Download to read offline

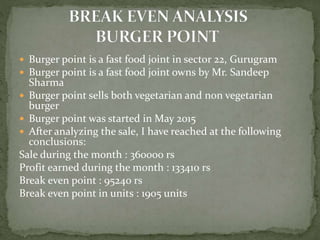

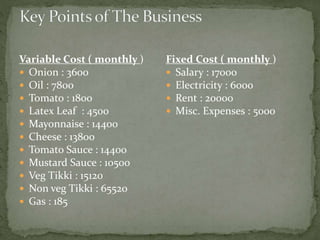

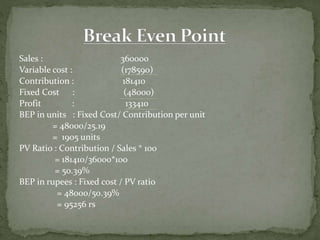

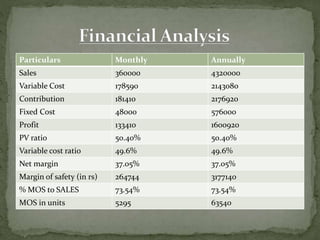

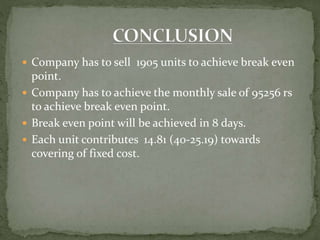

Burger Point is a fast food joint in Gurugram, India owned by Mr. Sandeep Sharma that sells vegetarian and non-vegetarian burgers. An analysis of their monthly sales of Rs. 360,000 found that their profit was Rs. 133,410, break-even point in units was 1,905, and break-even point in rupees was Rs. 95,240. Their variable costs include ingredients like onions, oil, and sauces, while fixed costs include salaries, electricity, and rent.