Downloaded 76 times

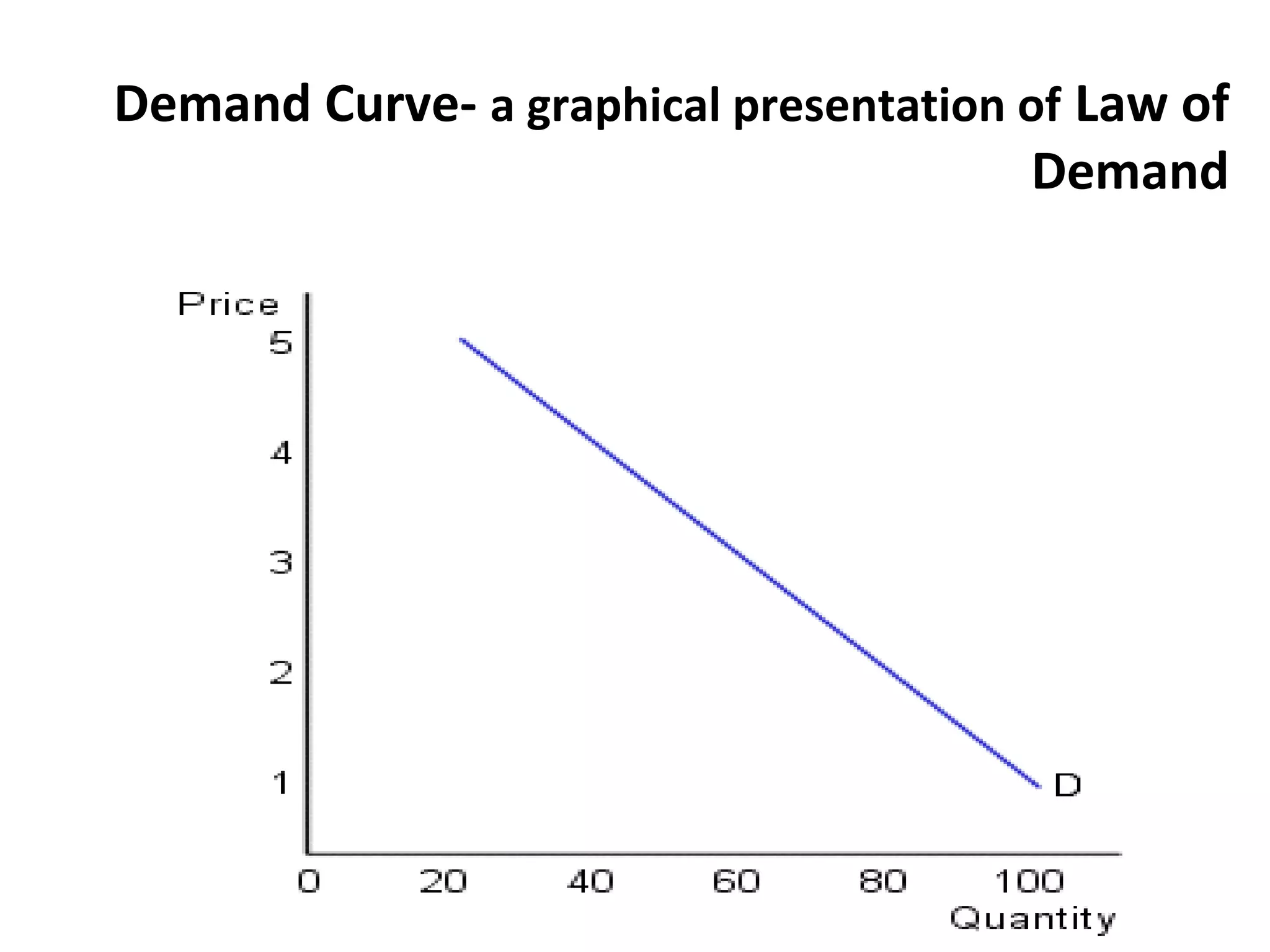

This document provides an overview of demand, supply, and elasticity concepts. It defines key terms like market, demand, supply, equilibrium, price ceilings and floors. It explains the laws of demand and supply graphically and how shifts occur due to changes in determinants. It also defines different types of elasticity including price elasticity of demand and supply, income elasticity, and cross price elasticity. Formulas for computing elasticity coefficients are provided.