Download as PDF, PPTX

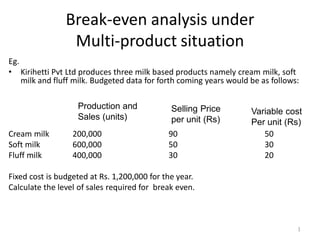

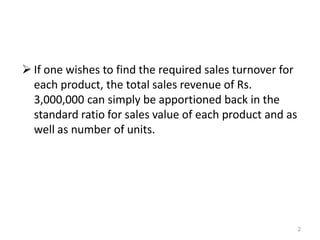

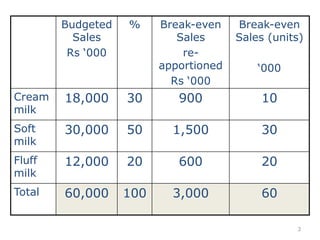

The document discusses break-even analysis for a company that produces three milk products: cream milk, soft milk, and fluff milk. It provides budgeted production, selling price, and variable cost data for each product. The total fixed cost for the year is budgeted at Rs. 1,200,000. To calculate the break-even point, the total sales revenue of Rs. 3,000,000 is apportioned to each product based on its percentage of total sales value and units. This results in break-even sales levels of Rs. 900,000 for cream milk, Rs. 1,500,000 for soft milk, and Rs. 600,000 for fluff milk.