Downloaded 5,851 times

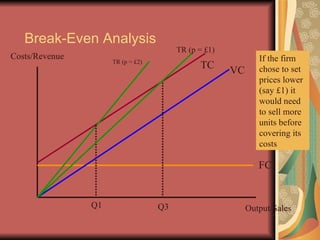

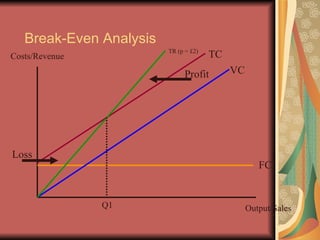

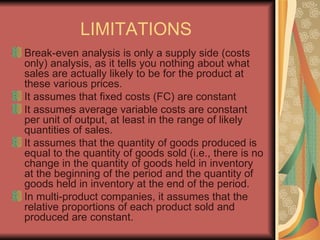

The document discusses break-even analysis, which helps determine the sales volume needed for a business to start making a profit by calculating fixed costs, variable costs, total costs, and total revenue. It also explains how to find the break-even point and the impact of pricing strategies on profitability, along with the limitations of this analysis. The conclusion distinguishes break-even analysis from other managerial tools like flexible budgets and standard costs.