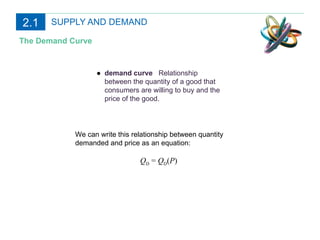

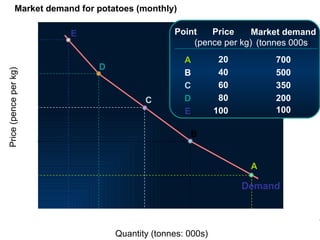

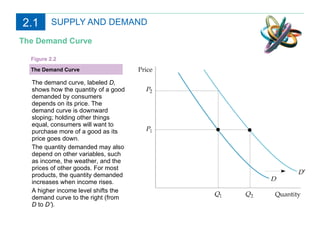

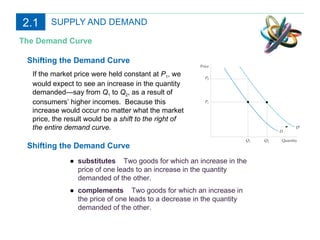

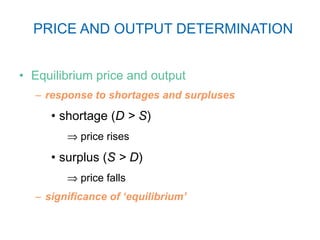

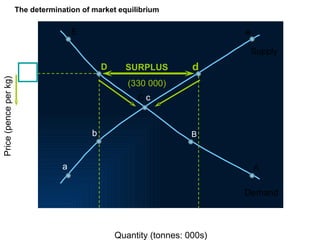

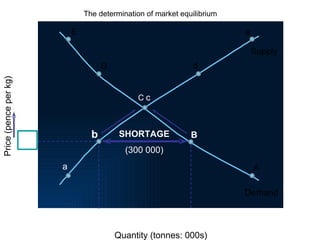

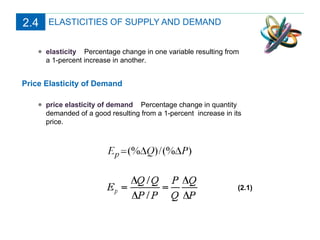

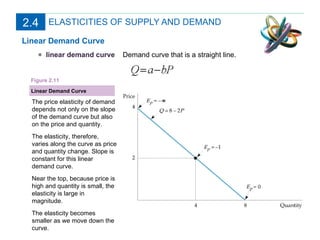

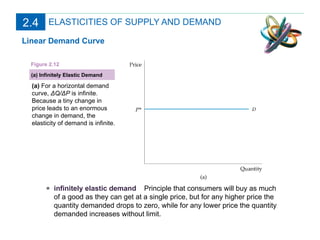

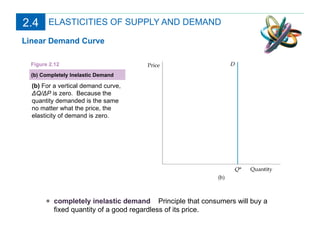

This document discusses key concepts related to supply and demand, including: 1) It defines supply and demand curves, and how they relate quantity supplied/demanded to price. 2) It explains how equilibrium price and quantity are determined by the intersection of supply and demand. 3) It discusses factors that can cause supply and demand curves to shift, leading to new equilibrium prices and quantities. 4) It introduces concepts of price elasticities of supply and demand.