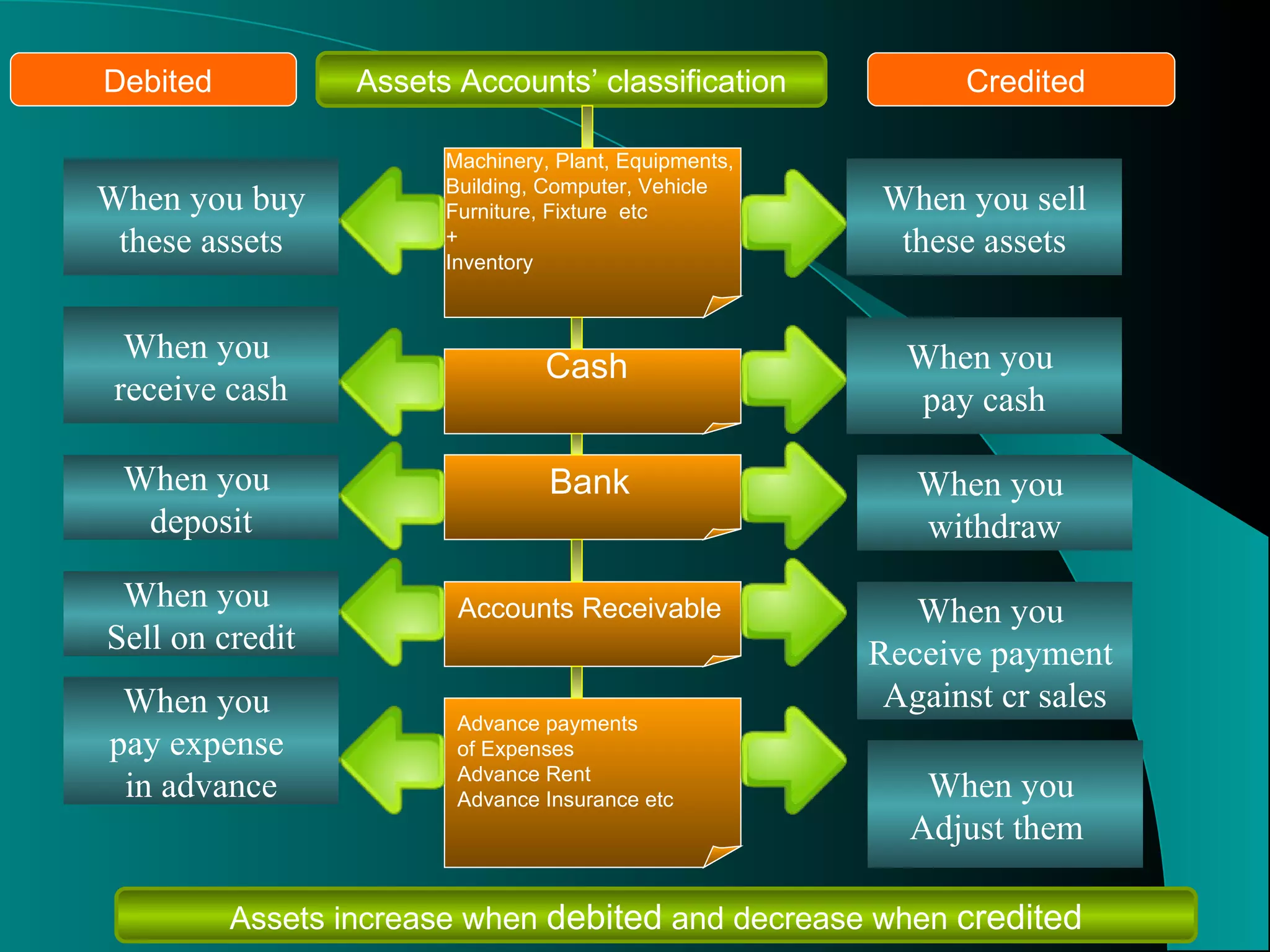

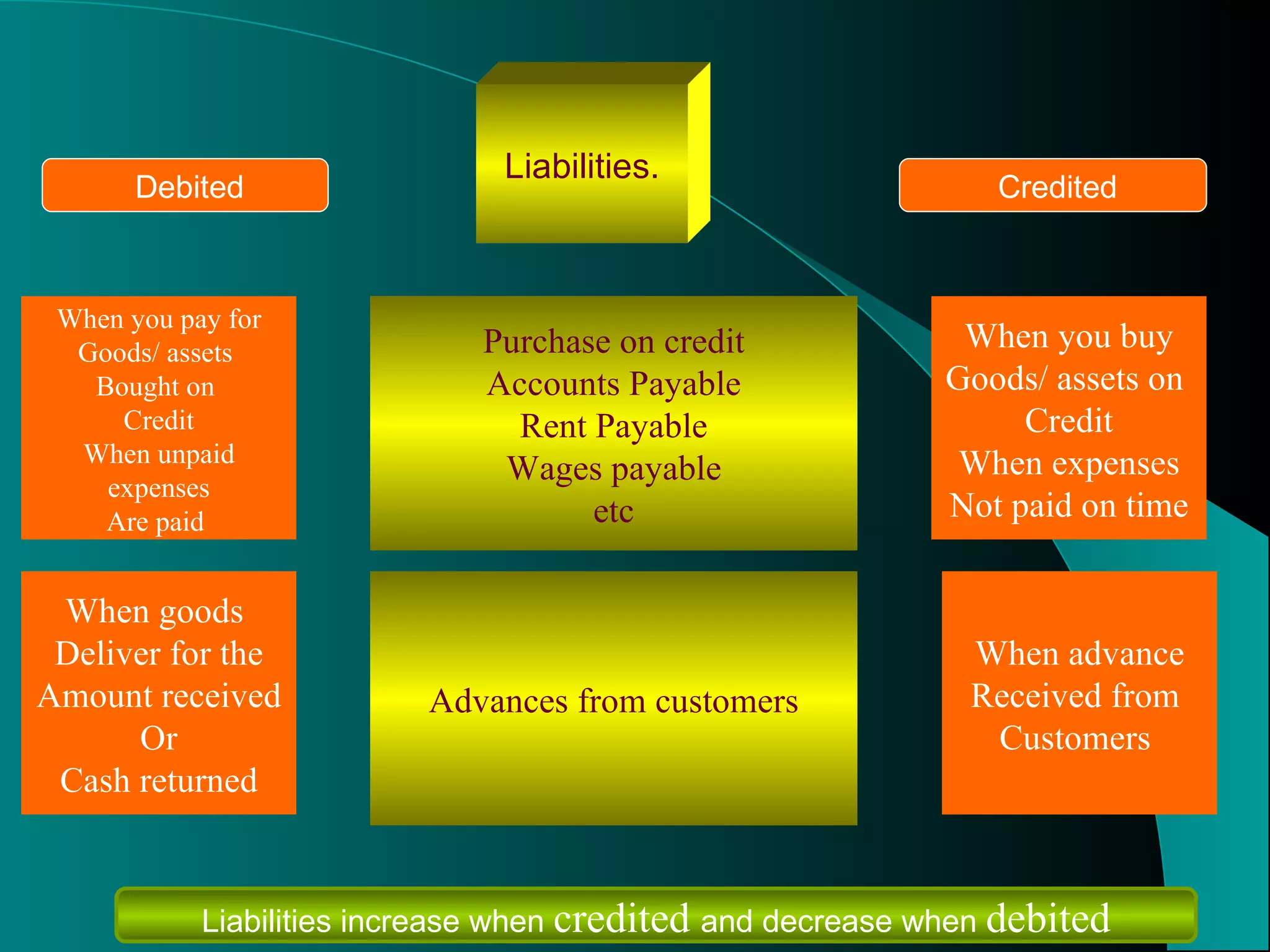

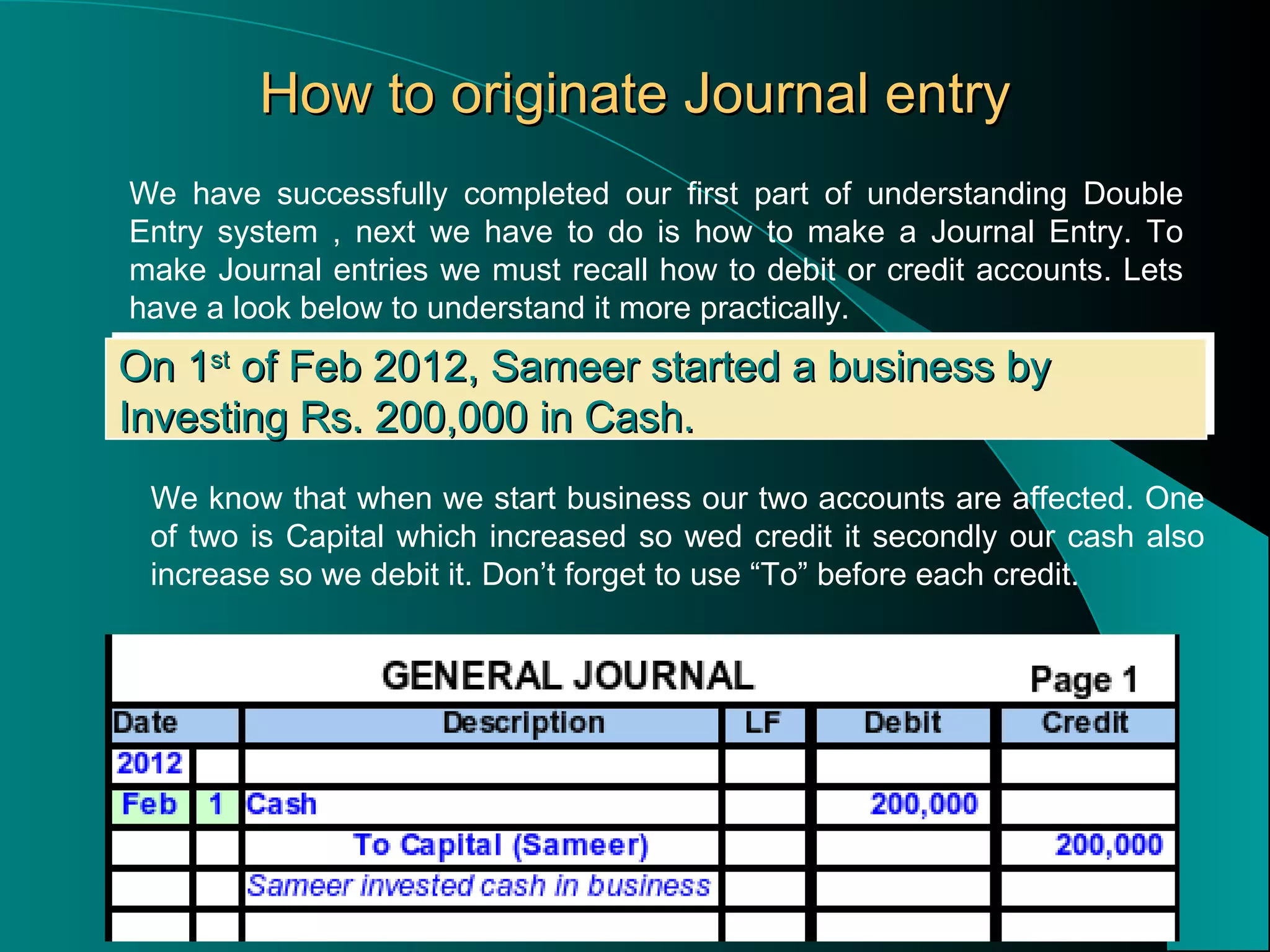

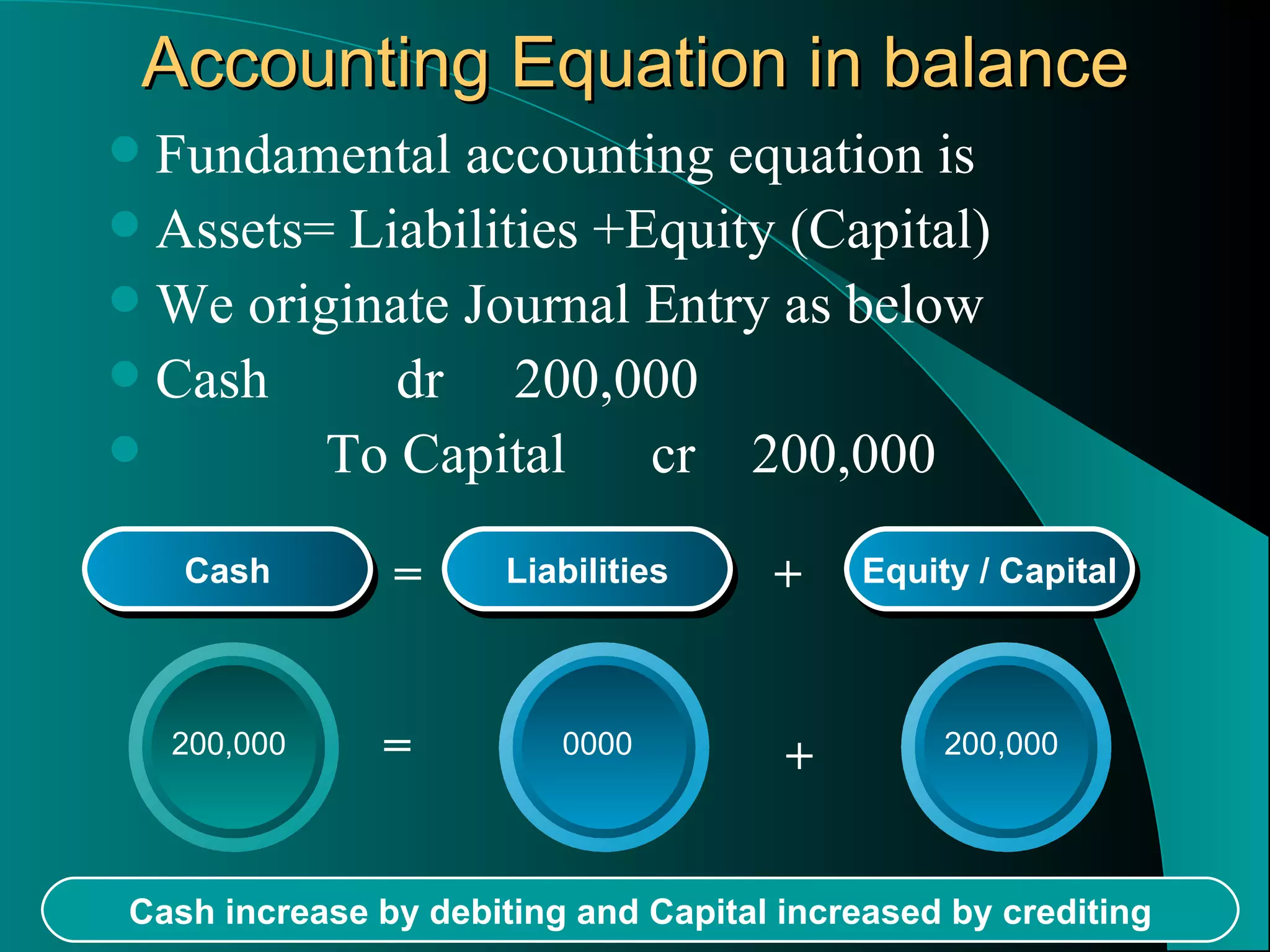

The document explains the double-entry accounting system, emphasizing that every transaction involves both a debit and a credit, ensuring the accounting equation (assets = liabilities + equity) remains balanced. It details the classification of accounts, including assets, liabilities, equity, revenue, and expenses, along with their respective rules for debits and credits. Additionally, the document provides examples of journal entries to illustrate the practical application of these principles in accounting.