Downloaded 2,458 times

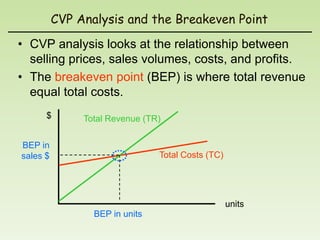

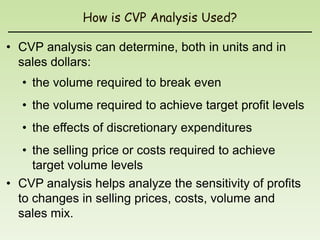

This document discusses cost-volume-profit (CVP) analysis and how it can be used to analyze the relationship between costs, sales, and profits. It defines the breakeven point as the level of sales where total revenue equals total costs. The document provides examples of using CVP analysis to calculate breakeven points, target profits, and how costs and selling prices can impact profits. It also demonstrates how CVP analysis can be used to compare alternative business strategies and identify indifference points.