Downloaded 709 times

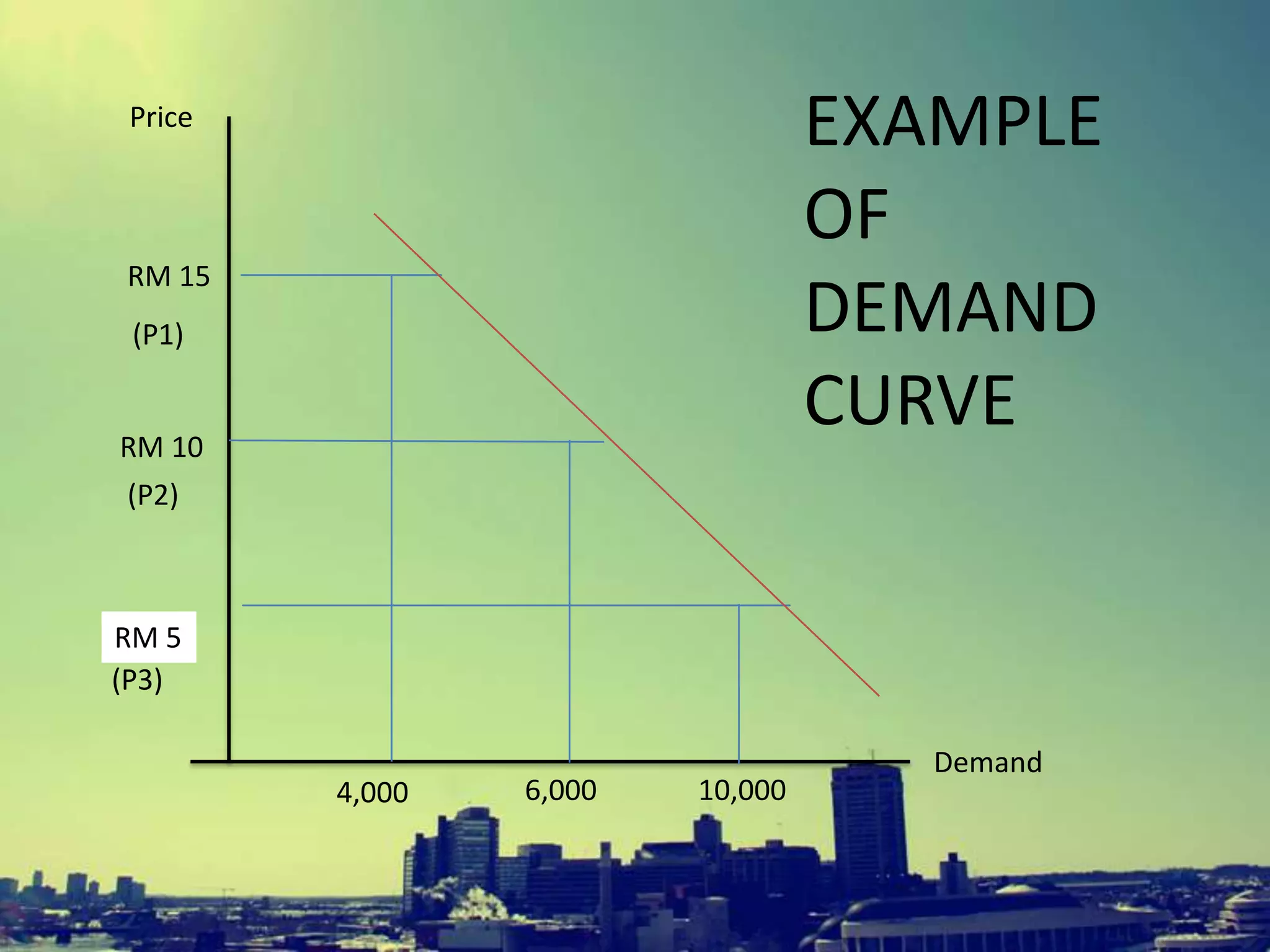

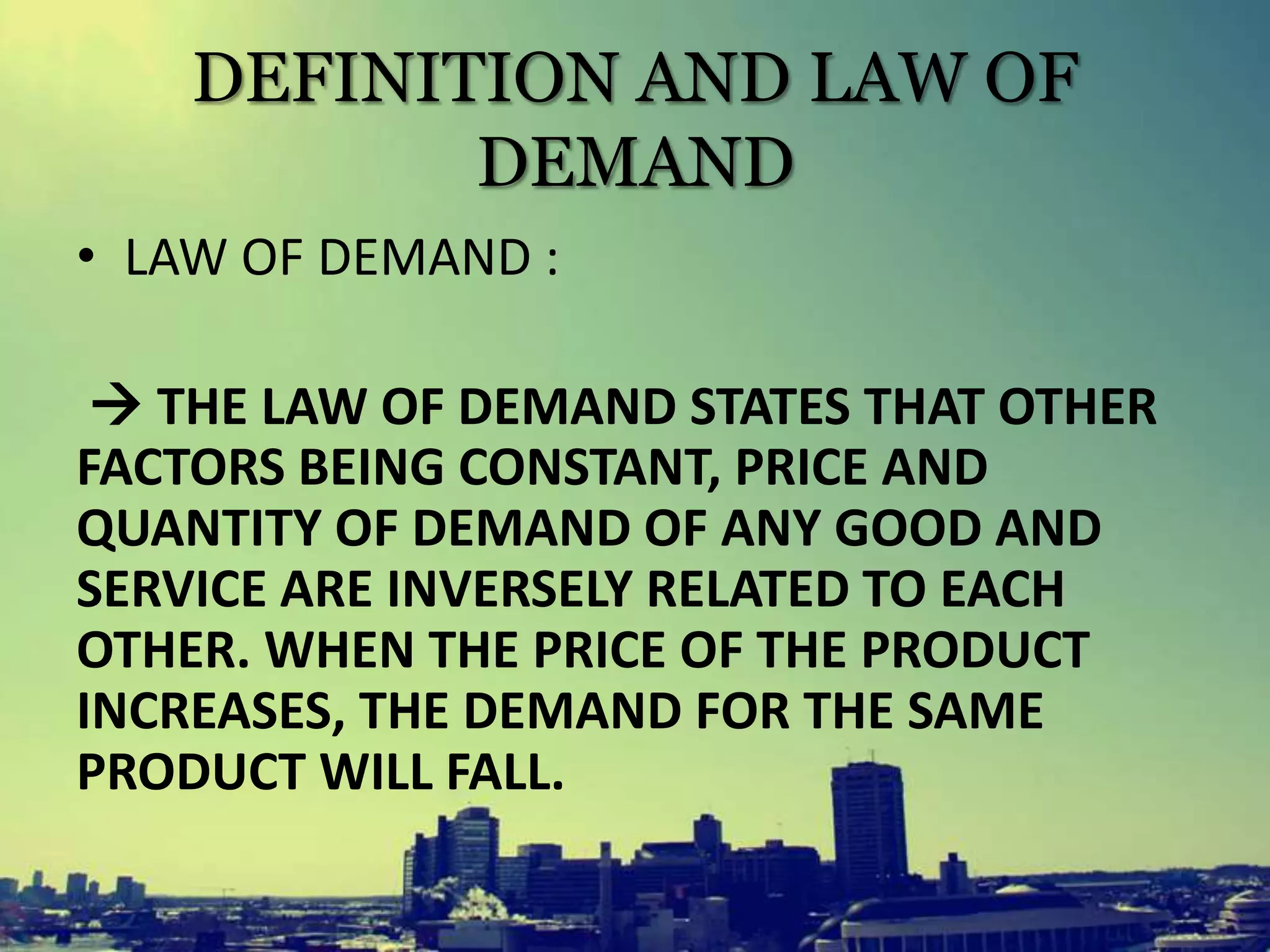

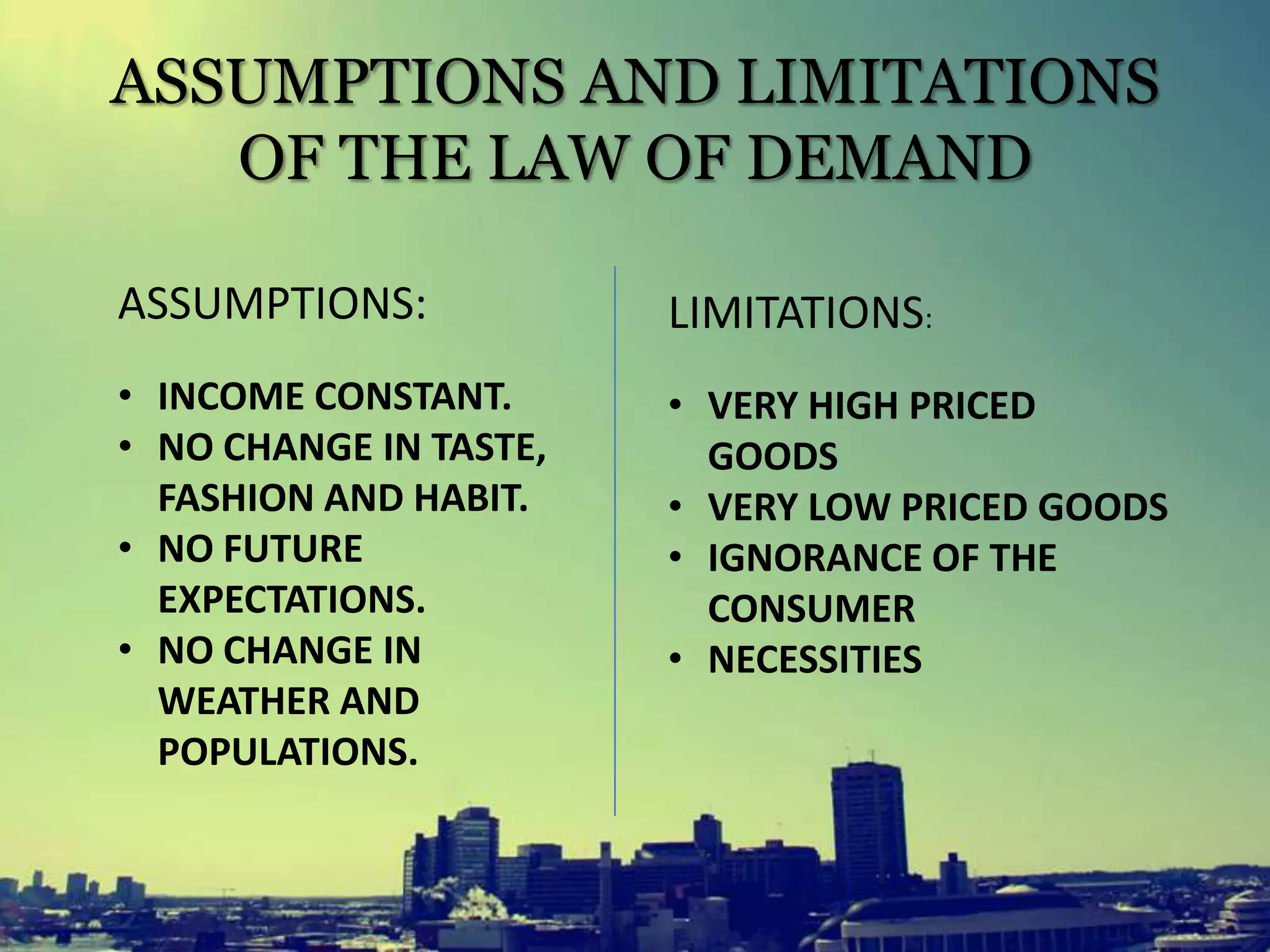

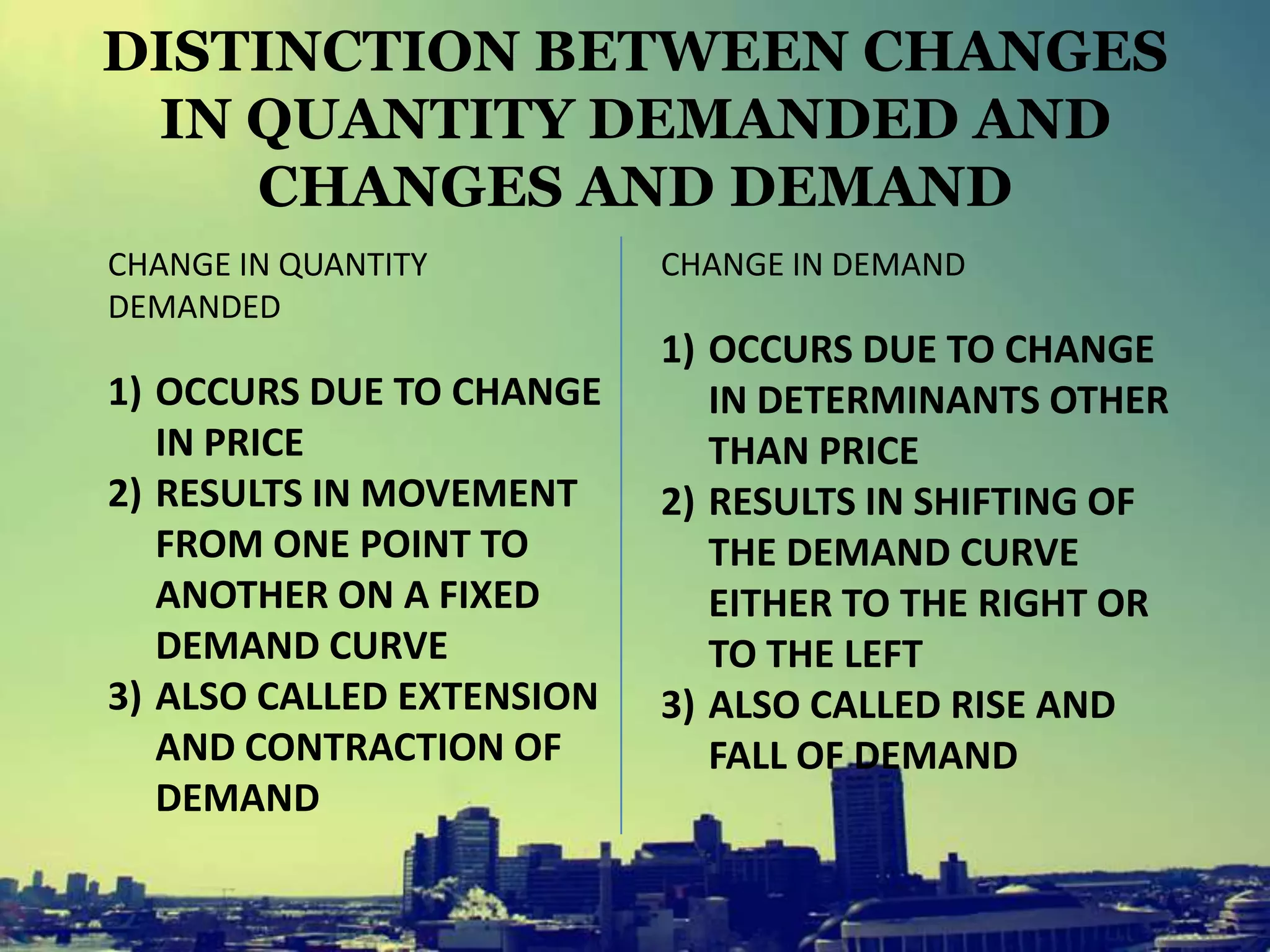

This document defines key economic concepts related to demand and supply, including: - Demand is the desire and ability to purchase goods, defined by a demand schedule and curve showing the relationship between price and quantity demanded. - The law of demand states that as price increases, quantity demanded decreases, assuming other factors remain constant. - Supply is the quantity of a good producers are willing to provide at a given price, defined by a supply curve showing the positive relationship between price and quantity supplied. - Determinants like tastes, income, and expectations can cause shifts in the demand curve, while costs and technology can shift the supply curve.