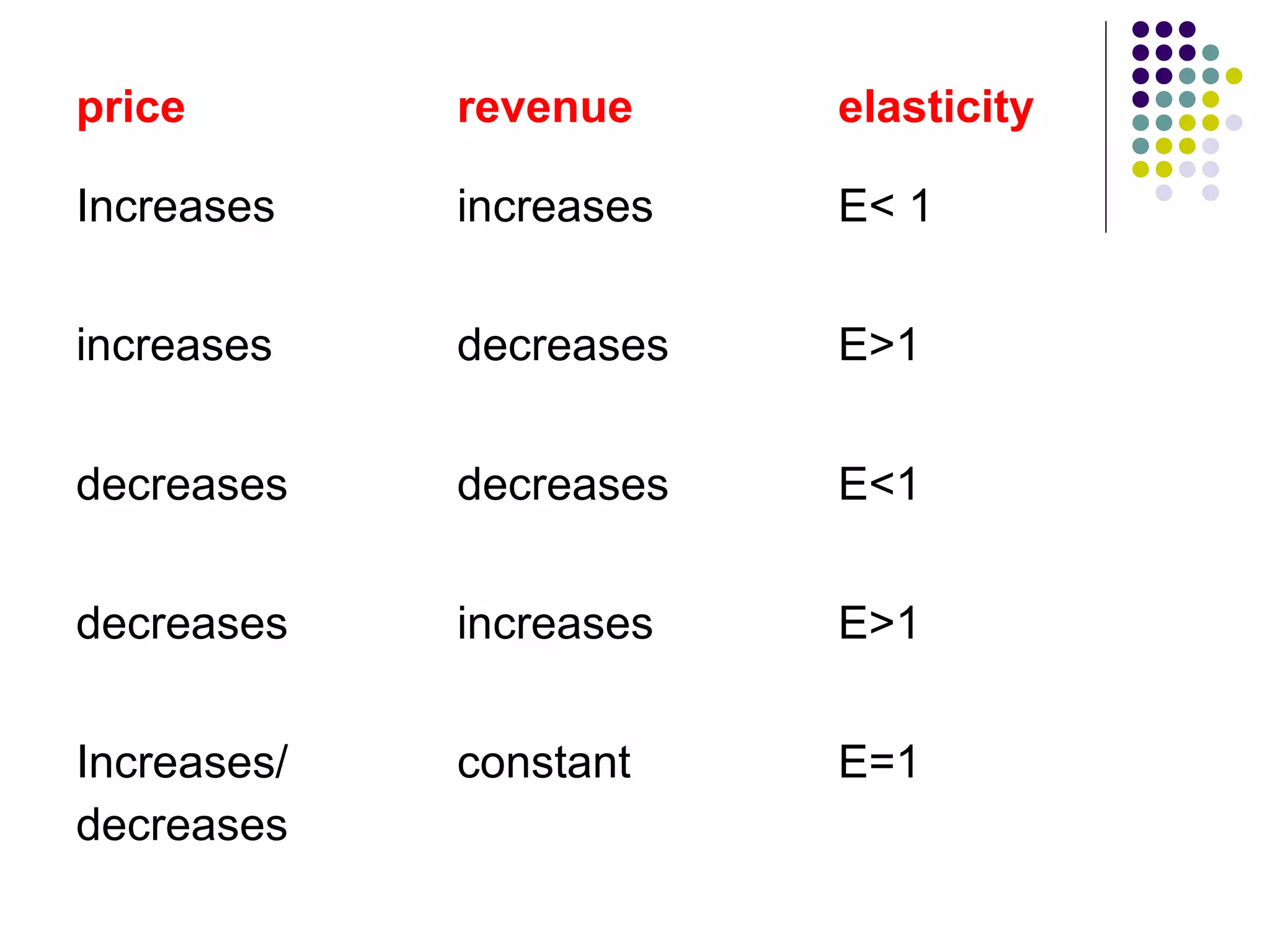

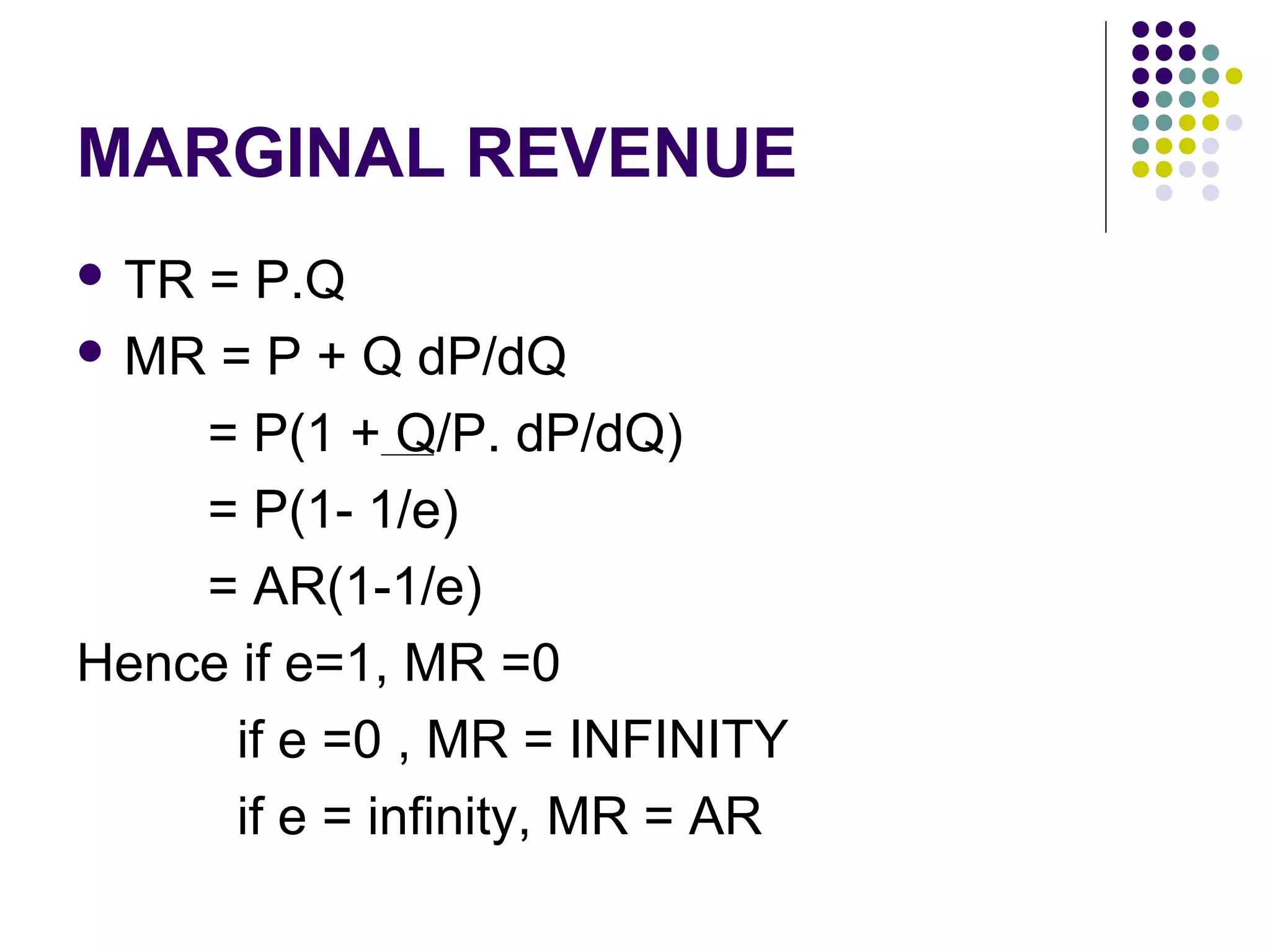

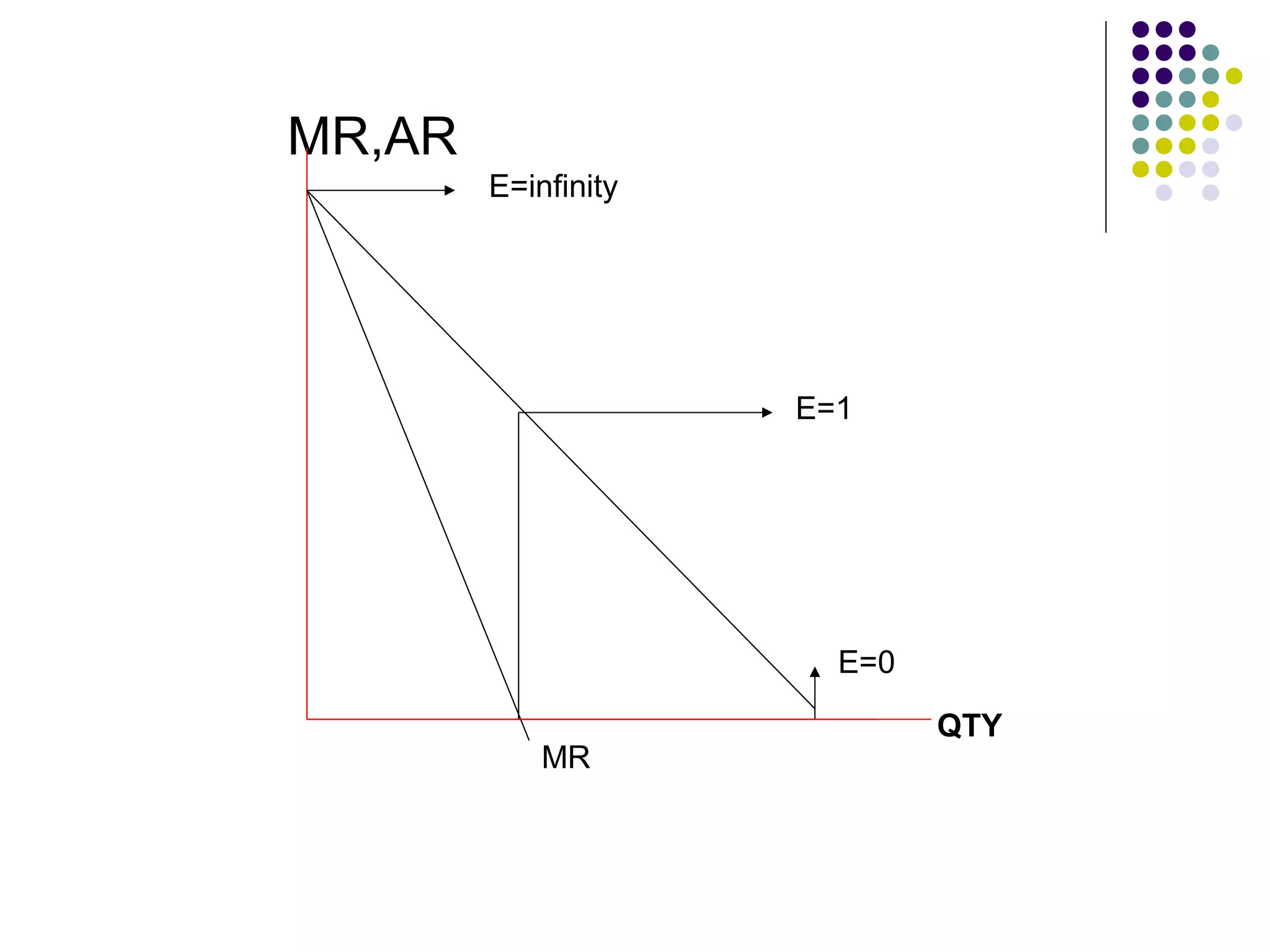

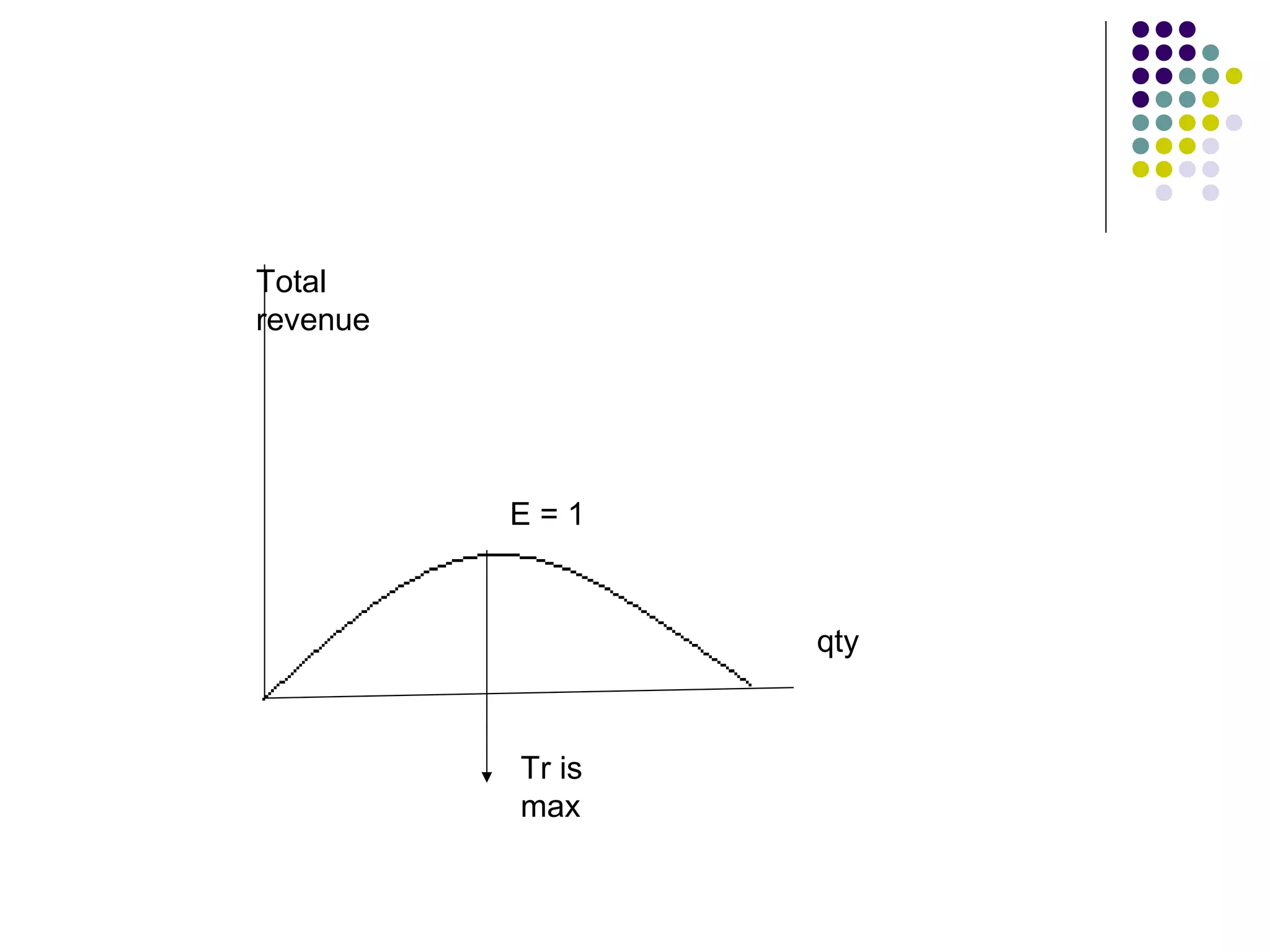

The document discusses concepts related to demand and supply, including: 1. Demand curves show the relationship between price and quantity demanded, while supply curves show the relationship between price and quantity supplied. 2. The intersection of the demand and supply curves determines the equilibrium price and quantity in a market. 3. Elasticity measures the responsiveness of demand or supply to various factors like price, income, and price of related goods. It helps to determine how demand and supply respond to changes in the market.