Downloaded 325 times

![18

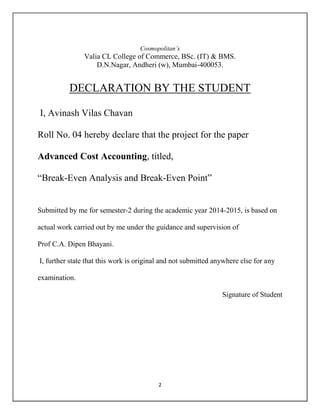

Definition Of Break Even Point:

Break-even point is the level of sales at which profit is zero. According to this definition, at

break-even point sales are equal to fixed cost plus variable cost. This concepts is further

explained by the following equation:

[Break-even sales= fixed cost + variable cost]

The break-even point can be calculated using either the equation method or margin method.

These two method are equivalent:

Equation method:

The equation method center on the contribution approach to the income statement.

The format of this statement can be expressed is equation form as follow:

Profit = (Sales – Variable expenses) – Fixed Expenses

Rearranging this equation slightly yields the following equation, which is widely used in cost

volume profit (CVP) analysis:

Sales = Variable expenses + Fixed Expenses + Profit

According to the definition of break-even point, break-even point is the level of sales where

profits are zero. Therefore the break-even point can be computed by finding that point where

sales just equal the total of the variable expenses plus fixed expenses and profit is zero.

Example:

For example we can use the following data to calculate break-even point.

1. Sales prices per units = 250 Rs.

2. Variable cost per unit = 150Rs.

3. Total fixed expenses = 35000Rs.

Calculate break even point.](https://image.slidesharecdn.com/cosmopolitan-150312113114-conversion-gate01/85/Break-Even-Analysis-and-Break-Even-Point-18-320.jpg)

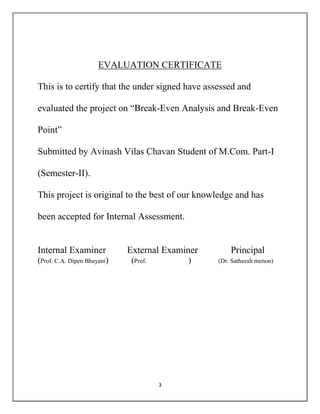

![19

Calculation:

Sales = Variable Expenses + Fixed Expenses + Profits

Rs.250Q* = Rs.150Q + Rs.35000 + Rs. 0**

Rs.100Q = Rs.35000

Q = 35000 / 100

Q = 350 units

[Q* = numbers of units sold]

**The break-even point can be computed by finding that point where profits is zero.

The break even point in sales Rupees can be computed by multiplying the break even level of

units sales by the selling price per units.

350 units x 250Rs. per units = Rs. 87500

Contribution Margin Method:

The contribution Margin method is actually just a short cut conversion of the equation method

already described. The approach center on the idea discussed earlier that each unit sold provides

a certain amount of contribution margin that goes toward covering fixed cost. To find out how

many units must sold to break even, divide the total fixed cost by the unit contribution margin

be.

Break even Point In Units = Fixed Expenses / Unit contribution Margin

35000Rs. / Rs.100* per unit

350 units

*Rs. 250 (sales) – Rs. 150 (variable Exp.)

A variation of this method uses the Contribution Margin Ration (CM ratio) instead of the unit

Contribution margin. The result is the break even in total sales dollars rather than in total units

sold.

Break even point in total sales dollars = Fixed Expenses / CM Ratio

= Rs. 35000 / 0.40

= Rs. 87500

This approach is particularly suitable in situation where a company has multiple product lines

and wishes to compute a single break even point for the company as a whole.](https://image.slidesharecdn.com/cosmopolitan-150312113114-conversion-gate01/85/Break-Even-Analysis-and-Break-Even-Point-19-320.jpg)

![20

The following formula is also used to calculate break even point

Break even point in Rupees = [Fixed cost / 1 – (variable cost – Sales)]

This formula can produce the same answer:

Break even point = [Rs. 35000 / 1 – (150/250)]

= Rs. 35000 / 1 – 0.6

= Rs. 35000 / 0.4

= Rs. 87500

Break-even Point In Units

The break-even point in units for Oil Change Co. is the number of cars it needs to service in

order to cover the company's fixed and variable expenses. The break-even point formula is to

divide the total amount of fixed costs by the contribution margin per car:

It's always a good idea to check your calculations. The following schedule confirms that the

break-even point is 160 cars per week:](https://image.slidesharecdn.com/cosmopolitan-150312113114-conversion-gate01/85/Break-Even-Analysis-and-Break-Even-Point-20-320.jpg)

The document appears to be a student project report on break-even analysis and break-even point. It includes sections on definitions of key terms related to break-even analysis like fixed costs, variable costs, selling price. It also discusses the assumptions and limitations of break-even analysis. The document provides an example calculation of break-even point using the contribution margin method and defines break-even point as the sales volume where total revenue equals total costs and profit is zero. It is a student report submitted to the University of Mumbai for an M.Com course.